Some observers point out that the higher costs of 5G networks--driven by small cell architectures and the need for more backhaul and more radio sites--is going to mean 5G networks cost more than 4G networks. Logic suggests the merit of that view. Macrocell networks (4G and earlier generations) require fewer towers, sites, radios, frequency coordination and backhaul than microcell networks.

And that means a current problem--return on invested capital--is going to become even more important in the 5G era.

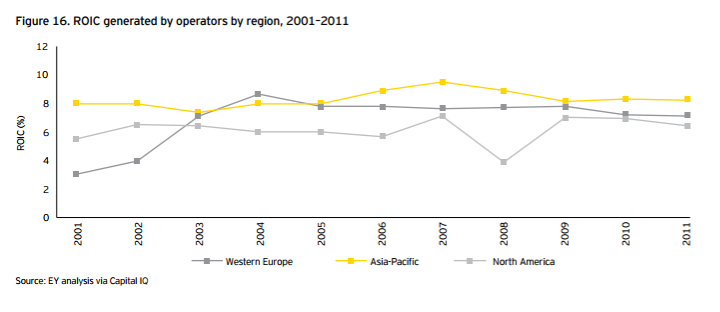

Return on invested capital, not earnings (EBITDA) or cash flow, now is the way major telcos have to measure business results, argue analysts at PwC. The fundamental reason is that “growth is gone and it’s not coming back,” say PwC analysts. “Downward trends in return on invested capital (ROIC) are the result of a number of factors, from regulated price reductions to cannibalization of legacy revenues by OTTs, along with high capital intensity required to support demand for data,” say researchers at EY.

So if revenue growth is muted, what matters is how well access providers monetize invested capital. That is not going to be easy.

Philippines telco Globe Telecom had a return on capital of about 7.7 percent in the third quarter of 2016. Airtel in India points out that, in 2016, some Indian telcos might have had a one-percent return on capital.

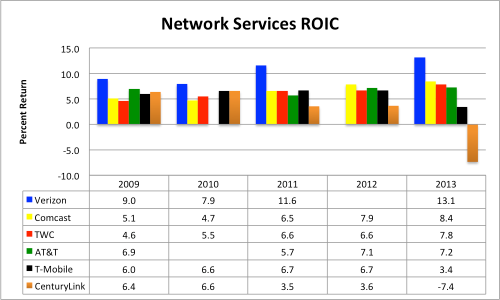

That 7.7 percent rate is about in line with global telecom firm financial returns from the 1990s until perhaps 2006. But there can be wide variation. In the U.S. market, in 2013, Verizon has ROIC of more than 13 percent, while CenturyLink has ROIC of minus 7.4 percent.

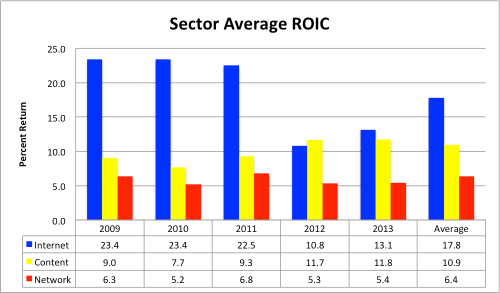

ROIC issues for access services are one reason why the strategy of “moving up the stack” or “up the value chain” continues to be relevant and necessary for at least the larger telcos, cable companies and similar access providers. Mergers to gain scale will help, in many cases, but the fundamental problem--lack of organic growth for network services--will be a key constraint.

Market consolidation, in many cases, also will help, as market share and financial return tend to be correlated.