Very few firms in the global telecom service provider business are likely to make significant moves to vertically integrate into other elements of the business. In part that is because such moves entail lots of execution risk (moving outside the perceived core competence), lots of capital and lots of scale.

The market is too risky and unreliable—it "fails";

Companies in adjacent stages of the industry chain have more market power than companies in your stage;

Integration would create or exploit market power by raising barriers to entry or allowing price discrimination across customer segments; or

The market is young and the company must forward integrate to develop a market, or the market is declining and independents are pulling out of adjacent stages.

Generally speaking, “failing” markets have one or just a few buyers and sellers, a situation guaranteed to lead to big efforts to gain and sustain advantage. The relationship between content owners and distributors is a good example of such instances, and therefore also a reason vertically integrating content and content distribution makes sense, as Comcast and AT&T have done.

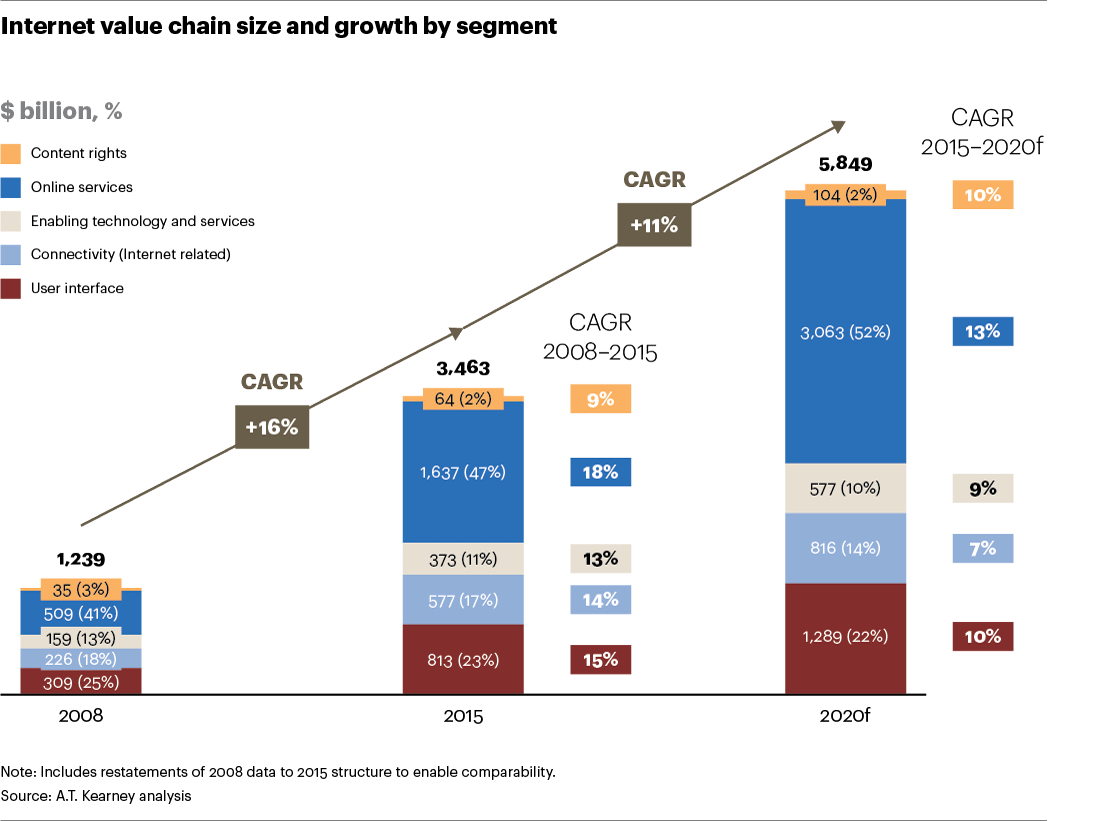

Another instance where vertical integration makes sense is when market power is held by others in the value chain or ecosystem. Consider the internet ecosystem, where devices claim about 15 percent of revenue and internet access about 14 percent, while application providers get about 18 percent.

Over time, revenue claimed by app providers will grow faster than any other segment. That likewise makes vertical integration rational for at least some tier-one service providers.

One way of describing the dynamic is to argue that “you have to own at least some of the content and apps flowing over your network.” In other words, own the actual apps, not simply the access pipe.

Vertical integration, in the internet era, can confer the traditional advantages of raising barriers to entry. When the leaders in one app segment can integrate the leaders in other strategic app segments, entry barriers arguably are created. That is the logic behind the “winner take all” trend in applications generally.

That typically does work so well with communications service providers, who rarely have the market dominance some leading app providers have attained.

