Saturday, June 15, 2019

AT&T View of Fixed Wireless for Internet Access

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, June 14, 2019

U.S. Fixed Network Internet Access Market Could be 5% Away from Full Adoption

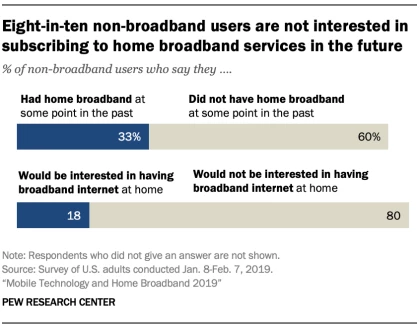

Consumers sometimes make surprising choices. Consider that 60 percent of people surveyed by the Pew Research Center who do not buy a fixed network internet access service say they never have had high-speed internet service at home in the past.

Some 33 percent say they have had fixed network internet in the past.

But the most-surprising finding is that “most non-adopters are unenthusiastic about the prospect” of buying fixed network access. “Fully 80 percent of non-broadband users say they would not be interested in having broadband at home,” the researchers note.

It is not that they cannot buy it, because the service is not available, nor necessarily because the service is too expensive. Rather, many consumers simply feel their smartphones do everything they need, where it comes to internet apps and services.

That implies that 100-percent fixed network broadband adoption is about 78 percent (present buyers and 20 percent of the non-buyers). Adoption at the moment is 73 percent, suggesting there is about five percent more adoption before the market is fully saturated, and every potential buyer already is a customer.

That is important when assessing the state of internet access adoption in the U.S. market. The percentage of survey respondents who say they have broadband service at home grew from 65 percent in 2018 to 73 percent in 2019.

Some 27 percent of survey respondents do not buy the product, say researchers at Pew Research Center. “And growing shares of these non-adopters cite their mobile phone as a reason for not subscribing to these services.”

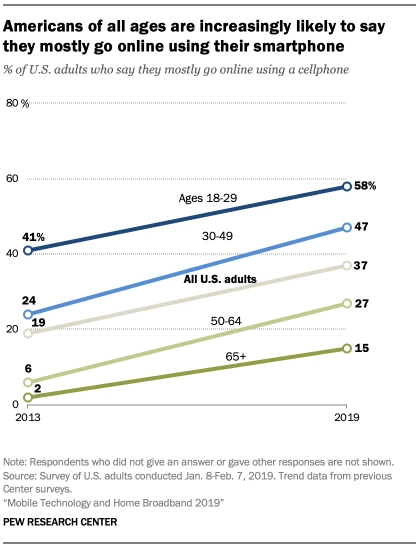

Even in advance of 5G, which will in many cases become a full substitute for fixed network internet access, 17 percent of survey respondents say they already are “mobile only” for internet access.

As has been true in the past, income and education play key roles in propensity to purchase fixed network internet access. Some 92 percent of adults from households earning $75,000 or more a year say they have broadband internet at home, but that share falls to 56 percent among those whose annual household income falls below $30,000, according to the Pew Research Center.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, June 11, 2019

China Now Accounts for 21% of Global Internet Users

China now accounts for 21 percent of global internet users; India 12 percent; the United States eight percent, according to Bondcap analyst Mary Meeker. Based on population, China and India eventually will represent even more share.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

U.S. Households Might Spend 1.2% to 2.8% of Household Income on Voice Services

According to U.S. Bureau of Labor Statistics data, households headed by an occupant who did not graduate from high school spend a bit less than three percent of household income (2.8 percent) on phone service.

Households headed by an occupant with a graduate degree tend to spend about 1.2 percent of household income on phone service.

The differences seem to flow from household income, which BLS data shows varies directly with educational level.

It is not clear how spending on video services and internet access varies with educational level and income, as those services seem not to be directly tracked by BLS.

Household Spending, Homes Headed by Occupant with Less than High School Education, $28,245 in spending (98.5% of total income), 2.2 people (0.7 income earners, 0.6 children, and 0.5 seniors)

Household Spending, Homes Headed by Occupant with a High School diploma, $35,036 in spending (87.3% of total income), 2.3 people (1.0 income earners, 0.6 children, and 0.4 seniors)

Households headed by high school graduates, with income of $40,147 and 2.3 occupants spend about the same--2.7 percent of income--on phone services.

Households headed by an occupant with a bachelor’s degree, with $92,409 in income, spend about 1.7 percent of income on phone services.

Household Spending, Homes Headed by Occupant with a Bachelor’s Degree, $63,373 in spending, 2.5 people (1.5 income earners, 0.6 children, and 0.4 seniors)

Households headed by an occupant with a graduate degree spend about 1.2 percent of income on phone services.

