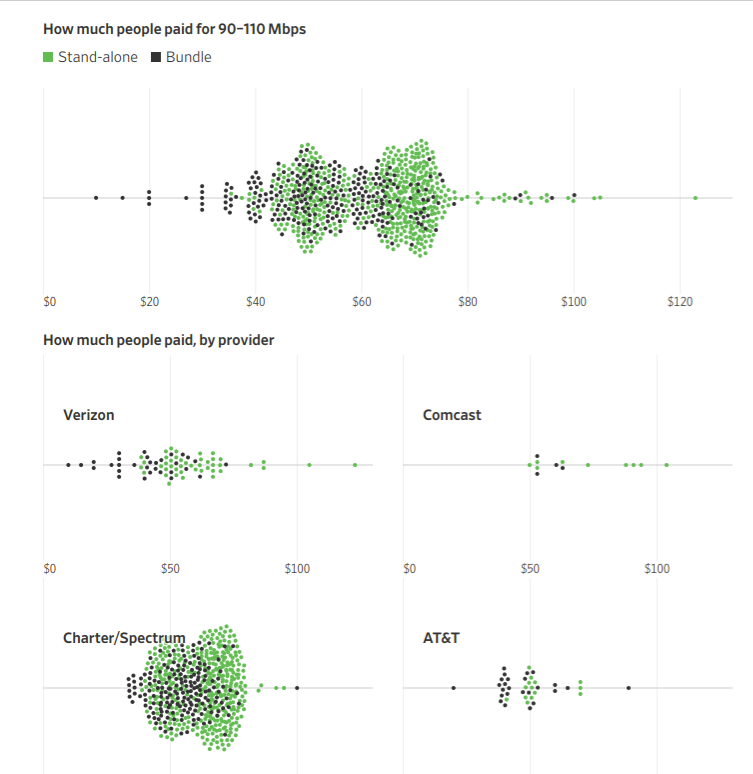

In a non-scientific study of consumer fixed network internet access bills, the Wall Street Journal found monthly bills for service at about 100 Mbps clustered between $45 a month to $70 a month. The caveat is that the sample is heavily weighted to just one internet service provider, Charter Communications, which has a heavy subscriber weighting to rural areas, in addition to some big-city systems.

Notably light in the survey were customers of Comcast’s services. Comcast is the biggest U.S. supplier of fixed network internet access connections.

I would not infer too much except where it comes to Charter customer experiences, where the typical price paid for internet access tends to run in the $45 to $80 a month range.

The Journal collected and analyzed information from more than 3,300 bills from homes in all 50 states, mostly supplied by Billshark, a company that helps customers negotiate better rates with their cable and telecommunications providers.

Among the unknowns is how customers on triple-play packages, or bill analyzers, decide to allocate a bundle’s cost across video, internet access and voice components of the bundle, as triple-play service details are not typically shown on a bill.

That means any evaluator has to make assumptions about what the “price” of each component might be. One method might be to take the posted a la carte rates for each individual service and then discount by an equal amount. Others might try and weight the prices based on some assessment of value.

Any method involves making assumptions that cannot be independently verified. Some of us would apply a near-zero (there are taxes and fees, even if the value of the service is deemed to be “nothing”) or actual zero value to voice, and then allocate total bundle price only to the internet access and video services. In principle, that could boost internet access and video prices inside a bundle by $20 to $25 per service.

