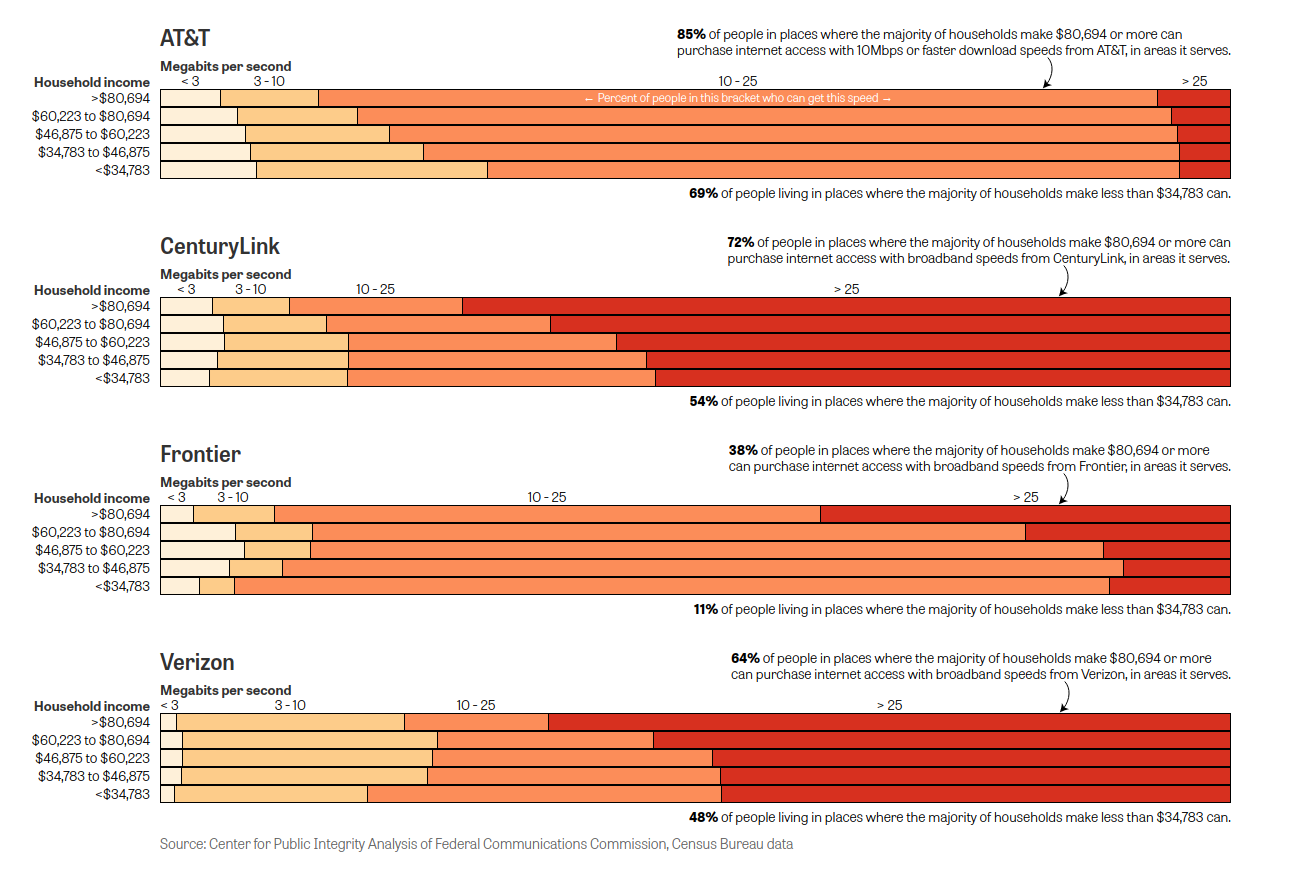

In a study, the Center for Public Integrity argues “the largest non-cable internet providers collectively offer faster speeds to about 40 percent of the population they serve nationwide in wealthy areas compared with just 22 percent of the population in poor areas.”

In a study, the Center for Public Integrity argues “the largest non-cable internet providers collectively offer faster speeds to about 40 percent of the population they serve nationwide in wealthy areas compared with just 22 percent of the population in poor areas.”

