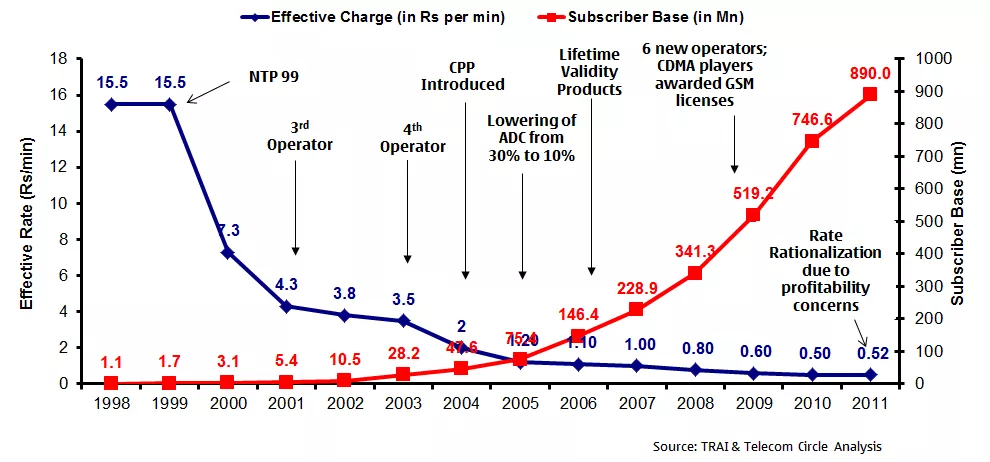

Facilities-based competition in access markets qualitatively increases business risk.

Consider sales expectations in a monopoly environment. If voice adoption was high--90 percent to 95 percent--revenue per passed location was a number nearly identical to revenue per customer location.

All that changes when there are two or more competitors with roughly equal capabilities and market share.

The business model for fiber to premises networks using industry-standard fiber-to-home platforms provides a clear example.

Depending on the deployment situation, the cost per location might range somewhere between a high of US$2,250 per site and US$660 per location on the lower end, including activated drops, but not including any required customer premises equipment.

Assume an “average network cost” of $1455 per location passed. If customer adoption is 95 percent, then the “per-customer” cost is about $1528.

In a duopoly market, the investment costs are radically different. Assume the network is expected to have a 50-percent adoption rate (one out of every two locations buys at least one service). Then the per-customer cost is $2910.

The economics obviously get worse in a three-provider market where expected take rates are 33 percent (again assuming three equally-skilled and capitalized competitors). In that scenario, a new provider might have to expect network costs of $4365 per actual customer.

You readily can see the business model problem. In a monopoly environment, per-customer network cost is just $1455. In a duopoly market the per-customer network cost might be $2910. In a three-provider market, network cost might be as high as $4365 per customer.

In other words, investment in a monopoly environment is three times higher, per customer, in a three-contestant market, and roughly twice as high as in a duopoly market.

Against that, assume $70 to $130 of revenue, in some cases. Over a three-year period, that is about $2520 to $4680 in revenue, per customer.

By rough estimate, assuming a customer life cycle of 36 months, the network might not even break even over three years, based solely on network costs.

Some U.S. ISPs, such as Sonic.net, are retailing gigabit connections plus voice for $40 a month, though. That implies three-year revenue of just $1440 per subscriber.

Assume a smaller operator could manage to connect a customer and activate service (including customer premises equipment) for about $300, where a telco connection might cost as much as $800.

So add network cost, plus service activation cost, of only $300 per site. That implies direct network-related activated customer investment of $1755 in the monopoly case, $3210 in the duopoly case and $4665 in the three-provider market.

Assume the ability to earn $130 a month of revenue requires selling video entertainment services, with higher customer premises equipment investment. So then use the $800 per customer figure for an activated location.

That implies monopoly scenario investment in network and CPE of $2255, growing to $3710 in the duopoly case and $5165 in the three-provider scenario. Recall that a three-year customer life cycle at $130 a month represents $4680 in account revenues.

All of that is before operating costs, franchise payments and marketing. Clearly, service providers are counting on longer customer life cycles, incrementally higher revenues and muted operating costs, to make the business case work.

The fundamental point is that the economics of a competitive fixed network business case are radically more difficult than in a monopoly environment.