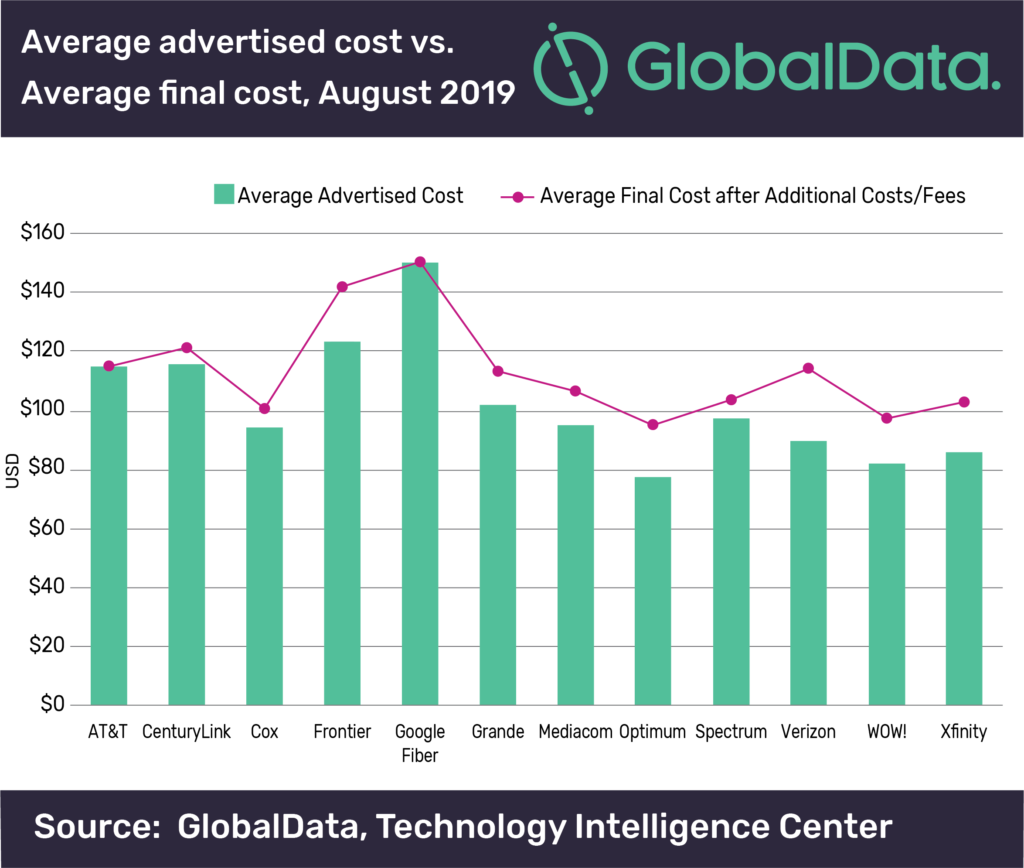

The other obvious issue is whether the analyzed or assumed prices include only the actual service, or whether equipment rentals, fees and taxes are included. Obviously, ISPs want to advertise only the lower figure; customers are likely to use the “what I pay” total, which always is higher.

“In some cases, the final cost (of a bundle) is as much as 45 percent over the advertised rate,” said Courtney Rudd, GlobalData analyst. “For example, Xfinity’s $40 ‘Starter Internet plus Basic’ TV bundle jumps to $58 per month once the additional $18 in equipment costs are added. Prices can also vary based on location.”

As has been the case in the broader telecom industry, actual prices and profit margins are, in large part, determined by the allocation of costs and overhead to various services.

Video entertainment arguably has the highest cost of goods, so I would allocate perhaps 46 percent of price in a bundle to video. Then perhaps 32 percent of price in the bundle to internet access and maybe 21 percent for voice (as accountants might tally the numbers).

Consumers buying triple play bundles might allocate near-zero value to voice, however, even if offering voice has non-zero cost to connectivity providers. That obviously would affect the perceived price of internet access and video services. So one way to tally the price is to say that even if the value of voice in a bundle is zero, it has a cost, namely the attributed fees and taxes a consumer has to pay, even when not using the voice line.

I’d estimate that cost as about three percent to five percent of the bundle price. So maybe 54 percent of the bundle price is for video, 40 percent for internet access, five percent for voice.

So that might imply a retail price of video in a triple-play bundle as about $82 a month, internet access at about $61 a month, voice at perhaps $5.