The argument is that the large telcos have rather systematically targeted network upgrades to “wealthier” communities, compared to “poorer” communities.

There is statistical truth to those claims. Any analysis of urban-rural Internet access speeds would show that rural speeds are generally much slower than urban speeds, and that urban household incomes are generally higher than rural incomes.

Hence, it is is statistically correct to argue that speeds are, in fact, faster in urban (wealthier) areas, compared to rural (poorer) areas.

It might also be correct to argue that top speeds in some poorer neighborhoods are slower than top speeds in more-upscale neighborhoods.

The reality is that several obvious issues are at work. Telco copper network speeds are distance sensitive. That is one reason why rural networks have been “slower” than urban networks, as a rule.

Customer density is far lower in rural areas, which is why it is hard to justify the same investment in rural areas, compared to urban areas.

Also, upgrading even some urban properties--especially multiple dwelling units--is less than straightforward, as building owners can block or delay installation of new facilities.

Beyond all that, communications policy related to Internet access facilities never has been governed by “common carrier” regulation that mandates universal access and comparable prices for the same classes of service, or even minimum levels of service.

In fact, precisely because incentives matter, where it comes to next-generation facilities, mobile and fixed service providers have traditionally had more leeway to build facilities in some areas first, in other areas later, to avoid building, in many cases.

Service providers are free, for example, to build new networks to serve business customers only, and not consumers; large businesses in preference to small businesses; or businesses in some areas and not others.

In fact, municipal authorities now have taken that same approach and applied it to next generation networks serving consumers. That is why Google Fiber is allowed to build in some neighborhoods, and not others, or to build first in some neighborhoods, and not others.

That approach has changed AT&T and Verizon thinking about deployment of fiber to home and gigabit networks, as well. Building first where there is higher demand drives more investment. It also means disparities will widen, for a time.

So, yes, the CPI study does show disparities. But the explanation is partly for reasons of regulatory frameworks, incentives for investment, the physical properties of telco copper networks, population density, property owner rights and end user demand for services, as well as income disparities.

That is not to condone the disparities. But it is a reality of the business model that networks are far more expensive in rural areas than urban areas, while demand is more robust in business customer segments than consumer; higher in wealthier neighborhoods than poorer ones.

There likely are disparities by age, marital status, children in household and regional differences, as well.

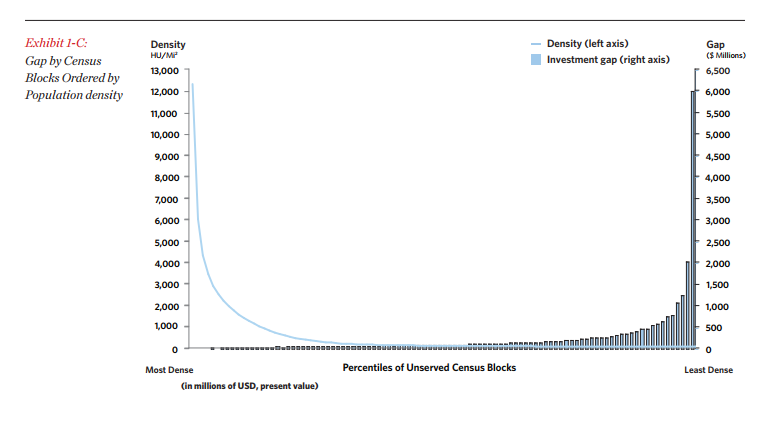

As this analysis by the FCC shows, high population density means affordable network cost. Conversely, low population density means high network cost.

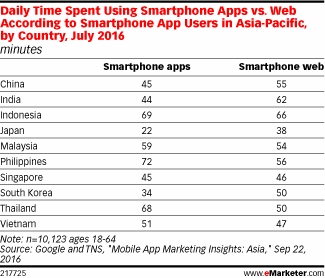

Global statistics can obscure more than they reveal, and that is true for the Asia-Pacific region as well.

Global statistics can obscure more than they reveal, and that is true for the Asia-Pacific region as well.