Tuesday, October 20, 2015

The Force Awakens

Because you need to relax, sometimes.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

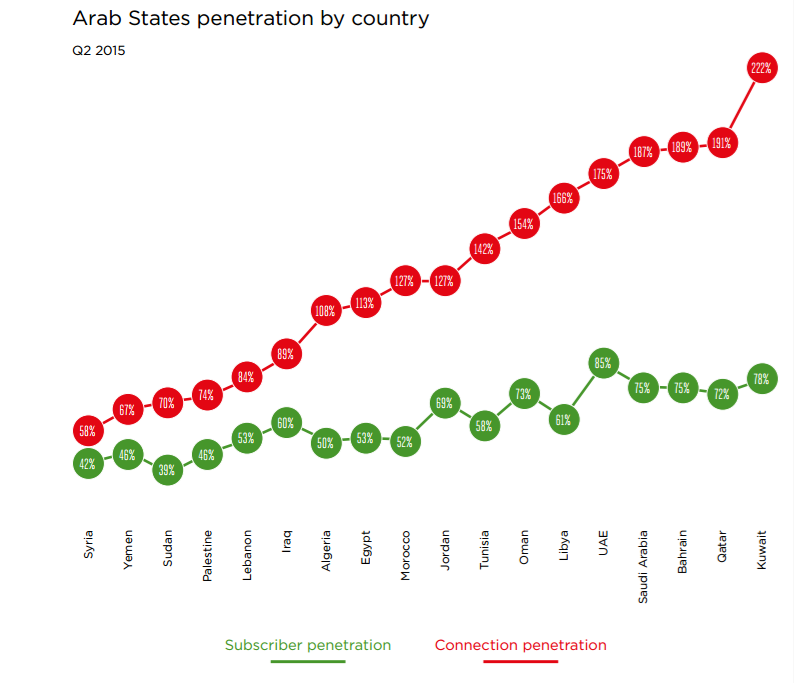

66% Mobile Broadband Adoption in Middle East, North Africa by 2020

Mobile broadband networks will support more than 66 percent of all mobile connections across the Arab States of the Middle East and North Africa by 2020, according to a new GSMA study.

The study predicts there will be 350 million 3G or 4G mobile broadband connections in the Arab States by 2020, accounting for 69 per cent of the region’s total connections by 2020, up from just 34 per cent at the end of 2014.

The number of smartphones connections in the region is forecast to almost triple between 2014 and 2020, reaching 327 million.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

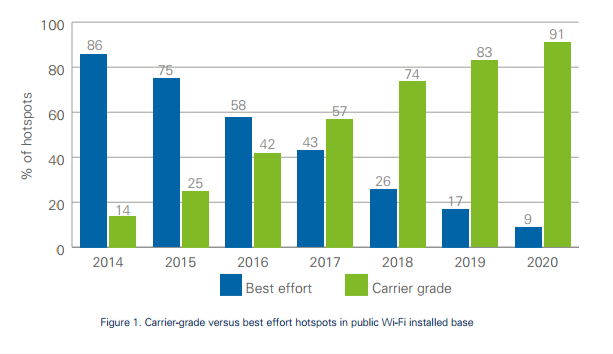

Many Large Public Hotspot Networks Will Be Carrier Grade (and Use QoS) by 2020

It would have been easy to predict, in advance of the promulgation of network neutrality rules, that such rules would simply push suppliers in other directions, either to improve business models or introduce differentiated new services.

That appears to be happening.

Despite the existence of network neutrality regulations--which apply to consumer access services--it appears quality of service mechanisms are going to be quite a prevalent feature of end user experience on many public hotspot networks, as such rules are enablers of new services and revenue streams.

Some important consumer applications actually benefit from, and under conditions of congestion, might require, quality of service (packet prioritization) mechanisms. And public Wi-Fi hotspot networks now are emerging as one expression of support for such QoS-enabled services.

That apparent contradiction is easy to explain, if one thinks about the matter. Though retail consumer Internet access services are covered by present network neutrality rules, business services are not covered.

A public hotspot is a business service, not consumer service. Whether the buyer is a hotel or coffee shop, or part of a network of public hotspot services, amenity Wi-Fi is a business service, not “consumer Internet access.”

