The Telecom Regulatory Authority of India castigated mobile operators in the Supreme Court during argument on the validity of TRAI’s call drop penalties, calling the industry a “cartel” that is

“interested in profiteering at the expense of consumers,” said Attorney-General Mukul Rohatgi.

"This is a cartel of four-five players in a country of a billion," Rohatgi said. "They earn huge revenues and couldn't be bothered about consumer satisfaction."

Rhetorical flourishes aside, many observers of the Indian mobile market would say that is hyperbole unrelated to the realities of the market, which is by almost any measure the most-competitive in the world.

Profit margins have suffered accordingly.

Bharti Airtel and Idea Cellular both posted higher year-on-year net profit in the fourth quarter ended on March 31, 2015.

But Bharti Airtel posted its first sequential profit fall in six quarters while missing estimates. Keep in mind those results include profits from international markets as well, not just India.

Idea, the country's third largest, met the lower end of analyst estimates.

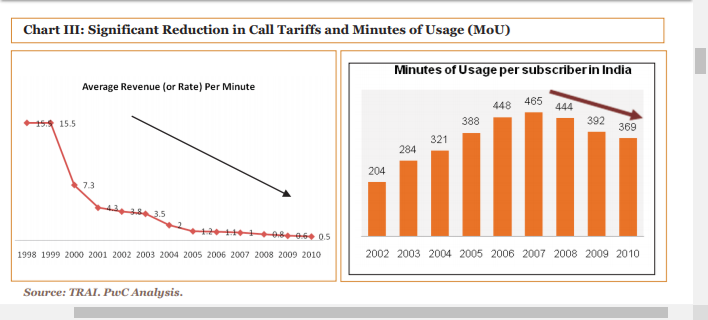

The standout theme for both was the struggling voice business, which accounts for more than 80 percent of overall revenue.

Revenue per minute for Airtel and Idea continued to drop sequentially, dropping in the first quarter of 2015by 2.4 percent and three percent, respectively.

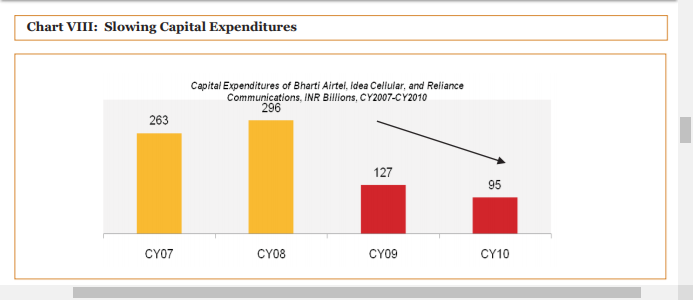

In fact, one might argue, so hyper-competitive is the market that suppliers do not have incentives to invest more heavily. Some believe the situation will worsen as Reliance Jio enters the market.

In 2011, for example, mobile firms in India did not recover their cost of capital. But some might argue earnings have at times in the past been in line with global norms.

On the other hand, operating profit margins for the top five mobile providers in 2014 were in some cases in the low 30 percent range. Operating profit, of course, is not net profit, after all other business costs. Net profits in the 2014 telecommunications business were about 11 percent, according to Investopedia.

The analogy is investment by AT&T and Verizon in copper facilities and legacy voice, rather than next generation mobile networks. Simply, the money gets invested where the revenue, growth and profit lies, not in those parts of the business that are declining and provide low to negative profits.

The point is that profiteering is probably not a fair characterization of the Indian mobile operator business. In fact, low profits would explain behavior better than "profiteering."