The internet era is fundamentally different from all prior eras of telecommunications. “Telecom” once was the center of its own universe. These days, telecom is part of the internet ecosystem. And some of us would argue telecom essentially is a tail on an internet ecosystem dog.

In large part, that means the industry cannot independently determine its own destiny, but supports, reflects upon and builds on other key trends in consumer behavior, device use, app use and enterprise priorities.

For that reason, argues the GSMA, “it is no longer appropriate to develop corporate strategies, or to assess policy situations, with a narrow focus on a single segment of the value chain.” In other words, the business context has changed. Boundaries between formerly-distinct industries have become porous, and actors in one part of the value chain now routinely expand into additional roles.

The implications for service providers--at least tier-one providers--are clear: movement beyond the access and transport function are within the realm of necessity and reason. You might compare such options to the older notions of vertical integration. The business logic is the same.

Sometimes revenue growth, profit or cost control is enhanced when firms operate across more of the value chain.

There is an important caveat, though.

It might not be possible for small service providers to contemplate strategies that include operations across multiple parts of the ecosystem. Large entities, whether app providers, device suppliers or access providers, can reasonably expect to have the scale necessary for success across multiple roles.

Smaller providers, for reasons of scale (or lack of scale), will have to adapt to more specialized roles, as smaller participants in the core telecom ecosystem always have done.

That does not mean awareness of the trend is unimportant. Small providers have to understand where opportunities exist within the larger ecosystem, and as potential partners for tier-one actors who do operate across multiple roles.

Precisely how many tier-one telcos actually might envision a substantial role across multiple areas of the ecosystem (apps, services, devices, access, advertising) is unclear, but it will be a relatively small subset of the universe of service providers.

When researchers at Nokia Bell Labs predict a consolidation of some 810 global service providers to perhaps 105 within a decade, that gives you some idea of the universe of possibilities. As only the largest app providers are able to occupy meaningful positions across the ecosystem, so only a few of the largest service providers can contemplate similar moves.