Household Spending, Homes Headed by Occupant with a Graduate Degree, $83,593 in spending (62.9% of total income), average of 2.6 people (1.5 income earners, 0.6 children, and 0.4 seniors)

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

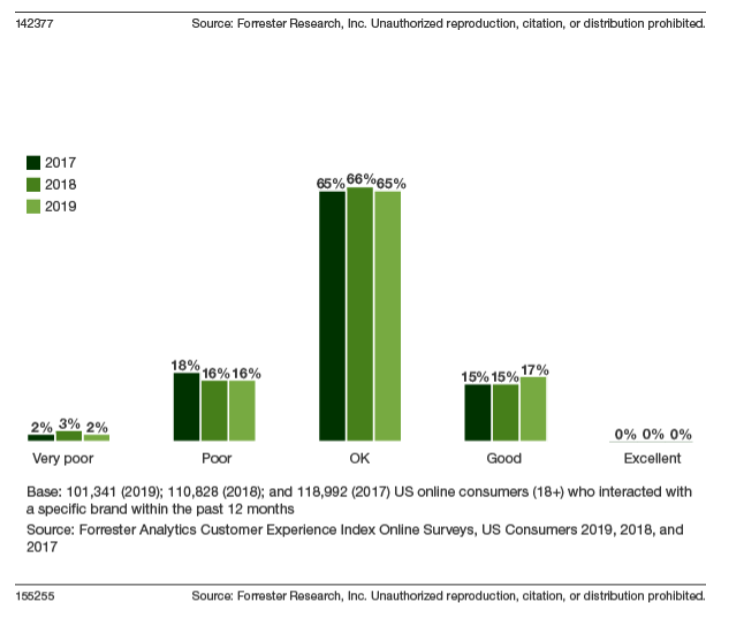

Most Firms are "Average" for Customer Experience

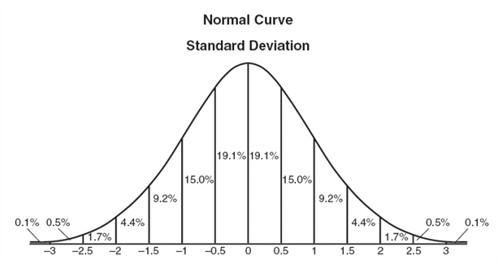

The Forrester Research 2019 “U.S. Customer Experience Index,” a study of customer experience for 260 brands in 16 industries, looks like a classic “Bell curve,” or standard distribution or standard deviation, where 50 percent of the distribution lies to the left of the mean and 50 percent lies to the right of the mean.

Simply put, the Forrester data suggests most firms are close to “average” in customer-reported experience. Roughly two thirds of firms are rated “okay.” About 16 percent get “good” or “poor” ratings. A very-small percentage get “excellent” or “very poor” ratings.

No executive or employee probably enjoys being “average.” Most firms tend to say their customer service, or customer satisfaction is good or excellent or at least better than most of its competitors and peers. The Forrester Research tends to confirm that customers do not see matters that way.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, June 10, 2019

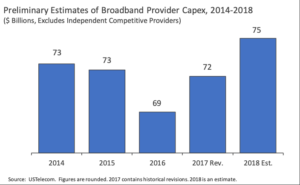

U.S. ISP Capex Rose $3 Billion in 2018

U.S. service provider capital investment increased by approximately $3 billion in 2018, according to US Telecom.

USTelecom estimates that U.S. internet service providers invested $75 billion in 2018, up from $72 billion the prior year, and up $6 billion from the 2016 low US Telecom says was the result of common carrier regulation.

“The decline in capital investment starting in 2015 and the recovery that started in 2017 suggest the likelihood of a negative regulatory impact from the 2015 utility classification of broadband providers and, conversely, a positive impact from a return to a more forward-looking policy environment in 2017,” US Telecom says.

The caveat is that “many factors affect company investment decisions, such as macroeconomic conditions, technological developments, capital costs, taxes, competitive upgrade cycles, and regulation,” US Telecom also says.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

5G Has Different Value for Consumers and Suppliers

For most consumer mobility apps, 5G represents not so much an experience changer as an experience-maintaining development. While some new use cases will probably depend on both 5G and edge computing, the value of 5G for most consumer smartphone apps is that it allows the network to support ever-increasing data consumption.

For most use cases, 4G latency performance and speeds are likely not a problem. What is a problem is the cost of usage. Consumers are price resistant for all products, but likely especially so for data usage charges. No matter how much data they consume, customers tend to budget only so much for that product.

spending as a percentage of total disposal income does not change much, from year to year. To the extent that increases in purchases have happened, those boosts have been accompanied by decreases in purchase of some other product. To spend more on mobility, consumers have chosen to spend less on fixed network services, for example.

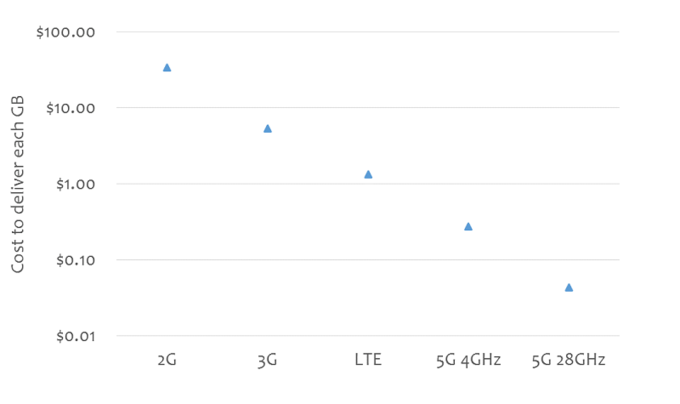

So a linear increase in cost-per-gigabyte consumed is not possible. But that is why 5G is essential: it is a way to keep supplying bandwidth at lower costs per bit, to maintain supplier profit margins.

