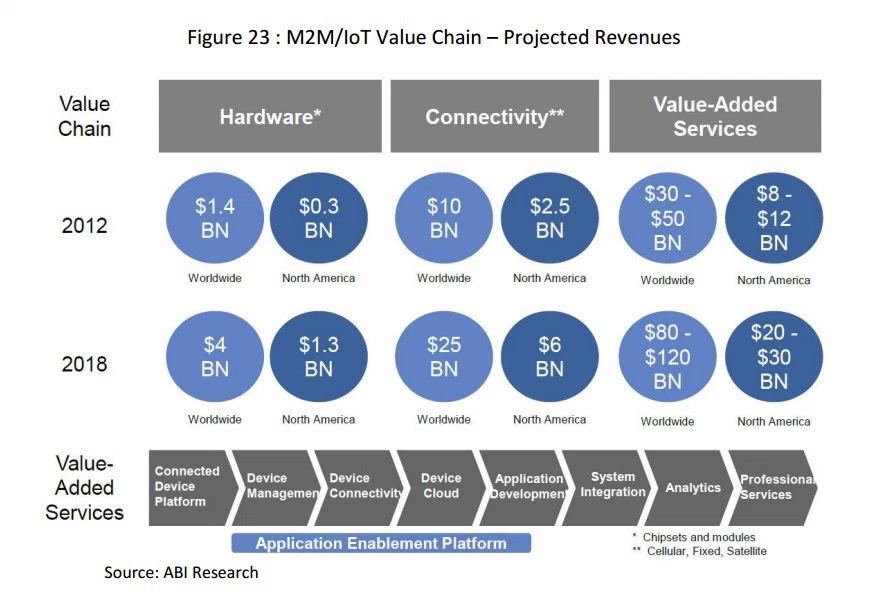

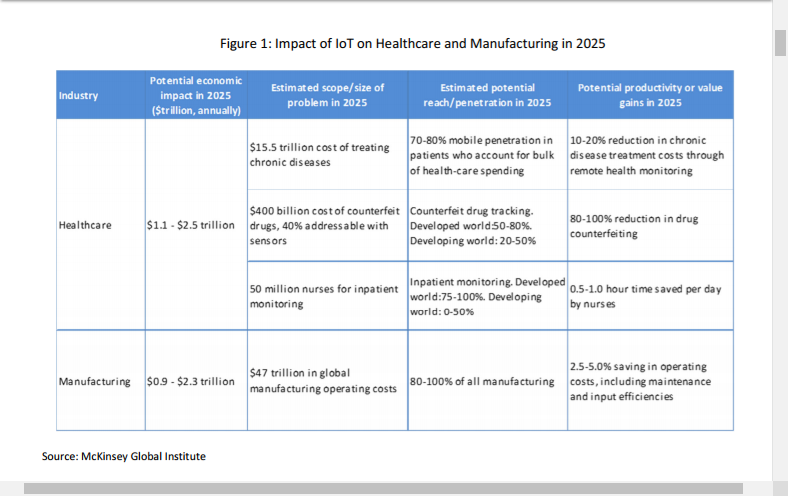

A McKinsey Global Institute study suggests that the Internet of Things has the potential to create economic impact of $2.7 trillion to $6.2 trillion annually by 2025. Connectivity (access) might account for about 16 percent to 17 percent of total ecosystem revenues, according to McKinsey analysts.

Vodafone plans to roll out the narrowband IoT (NB-IoT) platform to support Internet of Things connectivity across multiple markets in 2017, said Vodafone Internet of Things group Director, Erik Brenneis.

As often is the case when new platforms are being commercialized, different tier-one mobile operators are making different bets.

Altice’s SFR is deploying Sigfox while rivals Bouygues and Orange have opted for LoRa. Orange, though, has not ruled out use of other platforms as well.

China Mobile also has chosen to support NB-IoT.

In some ways, the choice of NB-IoT is not too surprising. Historically, tier-one telcos have preferred solutions based on licensed spectrum, and also have preferred options that build on already-established networks and also have perceived “quality of service” advantages. BB-IoT fits within that approach.

“NB-IoT operates in licensed spectrum and that is important to us at Vodafone because we need to deliver a high quality experience to our customers,” said Brenneis.

All of the proposed networks emphasize lower-cost connectivity and lower power consumption.