Whether telecom becomes a declining market could affect the usefulness of a vertical integration strategy where service providers move to occupy other adjacencies. You might argue that moves into content ownership illustrate that trend.

The internet of things markets might provide another incentive to vertically integrate, though it is not yet clear.

But most service providers will not have the requisite scale to make such moves, sustain them and wring business value out of them.

It is getting harder these days to illustrate the structure of telecom value chain layers. Traditionally, the seven-layer open systems interconnect model had the physical layer at the bottom, the applications layer at the top. Originally developed as a framework for data communications, the stack later became seen as a sort of metaphor for business value as well.

In that scenario, customers might constitute something of a layer eight, driving the revenue model. And some might add a new layer zero of actual physical network elements. More relevant is the addition of a layer for devices, which some place below the communications layer, while others might place the device layer above the communication layer.

Precisely where such layers are placed probably does not matter so much as the understanding that vertical integration can occur both forward (towards customers and retail distribution) or backwards (“down the stack” to incorporate inputs).

As a practical matter, for telecom service providers, the issues are to move either up the stack or down the stack to enhance the value of the present business, especially by adding different revenue sources.

In the monopoly past, creation of network infrastructure elements and architectures, as well as devices, was handled internally, in some cases, by entities such as Western Electric, with development work handled by Bell Laboratories, for instance.

All that changed with deregulation, as the service provider functions (in the U.S. market) were broken into a couple of roles, while research and manufacturing likewise were separated. Western Electric the internal operation became Lucent the independent unit. The research function (Bell Labs) was spun off to AT&T, which operated solely in the area of long distance services, while the “Baby Bells” were created to handle local access.

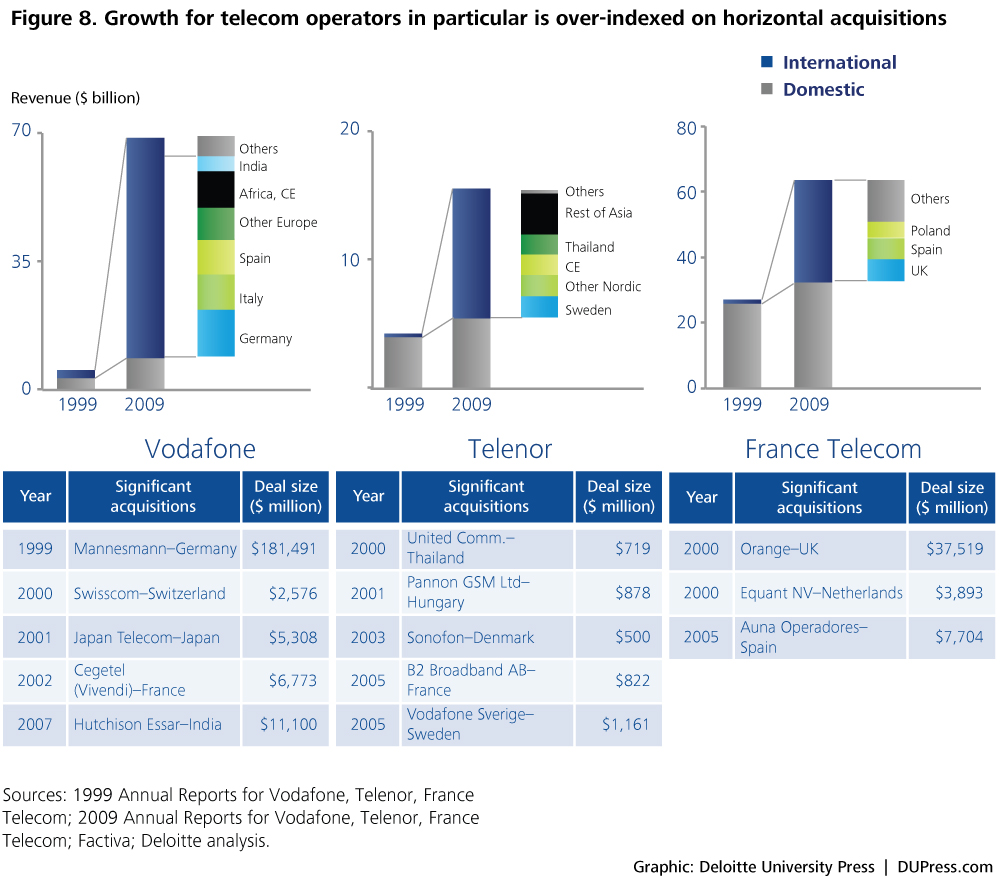

In some cases, vertical integration might prove useful. But most service providers are going to move horizontally, to gain scale in the present business. That has proven the most-prevalent revenue growth strategy in the telecom business over the last four or five decades.

source: Deloitte