In some cases, cheaper cost per bit also enables new use cases. That especially is true for fixed wireless use cases, where cost per bit for mobile solutions has to drop by an order of magnitude, compared to fixed alternatives.

Not so long ago, mobile data prices were so high, compared to fixed costs, that full substitution was mostly unthinkable.

That said, the trend is clear: since the 2G era, mobile bandwidth costs have fallen by more than 90 percent. In some markets, while the gap with fixed alternatives remains about an order of magnitude, that could change in the 5G era, especially where fixed wireless is possible.

That is far less true for 5G appeal in the area of enterprise use cases, where very-low-latency, edge computing and ultra-high bandwidth might enable new use cases.

This forecast developed by ABI Research for Interdigital shows as well as anything the potential revenues to be generated by 5G. Note the importance of industrial revenue, compared to consumer revenue.

In this context, “industrial” revenue includes smart cities use cases. “New types of services, especially in cities and smart cities, will likely come faster when 5G becomes a consistent connectivity and processing platform,” say ABI researchers.

“The proliferation of connected cameras and sensors around a city, in combination with 5G connectivity and edge computing, will allow for a much more comprehensive security solution deployed throughout cities,” ABI Research says. “It is almost certain that edge computing will be deployed first in cities, and coupled with 5G, it can allow for smart transport applications.”

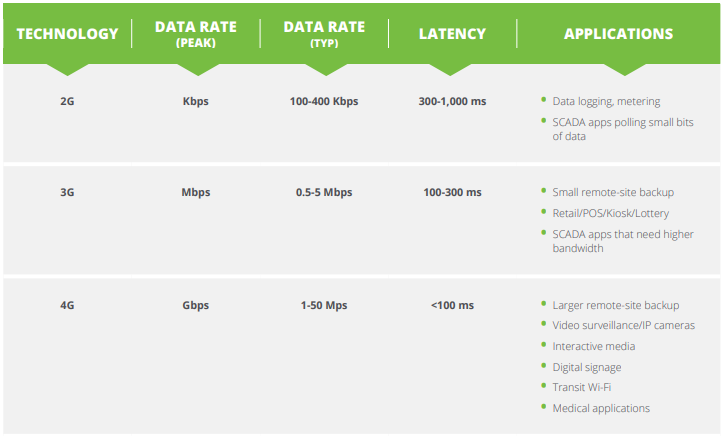

Every mobile generation since the first analog network has enabled new use cases and applications. In business markets, for example, 2G enabled what we now tend to call “internet of things” apps for monitoring industrial processed. During the 3G era use cases expanded to remote site data backups and kiosks. In the 4G era video surveillance became practical.

So the 5G focus on new use cases in the internet of things space are not misplaced. Of course, it is not simply the characteristics of the network but also cost per bit and other terms and conditions of use that help create new use cases.

In the 3G era I would not have considered using the mobile network full time as my primary internet access connection for work. Speed was too low and cost per bit too high. That changed in the 4G era, when I actually did replace a fixed connection with 4G.

To be sure, the use case was not “connect all the users in the home.” That remains to this day a fixed network solution, in large part because the main driver of demand is streaming video. But to support my own work needs, especially given the amount of mobility, 4G was a good choice.

Still, more important shifts tend to take time, at least in part because full deployment and advanced versions of the network will take some time.

But one of the nuances of 5G is that, for most consumer applications, the 4G network is going to be satisfactory, while Advanced 4G (LTE-A) is going to to support nearly every consumer 5G smartphone-based experience requirement.

So advanced 4G is going to be important as a way of maintaining continuity of experience as users bounce between 5G and 4G networks. Nobody wants to experience what used to happen in dropping from an area of 3G to an area of 2G, for example. For some of us, that same experience happened when dropping from 4G back to 3G.

There is reason to hope the switch from 5G to 4G will not be as abrupt, simply because consumer mobile app experience might not be noticeable when speed drops from 100 Mbps to 30 Mbps.

Still, gaming, virtual reality and augmented realitt seem to be the areas where some consumers might find 5G does actually provide improved experience.

For most of us, the transition to 5G will come more slowly, as the need to replace handsets results in acquisition of devices that can use 5G. In other words, for many, the new handset pulls with it the incentive and means to use 5G.

What remains to be seen is how soon that transition occurs, and when new use cases start to emerge. As a consumer smartphone user, the advantage seems less than was the case for migrating from 3G to 4G. Both 4G and advanced 4G seem more than adequate for my needs, at the moment.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...