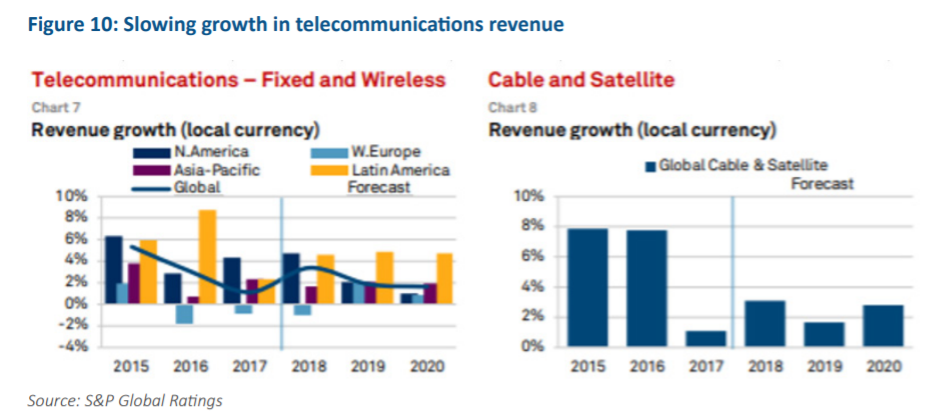

Revenue growth continues to be the big connectivity industry issue, with key markets looking at one percent to two percent annual revenue increases, according to S&P Global.

Friday, January 17, 2020

Slow Revenue Growth Remains Key Industry Problem

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, January 16, 2020

Microsoft Plans to be Carbon Negative

By 2030 Microsoft will be carbon negative, and by 2050 Microsoft will remove from the environment all the carbon the company has emitted either directly or by electrical consumption since it was founded in 1975, Microsoft says.

Microsoft aims to cut its carbon emissions by more than half by 2030, “both for our direct emissions and for our entire supply and value chain,” the firm says. “We will fund this in part by expanding our internal carbon fee, in place since 2012 and increased last year, to start charging not only our direct emissions, but those from our supply and value chains.”

It also is noteworthy that Microsoft intends to ground its efforts in “ongoing scientific advances and an accurate reliance on the basic but fundamental mathematical concepts involved.”

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

How Well is U.S. Fixed Network Business Doing?

In the U.S. market, there is a fairly clear bifurcation between fixed network connectivity providers doing relatively well, and those which are not doing so well, even if an argument can be made that the segment as a whole is challenged.

Tier-one cable operators are generating more revenue and profits from their wireline operations than most telcos are. Large tier-one telcos are doing better than smaller telcos. But AT&T fixed network revenue is slowly declining.

Verizon fixed network revenue also has been declining slowly.

The broader traditional telco market is doing less well, as revenue is dropping.

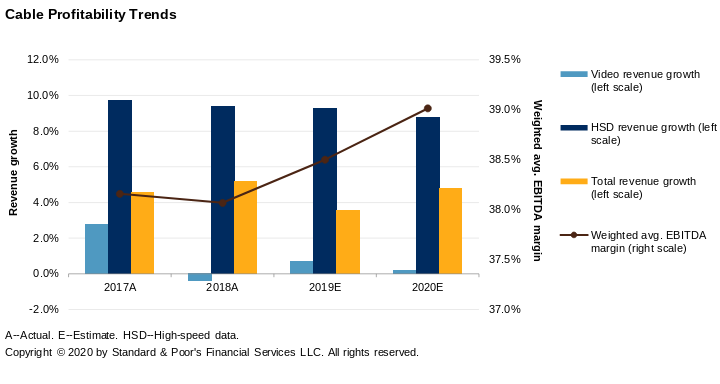

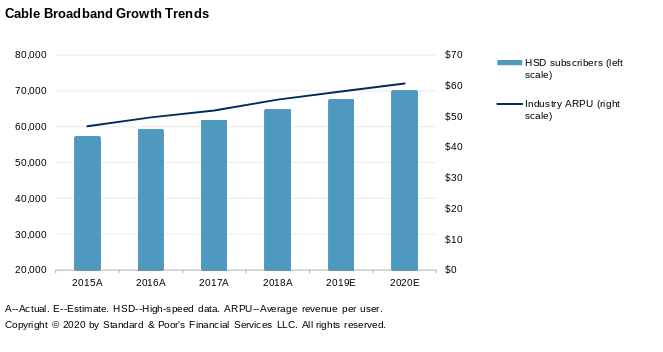

Cable internet service revenue growth arguably exceeds telco growth, which is flat to negative. And cable revenue from fixed network operations is growing. “Overall, we expect top-line growth of about five percent with weighted average margins improving by about 50 bps to approach 39 percent, S&P Global estimates.

“We believe cable companies can continue to increase high-margin broadband revenue for the next two years through a combination of subscriber growth and higher prices as subscribers demand faster internet speeds with rising data consumption,” says S&P Global. “We expect that the average number of broadband subscribers will increase by about four percent in 2020.”

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

WAN Costs Might be a Bigger Edge Computing Driver than Latency

By 2025, perhaps 75 percent of enterprise data will be generated outside enterprise data centers or cloud data centers, according to Cisco.

While today only 10 percent of all data is handled at the edge, analysts expect in three years between 50 percent and 75 percent of all data to be produced and processed at the edge,” said Paul Morgan, Global Sales for Manufacturing, Automotive & IoT, at HP Enterprise (HPE). “Gartner puts the figure at 75 percent.”

