Building a $66 million, municipal ISP network would be "marginally" viable at a 28 percent "take" rate, a study by Colorado firm Uptown Services predicted in 2015.

That might be an optimistic expectation of market share for any well-run ISP operating a fiber-to-home network and competing against a elco and a cable TV operator where one or both of those competitors are vulnerable because they have not, or cannot, invest in their own networks.

Much hinges on whether the Hillsboro network plans also to sell video service or voice. If not, actual take rates might be as low as 20 percent, and possibly lower.

Many municipal ISPs that report adoption rates (penetration, or the percent of homes passed that actually buy service) boosted by their sales of video and voice services. So the adoption rate is based on “units of service sold,” not the “number of homes buying service.”

At least so far, where a municipal ISP offers only internet access, early adoption rates--even with highly-competitive prices, have been in single digits.

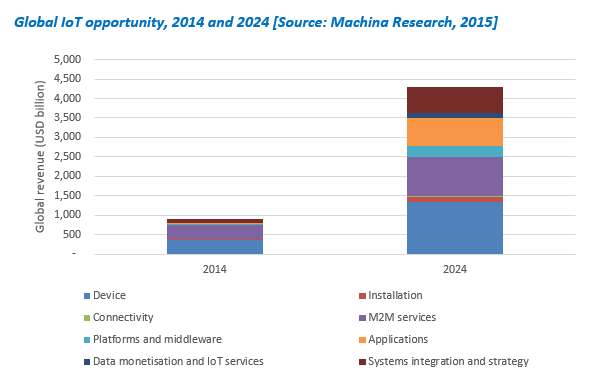

Penetration: Units Sold or Homes Buying Service?

| |||||

Morristown

|

Chattanooga

|

Bristol

|

Cedar Falls

|

Longmont

| |

homes passed

|

14500

|

140000

|

16800

|

15000

|

4000

|

subscribers

|

5600

|

70000

|

12700

|

13000

|

500

|

units sold

|

39%

|

50%

|

76%

|

87%

|

13%

|

services sold

|

3

|

3

|

5

|

3

|

2

|

HH buys .66 =

|

2

|

2

|

3

|

2

|

1

|

Homes served

|

2828

|

35354

|

3848

|

6566

|

379

|

penetration

|

20%

|

25%

|

23%

|

44%

|

9%

|

Some private ISPs would, and have, taken such a chances. Numerous cities and towns seem to be considering the option, as well.

The consultants estimate the Hillsboro municipal ISP operation would reach cash positive operations in 13 or 14 years, using the $50 per month benchmark. That might be too optimistic. Higher prices seem to part of the business model for other municipal broadband networks.

But city officials have decided to build the municipal broadband network anyway. It will not be easy.

Municipal ISPs enjoy no advantages in capital investment and perhaps marginal advantages in the make-ready and pole attachment cost areas. Any hope for enough operating efficiencies to sell service at $50 a month would presumably have to come in marketing and operating cost areas comparable to best practices seen at some private ISPs (Sonic, Tucows).

If successful, such networks generally result in lower prices, to be sure. But the proposed Hillsboro network might be seen as a key test of whether such networks can compete in suburban markets.

Traditionally, the opportunity for municipal broadband has seemed more realistic in rural markets and for smaller towns. The Hillsboro network might be likened to the network Ting is building in Centennial, Colo., a reasonably prosperous suburb of Denver.

Hillsboro possibly will be an important test case of the business model. Few private investors would be able to wait more than a decade simply to reach cash flow positive status, to say nothing of earning enough money to earn a profit after two decades or so.