So there is no violation of network neutrality rules, if a public hotspot is used to support QoS-enabled services such as carrier voice.

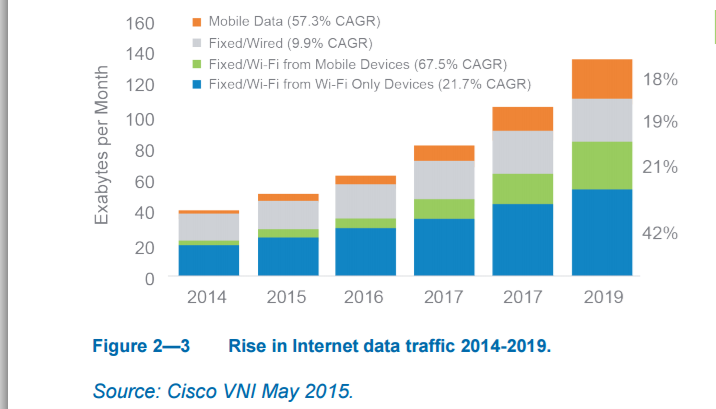

Juniper Research estimates that Wi-Fi networks will be carrying 60 percent of mobile data traffic by 2019. Cisco estimates that Wi-Fi will handle 63 percent of all traffic that year. And some of those services will benefit from quality assurances.

Separately, says the Wireless Broadband Alliance, among operators with hotspot networks in place, 57 percent have a timeline in place to deploy a next generation hotspot (Passpoint) standard network. By definition, Passpoint employs quality of service mechanisms.

Some 61.5 percent of respondents already have NGH or plan to deploy it over the coming year, while a further 29.5 percent will roll it out in 2017 or 2018.

The dominant business driver is the need to enhance or guarantee customer experience for revenue streams such as TV everywhere or enterprise services.

The Wireless Broadband Alliance, which created the Passpoint standard, also has promulgated quality of service mechanisms. Wi-Fi Certified WMM added quality of service (QoS) functionality in Wi‑Fi networks.

With WMM, introduced in 2004, network administrators and residential users can assign higher priority to real-time traffic such as voice and video, while assigning other data traffic to either best-effort or background priority levels.

Introduced in 2012, WMM-Admission Control further improves the performance of Wi‑Fi networks for real-time data such as voice and video by preventing oversubscription of bandwidth.

Prioritization of traffic includes categories for voice, video, best effort data, and background data, managing access based on those categories.

And many large hotspot network operators presently believe carrier-grade hotspots will represent 57 percent of all their locations, with carrier-grade hotspots accounting for 90 percent of locations by 2020.

Despite network neutrality rules, support for such apps likely is coming. All the technology tools are there to do so on big Wi-Fi hotspot networks.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, October 19, 2015

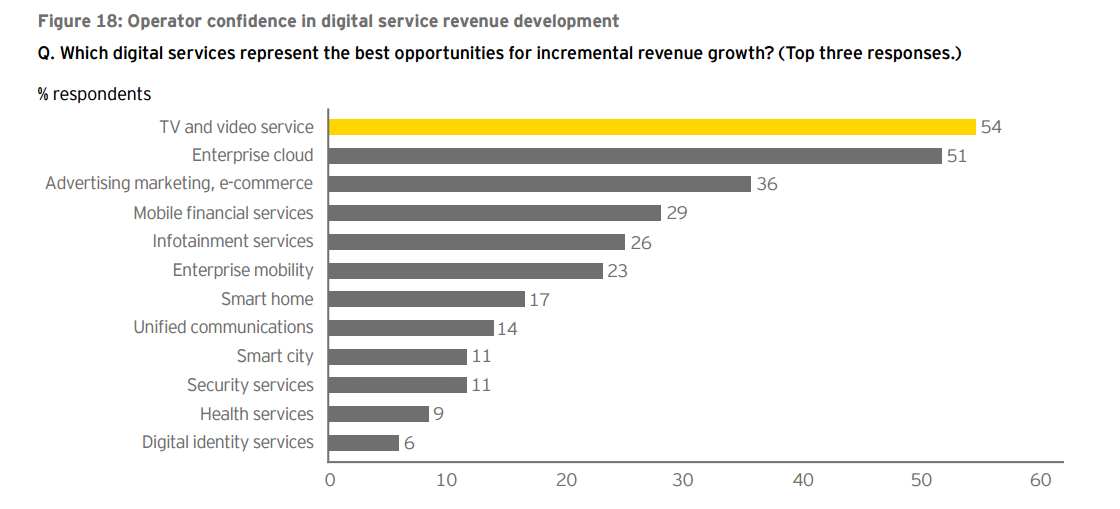

Most Incremental Revenue Opportunities are Enterprise Focused, Not Direct Consumer Services

