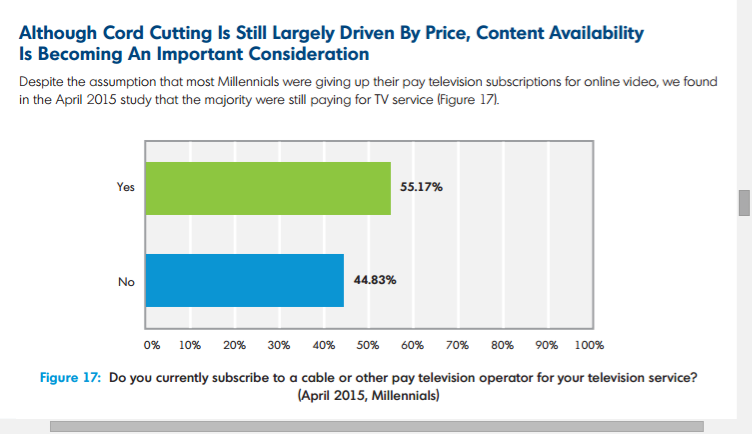

It is bad news when 45 percent of potential customers do not want to buy one of three core consumer communications or entertainment products, as the latest survey from Limelight Networks suggests. Though 55 percent of surveyed Millennials say they do buy linear video TV, that also means 45 percent do not buy.

That is an issue for all triple-play providers, but especially for cable TV and satellite TV firms, who have most of the market share.

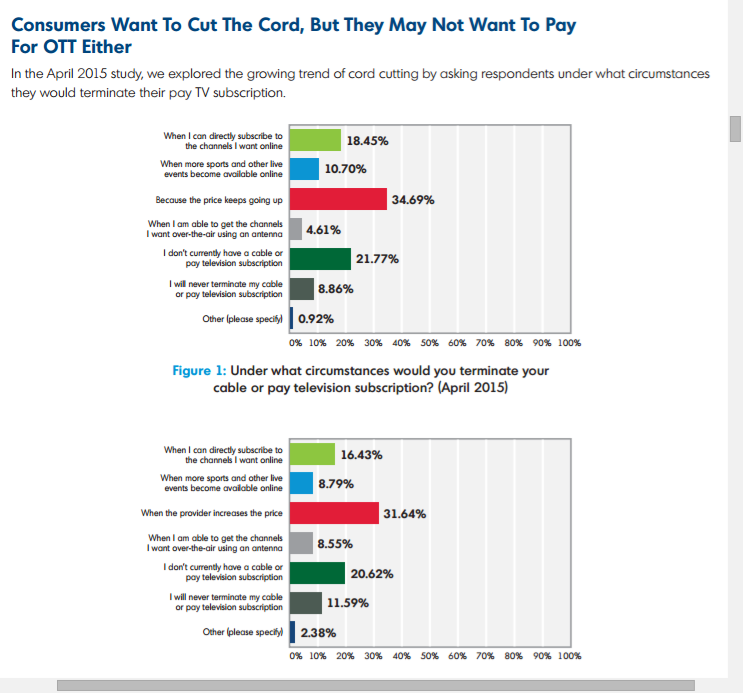

Price is an issue for many Millennials, as it is for most other demographic groups. Or, perhaps it is fair to say, price is an issue because value is challenged. The single greatest reason for disconnecting was “higher prices,” as you would expect. About 35 percent of subscribers said higher prices would cause them to consider disconnecting.

Some 19 percent suggested the ability to watch the channels they want online would be the reason for cancelling service. About 11 percent seem to be waiting for sports and live events to be available online.

Almost five percent say they would quit buying linear service when they are able to get all the channels they want over the air, using a TV antenna. Since that is not going to happen, we can discount the responses, and assume the key issue for such respondents is “no incremental cost.”

They seem to prefer paying nothing extra to watch all the channels they prefer, but that is not going to happen.

One issue that cannot be assessed is how typical spending might change, over time, as over the top streaming services proliferate and much content is available from a few dominant distributors.

What is unlikely to happen is that one single provider has content rights to “everything” a consumer might wish to watch. That will mean it is uncertain how spending might change, as consumers will have to buy more than one subscription, in all likelihood, to get most of what they want to view.

Some mix of “skinny bundles,” plus use of over the top subscription services, is likely to be the intermediate pattern for many consumers. More than 40 percent of Millennials, and 34 percent of all other consumers, already buy an OTT streaming service.

source: Limelight Networks