One might argue--based on history--that many firms and segments within the telecom ecosystem should not try and “move up the stack” (occupy new roles within the ecosystem), while some firms and segments have no choice but to try and do so.

One line of argument it that such moves are highly risky, and rarely succeed. That is true for any large firm, and not specific to the telecom industry.

A second set of arguments is that, in some parts of the ecosystem, the core business is, in fact, dumb pipe, and cannot easily be augmented or changed. That might well be nearly-completely true in the trans-ocean capacity business, arguably much less true in other retail parts of the business.

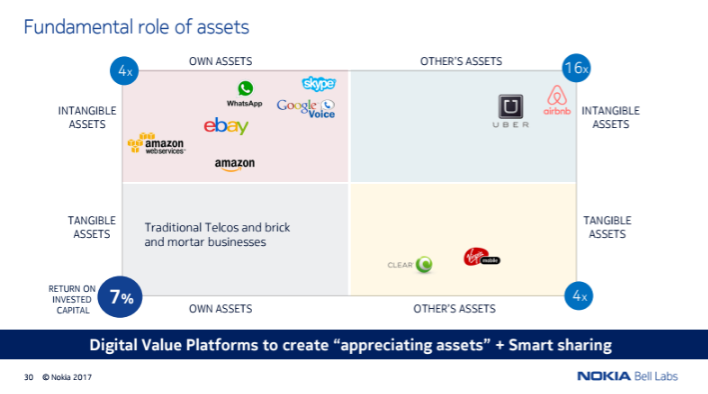

Consider return on capital, which for a telco might be seven percent (or less) on invested capital. App providers can earn 28 percent returns. In other cases, where marketplaces can be created to connect asset owners and customers directly, ROIC can be as high as 112 percent.

Source: Sanjay Kamat, Bell Labs

A final set of arguments might simply deal with the cost of such moves, weighed against other competing needs for capital, the impact on debt loads and the costliness of such assets, when purchased with telco currency (equity market valuations of telco buyers and app sellers).

To begin with, there is substantial evidence that all large acquisitions are difficult, and often fail to bring the hoped-for advantages. In fact, KPMG has argued that as many as 83 percent of mergers and acquisitions fail on one or more dimensions. Other studies suggest failure rates range between 70 percent and 90 percent.

A tier-one service provider, operating at scale, likewise needs scale even in its new business ventures, so such risks are nearly impossible to avoid.

Telco executives who actually have tried various means to occupy new roles, with new revenue models and revenue streams, know just how difficult this is to accomplish. On the other hand, they also know that amassing scale by making horizontal acquisitions (buying other service providers) most often does work, at least temporarily, in building scale, gaining efficiencies and growing gross revenue and possibly profit margins as well.

At a cultural and skills level, such efforts to create new roles within the ecosystem necessarily mean moving outside a self-understood “area of core competency.” At a practical level, this almost always happens by means of acquisition, since it is hard to gain measurable revenue impact when investing in a startup, or any other small firm, no matter how promising.

It is harder to evaluate the argument that moves “up the stack” into new roles within the ecosystem might well be impossible for some actors. It always is harder for small firms, undercapitalized firms and firms operating in smaller revenue niches.

Much of the reason is the cost of such moves (taking on debt, diluting a currency, buying a high market multiple asset with a low market multiple currency).

Telcos have a problem in that regard, as equity markets apply a low multiple of revenue to telco revenue, and a higher multiple of revenue to application (over the top) assets.

The point is that moving into new roles within the telecom, internet or business ecosystem is risky and expensive, when it is possible at all. So for many actors, if a particular role in the ecosystem becomes relatively less attractive, horizontal acquisitions, and then harvesting assets until an asset sale can be managed, is the logical strategy.

In a contracting industry, which the telecom industry already has become, in some markets, consolidation therefore becomes inevitable, as does profit margin pressure. In some instances, we must hope, at least some tier-one providers will make a successful move into adjacent roles in the ecosystem, offering not only new revenue sources and different business models, but also higher profit margins.