With one notable exception, a panel of global service provider executives surveyed by E&Y expects enterprise services--not consumer services--to drive future revenue growth.

With one notable exception, a panel of global service provider executives surveyed by E&Y expects enterprise services--not consumer services--to drive future revenue growth.

That notable exception is video entertainment services, expected by 54 percent of respondents to be the service with best opportunities for incremental revenue growth. Among the more-promising fields identified by the executives, 51 percent saw enterprise cloud opportunities as most promising.

Also notably missing from the list of expected revenue contributors are Internet of Things apps. In large part, that might speak to a structural fact of life, namely that most IoT apps driving significant revenue might require sponsorship and involvement by third party app providers. Also, even most large service providers will not have the scale to drive significant success.

Also notably missing from the list of expected revenue contributors are Internet of Things apps. In large part, that might speak to a structural fact of life, namely that most IoT apps driving significant revenue might require sponsorship and involvement by third party app providers. Also, even most large service providers will not have the scale to drive significant success.

There was much less consensus about many of the other services deemed drivers of future revenue growth. And though some of the services could be marketed directly to consumers, most of the opportunities seem logically to involve an enterprise partner.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

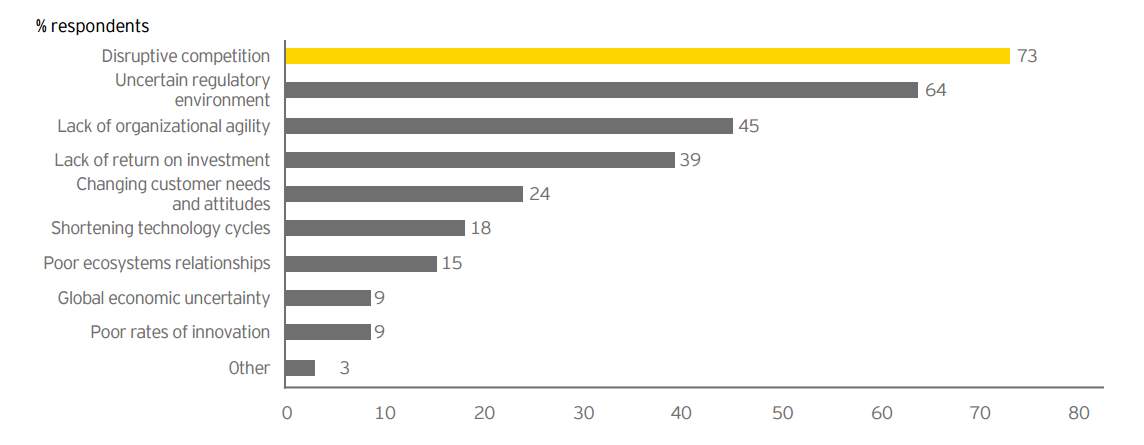

Competition is Top Service Provider Concern

Competition in general, and competition from over the top providers in particular, are the top two challenges global telecom executives say they face.

Fully 73 percent of service provider executives surveyed by E&Y say disruptive competition is the leading industry challenge.

But 64 percent of respondents also say regulatory uncertainty is an issue, as well. No other concerns are cited by more than 45 percent of respondents.

Of regulatory issues, access to new spectrum is cited by 78 percent of executives as the top concern.

