Though some desired business outcomes from Internet of Things advances will reduce the cost of inputs such as energy, arguably the biggest benefits will come from direct impact on business models or policy outcomes (lower air pollution, less traffic, accidents avoided, equipment protected, lives saved).

IoT sensors, for example, could help insurance companies better assess risk, and therefore premiums, charged to its customers. That is one direct benefit of connected air applications.

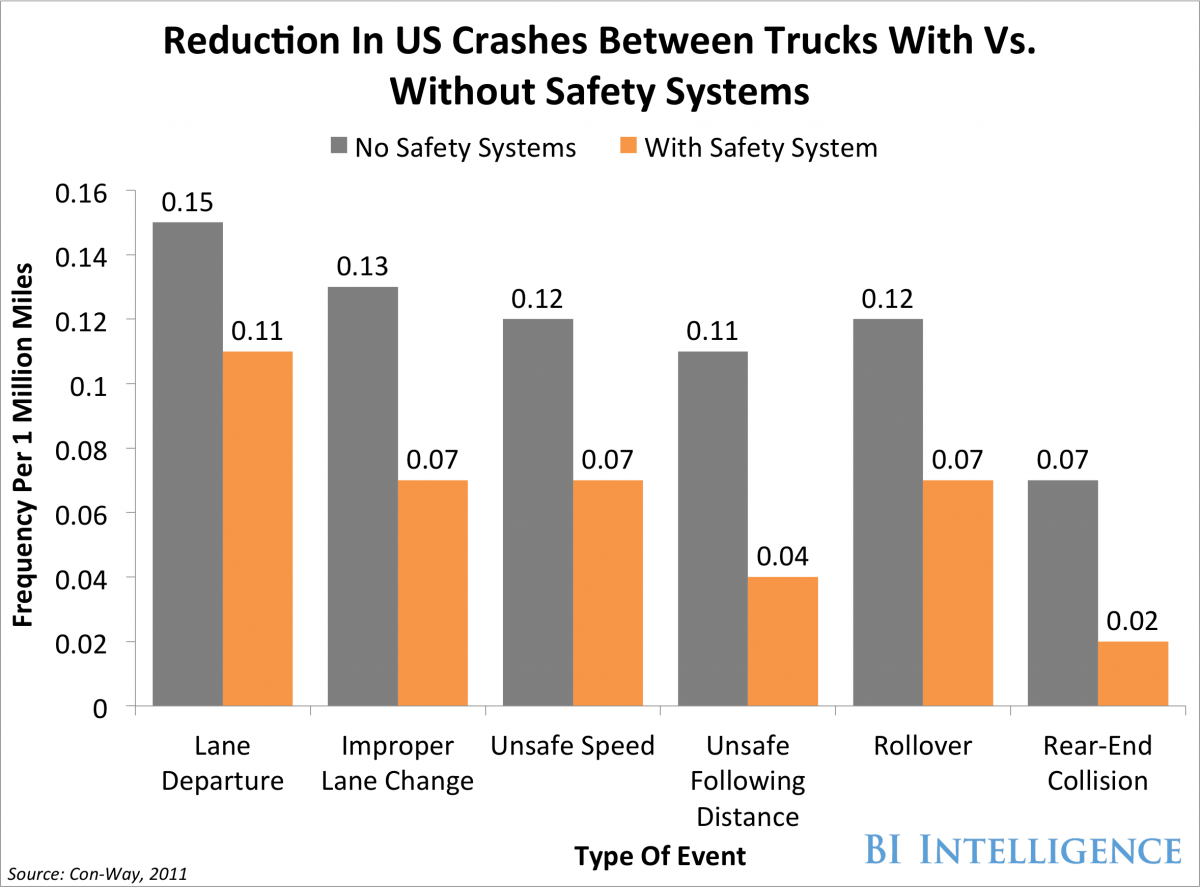

Since the basis of the insurance model is risk arbitrage, IoT sensors would help in several ways, allowing companies to safely provide “safe driver” discounts, while better matching premiums to risk in other cases.

That is one reason connected car applications are seen as early adopters: there are advantages for drivers (safe drivers, at any rate) and insurance companies. When an innovation had tangible benefits for both buyers and sellers, adoption can occur faster, because there is less friction (inertia or resistance).

Since the basis of the insurance model is risk arbitrage, IoT sensors would help in several ways, allowing companies to safely provide “safe driver” discounts, while better matching premiums to risk in other cases.

That is one reason connected car applications are seen as early adopters: there are advantages for drivers (safe drivers, at any rate) and insurance companies. When an innovation had tangible benefits for both buyers and sellers, adoption can occur faster, because there is less friction (inertia or resistance).