More U.S. households now seem to be abandoning even fixed Internet access in favor of mobile access, as it now is common for households to rely on mobile voice, instead of fixed network voice, or over the top video entertainment in place of traditional subscription services.

In fact, because of mobile use, fixed network Internet access rates actually are dropping in the United States, having reached an apparent peak in 2011.

Those sorts of trends pose key questions for service providers and regulators, since one has to ask important questions. If consumers are abandoning the fixed network, making the business case more difficult, what is the appropriate service provider investment strategy?

What is the right regulatory approach for services that are declining? Even if “parity” of regulation makes sense when technology platforms change, how much additional cost should regulators be placing on declining services--even services based on the newer platforms?

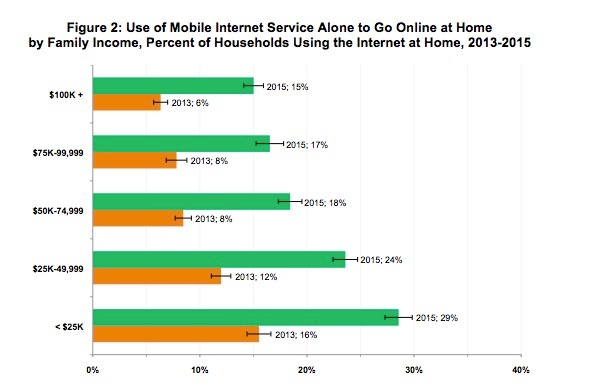

In an almost-unnoticed trend, more U.S. households, in every income bracket, are going “mobile-only” for Internet access at home, in 2015, compared to 2013.

In fact, says the National Telecommunications and Information Administration, between 15 percent and 29 percent of surveyed households now rely solely on mobile platforms for Internet access.

Trends such as the substitution of mobile for fixed access now have altered, or are poised to alter, the methods people use for voice, messaging, TV and Internet access. That has clear implications for service provider strategy and investment and for regulation of fixed services as a whole.

Some of us would argue that it makes little sense to apply more burdensome regulations on platforms that are in decline. Likewise, if the shift is to mobile and wireless communication, then it makes sense to continue allocating more bandwidth for mobile and wireless access.

There are a whole range of subsidiary issues where such choices must be made.

The U.S. Federal Communications Commission wants all ISPs offering IP-based voice services to provide battery backup, as legacy “plain old telephone service” has been line powered.

Frontier Communications says there is very little demand for battery backup for VoIP services, a finding that is consistent with prior consumer behavior.

That position is not surprising, as any universal battery backup plan would impose additional cost. Cable TV providers, for example, seem to have no objection to offering optional battery backup, but oppose mandatory backup for all carrier IP voice lines.

Frontier argues (as have cable TV operators for years) that, even when offered for sale, consumers do not generally buy battery backup services.

Frontier, in fact, argues, that few of its customers actually buy an IP telephony service, in marked contrast to cable TV operators and “fiber to home” providers, which universally offer IP telephony as their only voice option.

Frontier’s experience, in large part, also shows that the company continues to rely on legacy voice, instead of offering IP telephony. In large part, that is because the company does not use fiber to home platforms on a ubiquitous basis, which virtually requires that voice be provided using IP telephony.

Frontier notes that, according to the FCC’s most recent voice telephone services report, for all ILECs nationwide there are only 26,000 residential customers that actually use an OTT interconnected voice (IP telephony) product.

That hardly seems right, but appears to be a definitional issue. The FCC reported there were 48 million interconnected voice subscriptions in use by December 31, 2013. So Frontier clearly is using some definition of “connected voice” that is different from that used by the FCC.

That noted, given the prevalence of mobile service, rare in the extreme is a household that actually relies solely on fixed network voice.