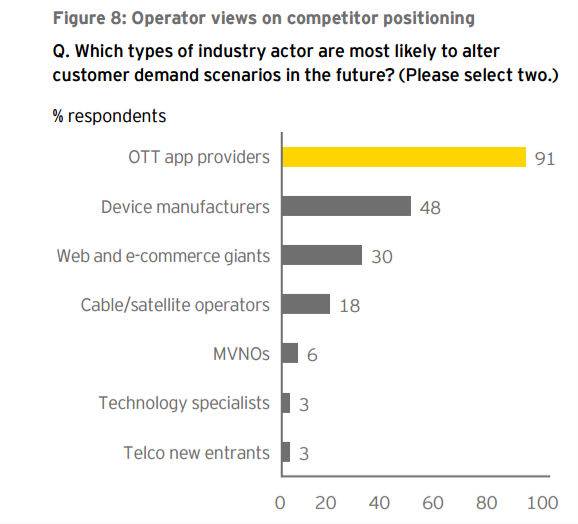

OTTs (app providers) represent the chief competitive challenges--even more than traditional firms within the telecom business--the study finds. The reason is that app providers now set pricing environments, cannibalize legacy revenues and create new consumer expectations.

App providers, such as WhatsApp, are viewed as the top driver of new consumer demands by 61 percent of respondents.

In developing regions, 67 percent of executives say device suppliers are likely to be key shapers of end user demand.

Service providers overall get about 55 percent of ecosystem revenue.

Survey respondents believe that app provider share of industry value chain revenues reached the 10 percent mark in just a few years according to EY estimates. That underestimates impact, however.

The challenge is that OTT apps redefine consumer price expectations. So the revenue impact on legacy providers is not so much loss market share but lower profit across the board.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

