The only certainty, where it comes to what Dish Network might do with its mobile spectrum assets, is that the firm will never allow the value of those assets to fall to zero. Beyond that, almost any monetiztion strategy is conceivable.

Despite the difficulties, some analysts think Dish Network might finally move to create a mobile business by first striking a long-term spectrum leasing deal with Verizon before the start of the 600-MHz incentive auctions planned for the first quarter or second quarter of 2016.

In general, any such deal would have Verizon trading long-term spectrum rights obtained from Dish Network for turned-up mobile capacity Dish Network could use to launch its mobile service.

Another scenario is Dish creating a spectrum leasing company that supplies different spectrum assets to different customers, including Verizon, AT&T and Sprint.

Though one cannot completely discount Dish doing a deal of some sort with either T-Mobile US or Sprint, neither of those companies could easily consider any major cash deals, and neither company really needs more spectrum right now.

In principle, a spectrum deal, or creation of a spectrum leasing company, would not necessarily prevent Dish from inking other deals with other carriers. Dish might well require retail store support, for example.

Perhaps Dish’s business plan would combine both mobile and fixed access. About the only scenario not conceivable is that Dish Network would allow the value of its spectrum holdings to fall to zero.

And though any such deals are logically discrete from the upcoming 600-MHz incentive auction, any such deals would affect contestant interest in that auction.

In addition to the decision by Sprint to sit out the auctions entirely, removing a major bidder for the reserve spectrum, now Verizon is hinting that it sees less value in the 600-MHz bands, because it already relies on 700-MHz spectrum.

And Verizon’s thinking would definitely shape its need and willingness to bid in the 600-MHz auctions.

Verizon has said it does plan to bid for 600-MHz spectrum, but Verizon also seems to be signaling that it has other options, and might not bid as aggressively as some had thought likely.

To be sure, such statements might, aside from other reasons, be positioning tactics, designed in part to dampen expectations that Verizon would be forced to bid “whatever it took” to acquire spectrum in the 600-MHz auction.

Perhaps Verizon also is signaling that it is less interested in 600-MHz spectrum than some had hoped Verizon would be, perhaps tempering expectations of license sellers and containing prices.

On the other hand, such statements also signal that a potential deal with Dish Network for wholesale access to its spectrum at 2-GHz is perhaps more interesting. That might also dampen price expectations for 600-MHz spectrum.

"Higher frequency spectrum is capacity and that's really what we need at this point in time," said Fran Shammo, Verizon CFO.

But it also would be necessary for Verizon to conclude any such deals before the 600-MHz auctions start, to comply with anti-collusion rules.

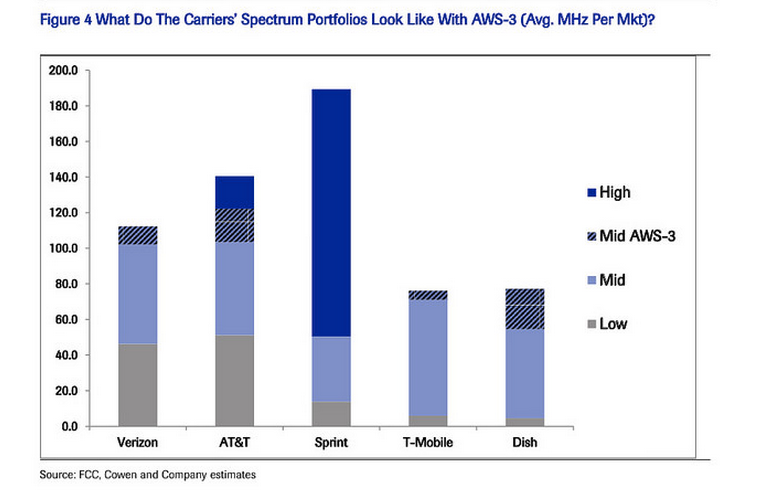

Most mobile spectrum is valued on either its coverage or its capacity dimensions, the basic trade off being that lower-frequency spectrum is better for coverage, but less valuable for capacity, while higher-frequency spectrum is better for capacity than coverage.

Verizon arguably has a reasonable amount of “coverage” spectrum, but not so much “capacity” spectrum.