And even if latency is an issue for some edge applications, conrtainment of bandwidth costs also matters. If much of that data can be processed locally, wide area network bandwidth costs are lower.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, January 14, 2020

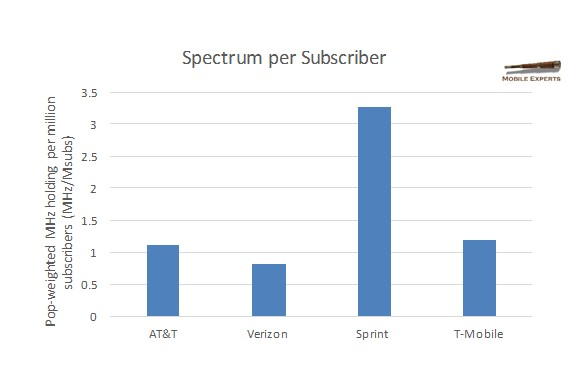

Spectrum Per Customer Matters

One always has to take marketing claims with a grain of salt. So it is with U.S. mobile operator spectrum holdings.

AT&T recently has claimed a dramatic lead in low-band spectrum. This chart shows why AT&T makes the claim.

AT&T has about 176 MHz worth of low-band and mid-band spectrum, compared to Verizon’s 117 Mhz, Sprint’s 212 Mhz, T-Mobile’s 11o MHz and Dish Network’s 92 MHz.

Of course, Verizon and AT&T have the most subscribers, so bandwidth per subscriber is less than for Sprint, T-Mobile US or Dish Network.

The “spectrum per subscriber” picture is different, though, because one also has to factor in the network load. Operators with more customers "need" more spectrum. And since Verizon and AT&T have "most of the customers," that should affect spectrum available "per customer."

Spectrum holdings matter, of course. But subscriber loading also matters. Looked at on a bandwidth per subscriber basis, AT&T, Verizon and T-Mobile US are not far apart. Only Sprint has an unusually high amount of spectrum. Dish Network has not launched yet, and will be starting with modest network loading, so it should have relatively high spectrum per customer.

Verizon has 35 percent share of subscriptions. AT&T has 34 percent market share. So those two service providers have a combined 69 percent share of market. T-Mobile US has 17.5 percent share, while Sprint has about 12 percent share, according to Statista.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

5G Subscription Forecasts Suggest Asia Will Lead

Market forecasts always are contingent on one’s assumptions, and that is no different for 5G subscription forecasts. It would take a brave leap or unusual definition to conclude anything other than that Asia will have the greatest number of 5G connections in the future, simply because Asia has the most people and the most mobile subscribers.

Juniper Research anticipates that over 75 percent of global 5G connections will be in the Far East and China. This is due to the early launches in South Korea by all tier one operators, which was followed by significant launches of commercial 5G networks in China.

GlobalData, on the other hand, suggests that Asia will account for about 65 percent of global 5G subscriptions by 2024 and about 44 percent of revenue. North America will account for 32 percent of revenue by 2024.

At the end of 2019, there were an estimated 4.5 million 5G users in the Far East, roughly 80 percent of the global total, nearly all of them in South Korea, Juniper Research estimates.

But Juniper also predicts the United States and South Korea will be the fastest adopters of 5G, with 75 percent of all 5G subscribers attributable to these two countries by the end of 2020. That does not make sense to me, but that is what Juniper says.

By 2025, Asia will still have more than 60 percent of 5G connections, Ericsson predicts.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, January 13, 2020

Is Structural Separation Still Relevant?

Australia, New Zealand and Singapore are among nations that have instituted a structurally separated telecom network environment, especially regarding the legacy national telecom networks.

Infrastructure sharing is a more common trend, as when mobile operators agree to share the cost of cell towers.

Municipal broadband networks represent a similar effort to create more competition, or higher-quality consumer services, using a wholesale approach where one entity builds and operates the network, and any number of retail providers are allowed to use the network to create their own retail efforts.

Compared to two decades ago, there seems less talk about structural separation as a method for either increasing capital investment or limiting the cost of such investment. Municipal networks, building brand new facilities, seems to be the bigger trend in some markets, such as the United States.

While it might be too early to draw final conclusions, there already is some mixed evidence of the value of such decisions. Some three decades ago, I was part of a study team looking at a proposal by Rochester Telephone Company to divest its local communications monopoly, creating a wholesale framework, in return for which RTC would be granted freedom to enter the long distance business, at that point.

Rochester Telephone won permission from state regulators to split into separate companies: a regulated wholesaler of telephone services named Rochester Telephone Corp. and an unregulated retailer named Frontier Communications of Rochester.

After approval, RTC become Frontier Corp. in 1995. In August 1995 Frontier Corp. merged with ALC Communications Corp., acquiring in that move Confer Tech International, the world's largest dedicated multimedia teleconferencing company.

Later in the year Frontier acquired LINK-VTC, a videoconferencing services company. A month earlier, Frontier had purchased Schneider Communications Inc., a long-distance voice and data carrier, and its 81 percent interest in LinkUSA Corp., a long-distance services provider, for $127 million.

Other 1995 acquisitions were WCT Communications, a West Coast long-distance company; Enhanced TeleManagement, Inc., offering integrated telecommunications services in six states; American Sharecom, Inc., a Minneapolis-based long-distance company; and Minnesota Southern Cellular Telephone Co. Frontier also established its first international subsidiary for integrated services, London-based FronTel Communications Ltd.

In 1999 the company was acquired by Global Crossing. In 2001, Global Crossing North America's local exchange assets, including Frontier Telephone of Rochester and Frontier Subsidiary Telco, and ownership of the Frontier name were sold to Citizens Communications Company, which in 2008 renamed itself Frontier Communications.

I have no idea how well the wholesale model actually has worked out in the former Rochester Telephone service area, but it is not clear to me that competition or investment has been significantly different after the structural separation.

If I had to guess I’d say the emergence of Charter Communications as a telecom services supplier has had more impact on prices and the quality of service than the structural separation.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...