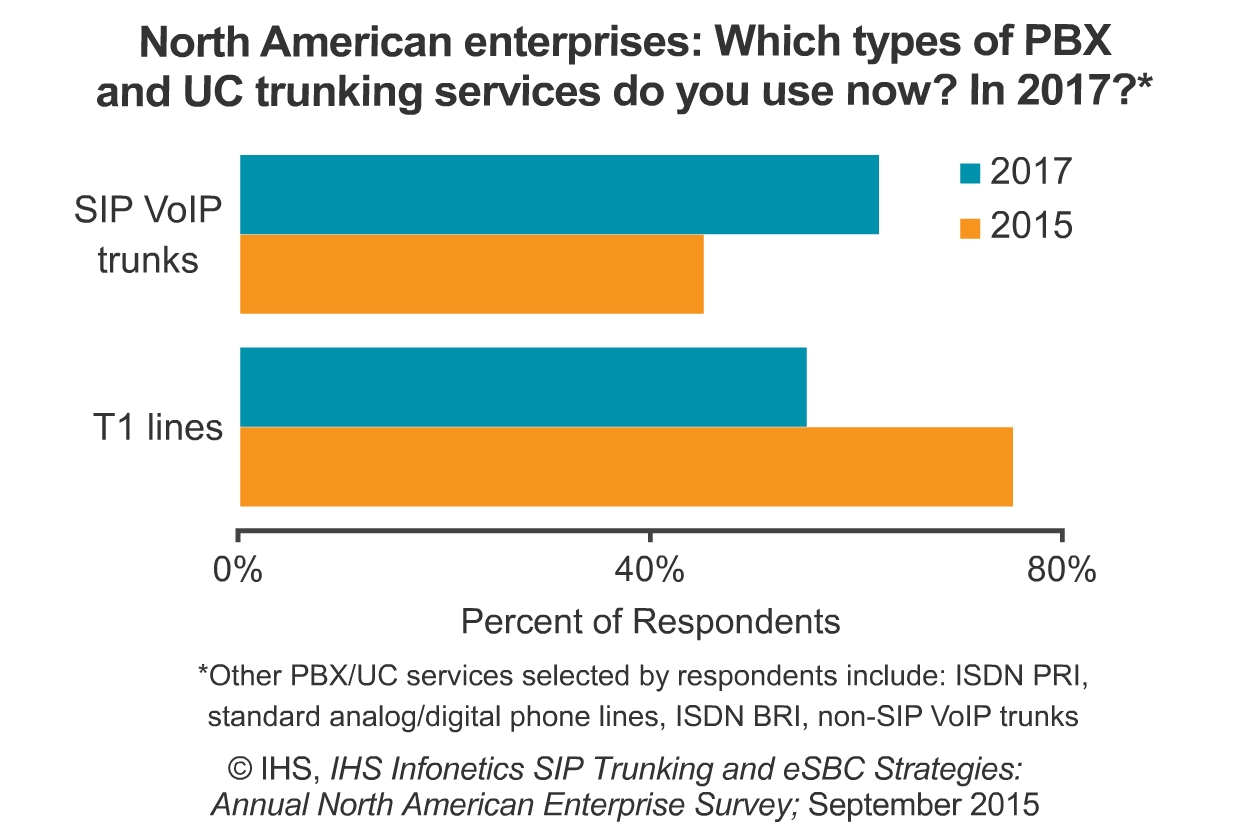

SIP Trunking at 45% in North America

About 45 percent of North American respondents use Session Initiation Protocol (SIP) today for a portion of their voice connectivity requirements, a survey conducted by IHS finds.

By 2017, the number of enterprises using SIP should rise to 62 percent.

Though businesses are migrating to SIP trunking, few have done a full cutover. Of those surveyed who already use SIP trunking, SIP represents about 50 percent of voice trunk capacity.

“SIP trunking’s been around for a while, but our survey shows inertia on the part of businesses tied up with existing contracts and services is inhibiting growth,” said Diane Myers, IHS research director.

The supplier market is fragmented and no single provider dominates. SIP trunking connections also are currently dominated by native support on the PBX rather than edge equipment such as enterprise session border controllers (SBCs) or gateways

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Special Access Battle Heats Up, Again

Some of us cannot remember a time when “special access” was not a contentious issue. The reasons--irrespective of all valid public policy concerns--are that special access has been, and remains, a major product for business customers.

At one level, the issue is how to create policies that encourage faster transition while not disrupting legacy operations too much. At another level, the dispute is over relative commercial advantage. All valid public policy disputes always involve considerations of private interest.

The other issue is that most sellers of special access do not own their own facilities, and lease access--for their own use or for resale--from a few companies that do own facilities. So disputes over wholesale pricing typically are at the center of dispute.

So it is not surprising that special access once again is on the docket of the U.S. Federal Communications Commission, and not surprising that prices are at the center of the dispute.

By some estimates, annual sales of special access circuits (T1 and DS3, for example) are about $24 billion.

To be sure, access is transitioning to Ethernet, but smaller customers and sites frequently rely on time division multiplexing (TDM) access.

In some ways, continuing debates about legacy TDM access, at a time when everybody agrees the legacy network needs to be shut down in favor of modern IP infrastructure, is curious.

In fact, some might argue it is silly to stupid to delay rapid network modernization to protect a $24 billion business that is shrinking and as much a part of the legacy infrastructure as “all copper” access media.

To be sure, many advocate a logical approach, namely preserving TDM access as IP infrastructure is turned on, at the legacy prices. There is room to debate the notion of fair” prices.

After all, new optical infrastructure and all-copper legacy infrastructure have different cost recovery requirements. New infrastructure is not fully amortized. Copper infrastructure might be nearly fully amortized.

There is less room to argue about the scarcity of high-capacity access, as access networks are scarce, and only one of two ubiquitous fixed network access suppliers in each market is subject to mandatory access requirements in most markets (some telcos, not any cable TV companies).

In 2013, incumbent local exchange carriers sold roughly 75 percent of the approximately $20 billion in annual revenues from the sales of DS1 and DS3 channel terminations, and received nearly 66 percent of all revenue from TDM sales.

That finding, in and of itself, might not be surprising, since only one provider in each market has both ubiquitous access assets and mandatory wholesale obligations (the underlying carrier makes money from its own retail sales and wholesale sales as well).

Only special access sales made by cable TV companies or independent providers with their own owned networks do not create revenue for the underlying carrier.

The latest inquiry centers on contract terms competitors say are unfair.

Some might also note that, no matter what is done, TDM-based access is going to keep declining, as do all legacy access methods do, when the next-generation network becomes ubiquitous and as end users switch from legacy to next-generation access equipment and software.

That is not to deny a transition period of some length. But TDM-based special access is going away, as IP access takes its place.

At one level, the issue is how to create policies that encourage faster transition while not disrupting legacy operations too much. At another level, the dispute is over relative commercial advantage. All valid public policy disputes always involve considerations of private interest.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...