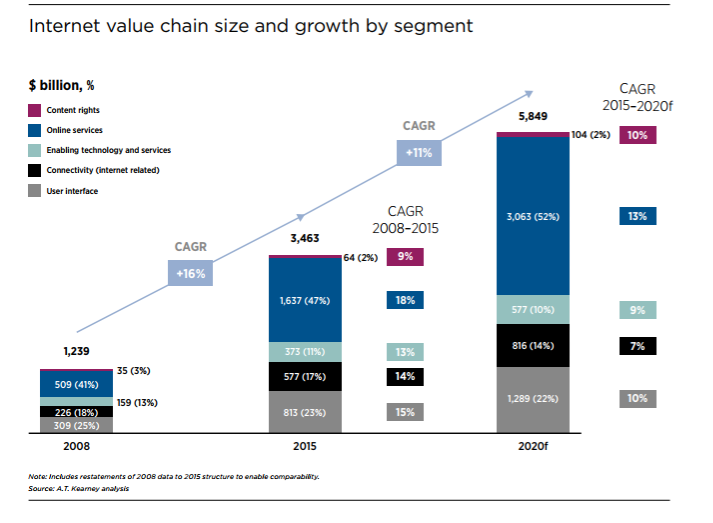

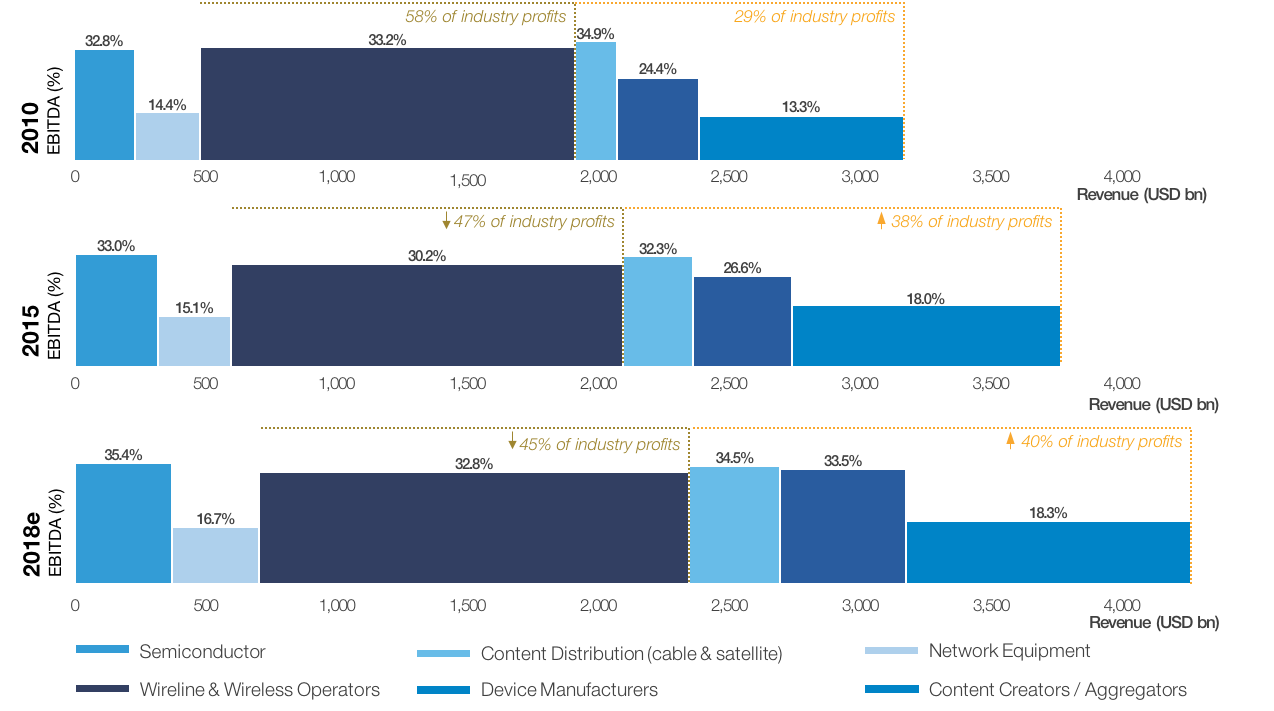

The internet value chain has almost trebled from $1.2 trillion in 2008 to almost $3.5 trillion in 2015, a compound annual growth rate of 16 per cent, according to the GSMA. So the ecosystem has grown substantially. So has the gross amount of revenue earned by the global service provider industry. But the percentage of total value earned by service providers is dropping.

The implications are perhaps obvious.

We sometimes forget that the global telecom business had, for most of its history, been about the sale of apps (services), not “access” to such apps. In other words, consumers and businesses bought the right to make phone calls, and not the right to access a network to make phone calls.

The difference is subtle, but crucial. “Phone companies” were in the “make a phone call” business, not the “network access” business. In the internet era, the value proposition flips.

If access to the internet now is among the primary values, if not the exclusive value, service providers now are in several businesses. “Access to the internet” (dumb pipe) drives significant revenue. But so do “apps” (voice, messaging, video entertainment).

So a core part of strategy is to grow the portion of the business related to apps or services, compared to lower-value “access.” That especially is true if one believes there are clear limits to the amount consumers ever will spend on access services.

The point is that growth options for providers that remain in the access services business (voice, messaging, video, internet access) are probably limited, going forward. Gaining scale (making acquisitions, especially outside the existing geography) will help, for a while. The limit there is the availability of capital and acquisition targets.

As always, that will spur a search for niches. As in the past, those niches will tend to be smaller or specialized segments that a tier-one service provider simply cannot support and make a profit. Rural geographies, local geographies and specialized business services have provided opportunities in the past. That should continue.

In the internet era, successes in other areas are harder to identify, with few clear sustainable advantages for carrier-supplied voice or messaging apps or app stores. There might be new advantages for some carrier-supported devices in some markets, especially where a service provider can use its own branded handsets to drive market share gains.

Language-specific content also could be promising.

The larger point is that, in the internet era, opportunities often are shaped by what other segments of the value chain will allow.