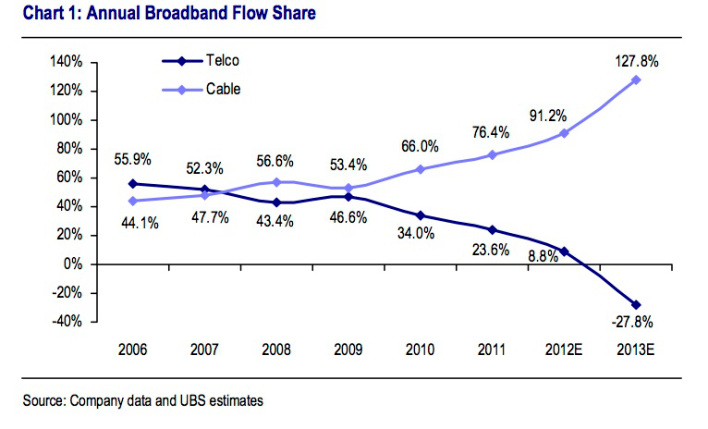

It always comes as a bit of a shock when an analyst suggests a core product will never grow again. But that is precisely what Jeffrey Wlodarczak, Pivotal Research CEO, says about U.S. fixed network telco chances to make net additions to their high speed access accounts.

“With cable aggressively ramping their speeds (boosted by the widespread rollout of DOCSIS 3.1 technology [and its promise of widespread 1 gig + download speeds]) it is a reasonable assumption that the telcos may never generate positive net fixed data subscriber growth again," he says.

In fact, U.S. cable companies have been taking market share in the fixed network high speed access market for years. In 2016, for example, U.S. cable TV companies will capture all the net account growth in the internet access market.

That happened in 2015 as well, when cable got all the net growth in high speed access accounts. In fact, cable companies have outgained telcos every year since 2007, in terms of net additions.