Making new spectrum available is one of the traditional ways regulators can introduce more competition into a market.

Perhaps rarely is the business environment so turbulent as in the U.S. mobile market, where a pricing war has broken out after years of stability, major blocks of new spectrum are going to be made available, and regulators face a new round of industry consolidation.

And regulators face a very tricky challenge. They must weigh the impact on competition and investment if four national mobile providers consolidate into three.

They have to design spectrum auction rules that presumably encourage competition at the same time the auctions raise revenue and make additional capacity available.

And they have to do so in a dynamic environment where the long-term outcomes are unclear, no matter which way policy is set. Some might argue it is self evident that four contestants are better than three.

Others argue the market will not support four contestants over the long term, and that three strong competitors will provide better consumer outcomes, and promote investment as well.

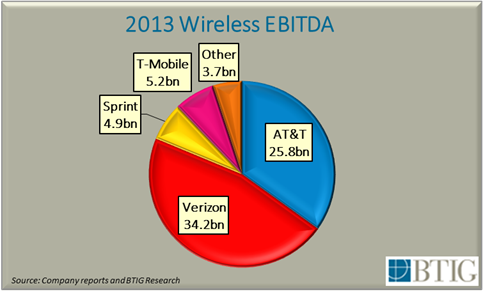

Looking only at earnings, it is clear the market is unstable. Where 2013 mobile earnings for Verizon were about $34 billion, and where AT&T earned about $26 billion, Sprint earned about $5 billion while T-Mobile US earned $5 billion as well.

The contestants are far from evenly matched, in other words. And some would say the long-term market structure cannot support four competitors so unevenly arrayed.

What policies might be created to affect the outcome is the issue. The smaller mobile carriers argue for spectrum set-asides, especially in the important upcoming 600-MHz auctions.

But that holds risks. Doing so would reduce the revenue the auctions would generate. That might not be so big a problem, except for the fact that the FCC is holding a two-stage auction, and has to induce TV broadcasters to give up their spectrum first, before mobile service providers can bid to acquire the spectrum.

Spectrum prices, in other words, will have a direct bearing on whether the auctions even are possible. Complicating matters is the desire expressed by Sprint to buy T-Mobile US, and the impact such a deal would have on Sprint willingness and ability to bid for new 600-MHz spectrum.

Already burdened by debt, Sprint might not be able to afford both a T-Mobile US acquisition and significant new 600-MHz spectrum, no matter what the bidding rules. And in that case, will there really be any more than two bidders, namely AT&T and Verizon, something the FCC might well want to avoid.

Nor is it clear Sprint will bid in the next auction of AWS 3 spectrum. That 65 MHz of new mobile spectrum in the 1695-1710 MHz, 1755-1780 MHz, and 2155-2180 MHz bands is in some ways going to be unappetizing for all the four major carriers.

The incremental spectrum gains are likely to be fairly minor (10 MHz gained by any single carrier is a likely result). And the big 600-MHz auction lies ahead.

Also, there is a novelty. The 2155-2180 MHz portion of the AWS 3 band already is licensed for use by Federal users.

So that spectrum will be available only on a shared basis with the new commercial users. That is a first for formerly-exclusive license issuance. But shared spectrum is likely to be considered less valuable than exclusive-use spectrum, and will therefore likely lead to lower market prices than other similar exclusive-use spectrum.

Also, in the case of AWS 3, there are indications that Sprint is not too interested in bidding.

Dish Network, on the other hand, is viewed as the likely bidder for unpaired spectrum Dish can pair with its existing AWS 4 spectrum.

The point is that it is not clear the AWS 3 auction will have as much impact on the fortunes of the leading mobile providers as other coming developments.

More importantly, it is not absolutely clear what the FCC can, or should do, with respect to enhancing competition in the U.S. mobile market. A reasonable observer might well argue that Sprint and T-Mobile US simply are too small to compete against AT&T and Verizon, long term.

|

| Source: BTIG Research |