Once upon a time, fixed network telecommunications was thought to be a “natural monopoly,” akin to roads, bridges, sewer services, water and electrical services.

In many markets, that clearly is not true. There is at least some room for facilities-based competition, though the number of viable contestants will be limited.

So fixed and mobile telecommunications are best thought of as oligopolistic, where only a few leading suppliers actually can exist in a market.

There are key implications. It likely never will be possible for more than a few facilities-based competitors to survive in any market.

That naturally will lead to thinking about regulatory policies based on robust wholesale obligations. The downside: robust wholesale tends to depress both investment by the existing carrier, and market entry by new carriers.

So the issue is not monopoly versus widespread market entry, but between monopoly and the best-possible (sustainable) level of competition among a limited number of contestants. That always will be a judgment call.

But that also poses issues for telecom regulators. If the regulated markets will, under the best of circumstances, only support a few suppliers, where is the boundary between oligopoly conditions where there is not enough competition, and oligopoly under which there is reasonable competition?

“High market concentration levels in a given market may raise some concern that the market is not competitive,” the Federal Communications Commision says. “However, an analysis of other factors, such as prices, non-price rivalry, and entry conditions, may find that a market with high concentration levels is competitive.”

In other words, says the FCC, even high levels of concentration do not necessarily mean a market is uncompetitive. Such markets might, in fact, be substantially competitive, even when other measures say they are not competitive.

We might not like the situation, but in some industries--including telecommunications--oligopoly is the pattern. There always are smaller niches within the market, but typically the amount of activity is a small fraction of total market revenues.

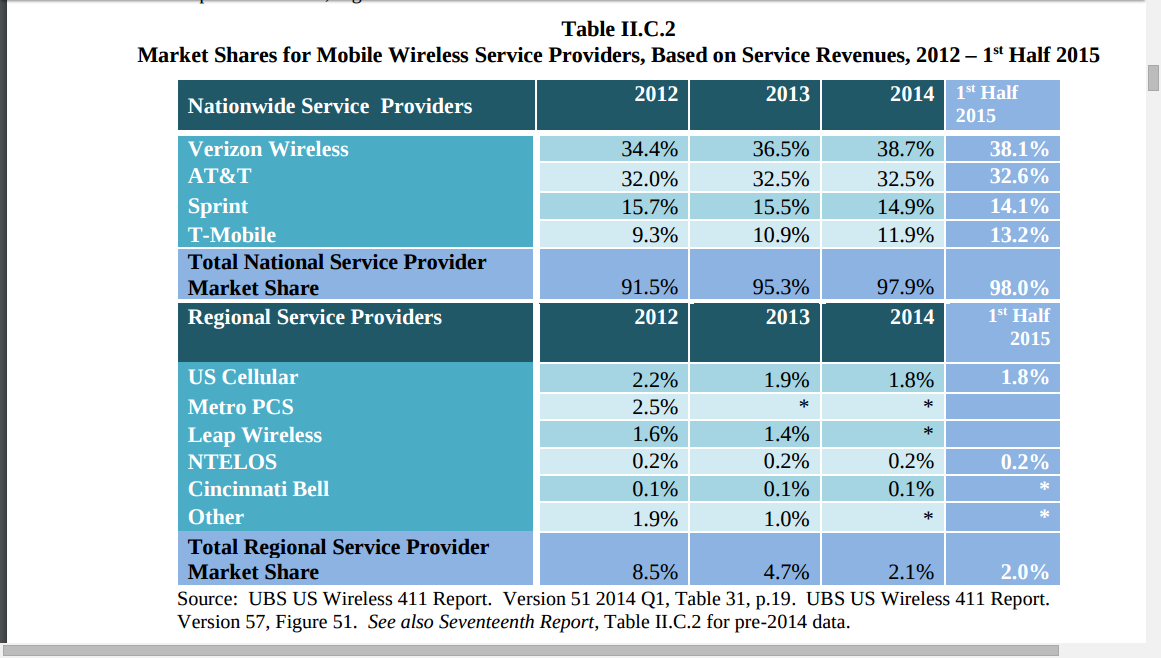

The U.S. mobile market is no exception. The four U.S. nationwide mobile service providers accounted for approximately 98 percent of the nation’s mobile wireless service revenue in 2014, up from approximately 91 percent in 2012, and the service revenues of AT&T and Verizon Wireless together accounted for approximately 71 percent of total service revenue in 2014, according to the Federal Communications Commission.

Of the four nationwide facilities-based service providers, AT&T and Verizon Wireless continued to maintain the largest market shares throughout 2014.

Sprint stayed relatively flat, and T-Mobile had the largest quarterly increases in market share to end 2014, as measured by revenue.

The same pattern continued in the first half of 2015, with AT&T and Verizon Wireless continuing to account for approximately 71 percent of total service revenues.

While T-Mobile continues to narrow the gap against Sprint, as of mid-2015, Sprint remained the third largest service provider in the mobile wireless marketplace in terms of service revenues.

The practical issue, then, often becomes the actual number of sustainable providers in any market. In the mobile arena, that tends to be the difference between three and four.