“Bothersome experiences” and “shopping delights” are thought by most people to be drivers of retailer abandonment, in the former case, or customer loyalty, in the latter case. Most of us tend to think of the full range of things a supplier does, or fails to do, that can move buyer perceptions in either direction.

Applied to the connectivity business, outages, incorrect billing, long waits for customer service, high perceived prices and low perceived quality of service are seen as drivers of churn. The logical thought is that high availability, correct bills, prompt customer service, reasonable prices and high value are seen as drivers of customer loyalty.

But an argument can be made that the bothersome and delightful dimensions of experience are not linear, on a single scale, but perhaps even two different categories: things that bother customers and need to be avoided, as well as things that delight customers, and have to be created.

In that view, you cannot delight customers by removing irritation: one only removes the bother and the risk of customer abandonment. In other words, no retailer creates delight simply by removing sources of unhappiness. Consider the results of studies by Qualtrics.

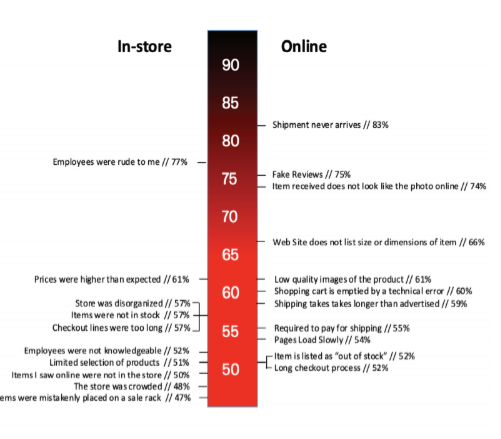

In-store irritants (complaints) include rude employees, high prices, items not in stock and long checkout lines. Online irritants include shipments that do not arrive, fake product reviews or misleading or inaccurate descriptions and depictions.

Say any given retailer has all those problems. Say those problems, at significant effort and expense, get fixed.

So now customers in stores encounter courteous employees, reasonable prices, items always in stock and fast checkout. Is that enough to produce “delight?” Maybe not. Maybe that is what customers shopping in stores simply expect. So the reasons to avoid shopping are removed.

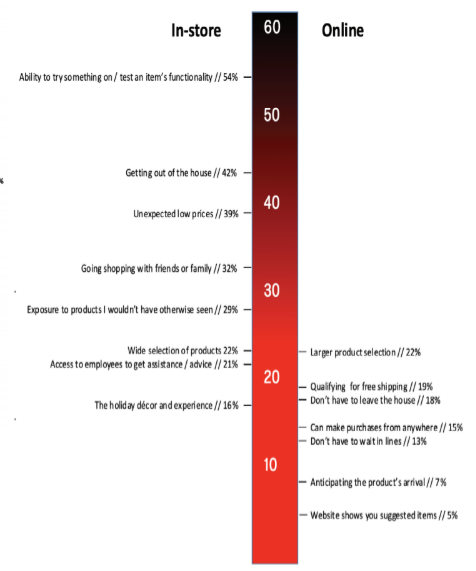

The single exception is price, in the in-store context. Shopping are irritated by high prices, and report enjoying unexpectedly low prices. With that exception, the irritant issues and enjoyment values do not overlap.

In an online context, say a retailer fixes irritants by improving logistics, the quality and accuracy of product reviews and descriptions. Again, the question is whether doing so creates a sense of buyer delight, or simply removes a reason not to use the site.

Now consider feedback from shoppers about what they most enjoy about particular retail or online shopping experiences. In-store, the ability to try on a garment, being able to “get out of the house,” unexpectedly-low prices, doing something with friends or family, and serendipitous exposure to products are positives.

Online, shoppers value larger product selection, free shipping, the ability to shop from anywhere and avoiding checkout lines as drivers of enjoyment. None of the major online “enjoyment” drivers are directly related to the complaints.

In-Store and Online Complaint and Enjoyment Drivers

| |||

In-Store irritant

|

In-Store enjoy

|

Online irritant

|

Online enjoy

|

Employee rudeness

|

Try on garment

|

Item did not arrive

|

Product selection

|

High prices

|

Low prices

|

Fake reviews

|

Shop anywhere

|

Merchandise unavailable

|

Get out of house

|

Misleading description

|

Free shipping

|

Long checkout

|

Be with friends

|

Low quality

|

No checkout line

|

Serendipity

|

Shopping cart

|

No need to leave house

| |

The point is that it is perhaps not so clear that all consumer interaction issues are on a single scale: high to low, good to bad, irritant or enjoyment.

Instead, there are at least two different scales: presence or absence of “things that irritate consumers,” and presence or absence of “things that delight customers.”

With the possible exception of an expectation of high in-store prices and unexpectedly low store prices, irritants and pleasures do not seem to be on the same scales. They appear to be different dimensions of experience.