The good news about Long Term Evolution networks is the faster speed and lower latency end users experience. The sometimes good news is that some mobile operators can charge a premium for use of the LTE network.

The in some ways good news is that people consume more data on an LTE network.

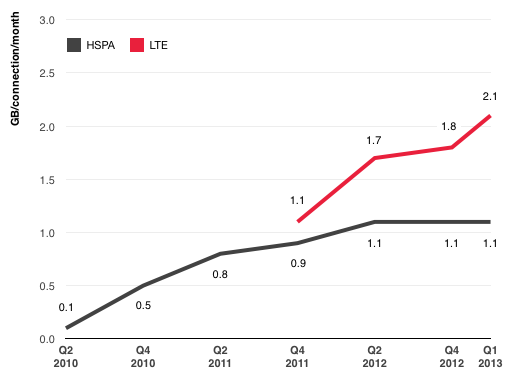

SK Telecom, for example, has seen average monthly data consumption per user rise significantly since the launch of its 4G network in 2011, with average consumption doubling between the fourth quarter of 2011 and first quarter of 2013, rising from 1.1 GB to 2.1 GB.

By way of comparison, data usage on the 3G network remained flat. Basically, total 3G and 4G network traffic almost doubled in the space of 15 months, on a two-percent growth in total connections.

What that means is that 4G users typically consume twice as much data per month as other users, according to GSMA.

That can have a direct impact on revenue when mobile service providers are able to charge somewhat incrementally for the additional usage. In other cases, where operators cannot bill for the higher usage, LTE can represent a problem.

Significantly, South Korean users actually are using Wi-Fi less, and using the LTE network more, than they had been doing in the past. GSMA believes that is happening because LTE now offers faster uploads and downloads than Wi-Fi does.

South Korean operators are generating significantly increased revenue from their 4G customers, GSMA notes. At KRW46,000 ($43), SK Telecom’s 4G average revenue per user in the the third quarter of 2013 was 32 percent higher than its blended ARPU.

In part, that is because more than 70 percent of new and upgrading 4G customers are buying higher-priced service plans.

At Korea Telecom, 4G ARPU of KRW44,000 ($42) was more than 40 percent higher than blended ARPU.

Operators in the United States are seeing similar trends. In October 2013, Verizon Wireless reported that the 38 percent of its retail 4G customers generated 64 percent of total data traffic.

But traffic is not revenue. Verizon Wireless third quarter 2013 average revenue per account was up 7.1 percent year over year.

Also, ARPA has grown 21 percent since the launch of the 4G network in 2010.

Cricket Communications says “usage from a 4G customer is about twice that what it is for a 3G customer,” while ARPU was up 8.4 percent year over year in the third quarter of 2013.

The picture in Europe is a bit more mixed. To be sure, 4G users consume more data than 3G users.

In the first quarter of 2013, Vodafone reported that average monthly data usage for its 4G smartphone users in Europe was 640 MB, approximately twice that for a 3G smartphone (350 MB) and roughly the same as a tablet operating on 3G.

In Germany, O2 reported third quarter 2013 monthly average data consumption by 4G users was three times that of non-4G users.

The UK’s EE said second quarter 2013 revenue from 4G customers was higher by about 10 percent. In the third quarter of 2013, 4G customers provided ARPU gains in the high single digits, EE said.

This contributed to a slight annual rise in blended ARPU (+0.5%), to £19.00 ($29.45) in Q3 2013.

In France, there has been no ARPU growth from 4G, however, among the three largest mobile providers. In part, that is because the operators have had to cut prices to compete with Illiad’s Free Mobile offers.

The average ARPU in France was down 13.2 percent year over year in the third quarter of 2013 to €22.82 ($30.23). GSMA expects the downward trend to continue.

But France isn’t the only market where an operator has chosen to offer 4G services without charging a premium. For example, 3UK, which switched on 4G last month, is allowing customers to migrate without switching from their 3G contracts and will continue to offer unlimited data allowances. Telefonica Movistar also is offering 4G at the same price as 3G.

SK Telecom Data Consumption

Source: SK Telecom