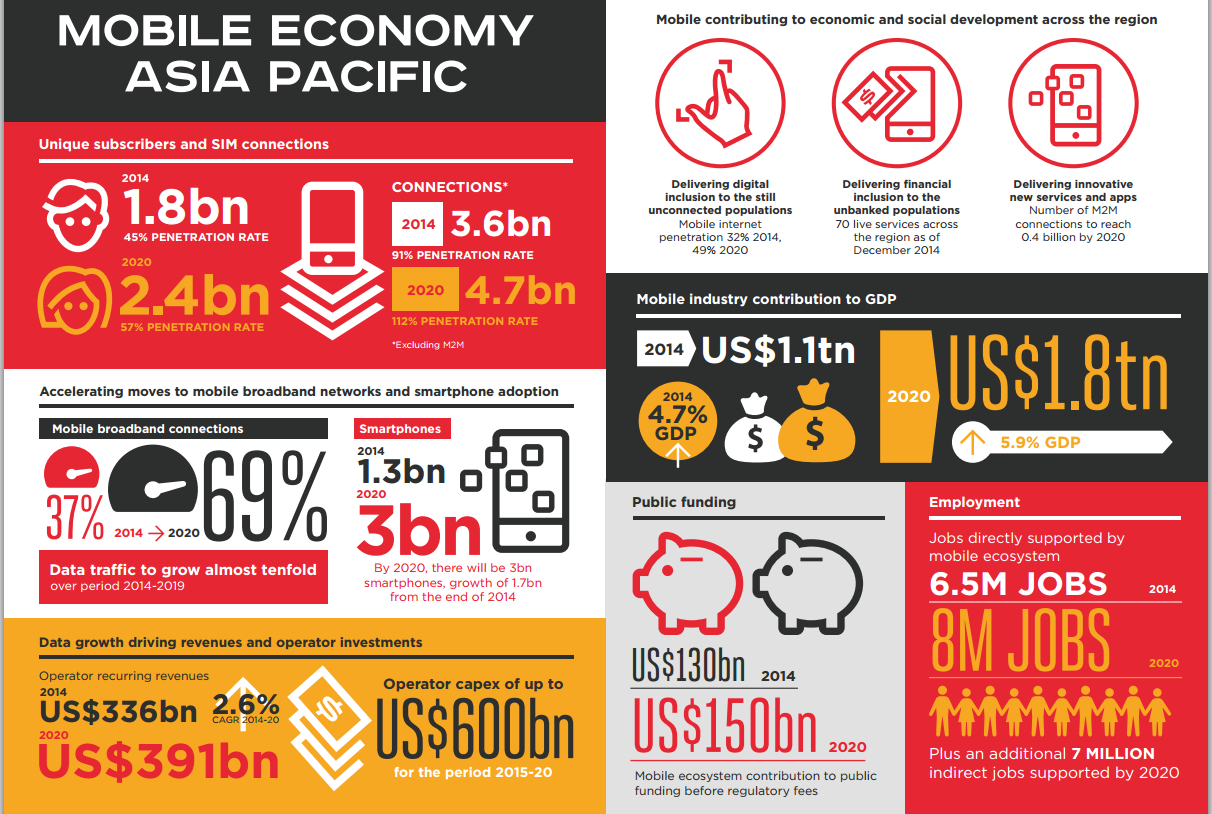

The mobile industry in Asia Pacific was worth more than US$1 trillion per year to the region’s economy in 2014, equivalent to 4.7 per cent of the region’s gross domestic product, with over a quarter of this economic contribution generated directly by mobile operators, a study sponsored by the GSMA.

Mobile operators directly contributed US$286 billion to the total in 2014, equivalent to 1.2 percent of regional GDP.

It is forecast that the Asia Pacific mobile industry will be worth US$1.8 trillion by 2020, accounting for 5.9 percent of projected regional GDP by this point.

In 2014 the mobile ecosystem directly and indirectly employed 12.5 million people in Asia Pacific, a figure expected to rise to 15 million by 2020. T

he industry also makes a substantial contribution to the funding of the public sector, with approximately US$130 billion contributed in 2014 in the form of general taxation. This is set to grow to over US$150 billion by 2020.

The study reveals that Asia Pacific now accounts for half of the world’s unique mobile subscribers and mobile connections and will continue to grow at a faster pace than the global average over the next five years, adding 600 million new unique subscribers by 2020.

Migration to 4G networks and services in markets such as China is now occurring at a faster rate than was the case in developed regions such as Europe and North America

At the end of the first quarter of 2015, there were 1.8 billion unique mobile subscribers in Asia Pacific, representing 45 per cent of the region’s population.

China, India, Indonesia and Japan account for over 75 percent of the region’s subscriber base.

Many of the largest markets in the region are still relatively underpenetrated, however.

India, Pakistan and Bangladesh, for example, have a combined population of over 1.6 billion, but a unique subscriber penetration rate of only 36 per cent on average.

Connecting these unconnected citizens will therefore be a major focus for both the mobile industry and policymakers in the region over the coming years.

The number of unique mobile subscribers in the region is forecast to grow by five percent per year over the remainder of the decade (2014 to 2020 CAGR), faster than the global average (four percent) and making Asia Pacific the second-fastest region globally behind only Sub-Saharan Africa.

Total mobile connections in the region stood at 3.7 billion in the first quarter of 2015.

Fourth generation networks accounted for nine percent of connections, a figure expected to reach a third of the total by 2020.

South Korea and Japan lead the world in 4G adoption, but the region also contains markets where 4G deployments are at an early stage (such as India, Indonesia and Pakistan) or where 4G licensing has yet to take place (such as Bangladesh, Myanmar and Vietnam).

Smartphones now account for 40 percent of connections in the Asia Pacific region and are set to account for 66 percent of the total by the end of the decade.

According to Cisco, mobile data traffic growth in Asia Pacific will grow at a 58 percent compound annual growth rate through to 2019.