It has been a rule of thumb that U.S. cable TV operators have operating costs lower than their major telco competitors.

But on one metric--revenue per employee--AT&T and Verizon arguably perform much more efficiently than U.S. cable TV operators.

Time Warner Cable, not among the best managed U.S. cable TV companies, generates revenue of about $436,000 per employee..

The average sales per AT&T employee totaled $495,000 in 2012, up from $209,000 in 2006, and is closer to $529,060 revenue per employee at present.

At least in part, those gains at AT&T and Verizon can be accounted for by continuous efforts to reduce headcount.

Tier one service providers, no less than other service providers, have been working to control or reduce operating costs for more than a decade, and especially over the last five years, in large part to cope with declining gross revenues (in Western Europe) or margin-challenged revenues (in the U.S. market).

Between 2007 and 2012, AT&T eliminated 67,620 jobs, almost a quarter of its workforce. At least in part, that accounts for average sales per AT&T employee of $495,000 in 2012, up from $209,000 in 2006.

Over the same five-year period, Verizon eliminated 48,000 jobs. Across the industry, telecom employment has fallen by almost 200,000 since 2007, according to the U.S. Labor Department.

Most of those cuts have come in the fixed network business, as mobile segment headcounts have been roughly flat between 2001 and 2008, and have been declining since 2008.

Between 2008 and 2010, the mobile segment lost about 40,400 jobs overall, by some estimates. By other estimates, U.S. mobile business jobs dropped by only about 10,000.

The point is that, by any estimate, most of the lost U.S. communications jobs have come from the fixed network business.

Still, it remains the case that U.S. cable operators have operating cost structures lower than the leading U.S. telcos.

|

| source: Michael Mandel |

In 2010, for example, where U.S. telco employee headcount might have been between 432,000 to 455,000, U.S. cable companies likely had between 157,000 to 180,000 employees, according to the U.S. Department of Labor.

Of course, the U.S. cable TV distributor business generated about $90 billion in annual revenue, where telcos generated about $447 billion.

Mobile revenue was about $160 billion in 2010, while fixed network revenue was about $287 billion.

But telcos had headcount only about 2.5 times to 2.75 times greater than cable TV companies.

By that measure, U.S. telcos are “more efficient” than U.S. cable TV companies.

AT&T and Verizon will continue to face the challenge of matching operating costs both to market competitors and to revenue generated by each of the lines of business. But it is, in many respects, hard to argue both firms have not been performing well, in terms of revenue per employee.

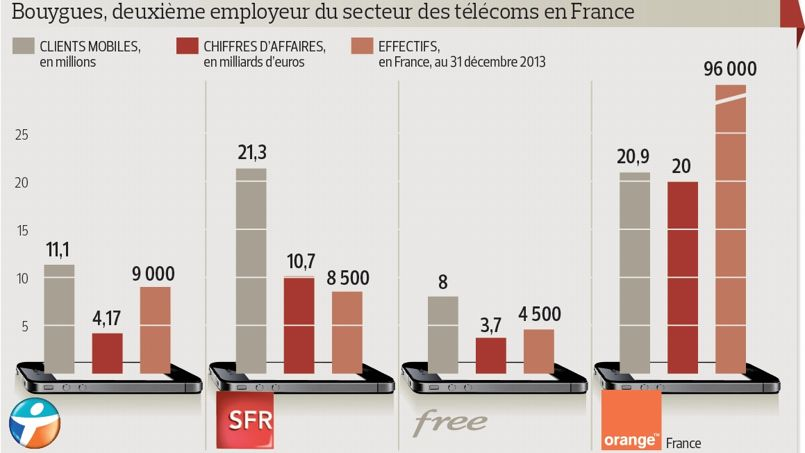

The French mobile carrier that really has outstanding sales per employee uses a "Wi-Fi-first" approach that U.S. cable operators will take, eventually.

Consider that Bouygues in France has about 11.1 million mobile customers, and nine million employees, while Illiad’s Free Mobile serves eight million mobile customers with 4,500 employees.

|

| source: Le Figaro |

Likewise, Bouygues has sales of about 4.17 billion euros, while Free Mobile has sales of about 3.7 billion euros.

In other words, Bouygues generates gross revenue of about 463,000 euros per employee, while Free Mobile earns about 1,777,000 euros per employee.

SFR, newly purchased by Numericable, has mobile revenue of about 1,258,000 euros per employee.

Orange, by way of comparison, apparently generates only about 208,000 euros per employee.

Free Mobile generates an order of magnitude more revenue per employee as does Orange. Even Bouygues generates double the revenue per employee as does Orange.

To be sure, Orange continues to have significant French government investment, so social goals--especially employment--are a consideration for Orange.

To be sure, by some estimates perhaps 33 percent of current employees will retire over the next six or seven years, allowing Orange a chance to gradually reduce the labor intensity of its French operations, assuming the French government will allow that to happen.

Some doubt much will be tolerated on that score, making it tough for Orange to get its cost structure in line with its major competitors, precisely at the point that SFR now will be able to marry cable TV services and fixed line high speed access with mobile service, more directly challenging Orange.

Also, Orange carries significant long term debt on its books as well, perhaps 30 billion euros. Paying down that debt on the basis of existing cash flow seems unlikely in the extreme.

For its part, Bouygues now seems likely to cut employees by a significant amount, in an effort to align its revenue per employee more closely with those of Free Mobile.