It is fair enough to argue that some organizations make better use of resources than others. It follows that some connectivity providers (mobile or fixed) will perform better than others, using any chosen set of key performance indicators, on business or network performance measures.

Firms also will tend to perform differently on different KPI measures, which can be set on business outcomes or network outcomes, for example. Financial metrics might be one thing, customer satisfaction or lifetime value another matter.

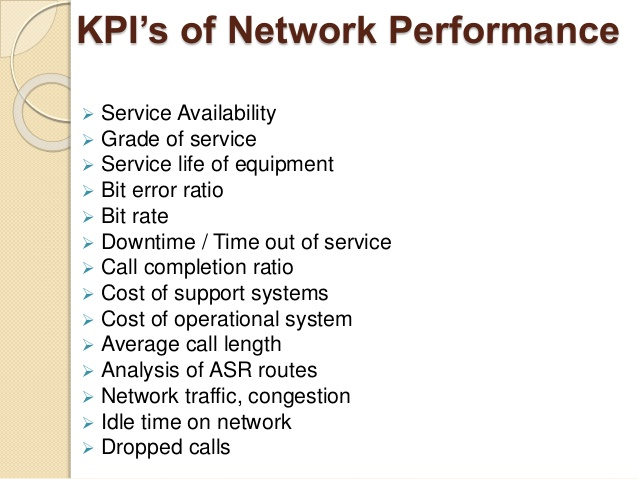

Business KPIs can include revenue per account, revenue per cell site, subscriber counts, market share, market share growth, margin per customer or account or subscriber acquisition cost, churn rates, lifetime account value, inquiry conversion rates, capital expense per account or operating cost per account, for example.

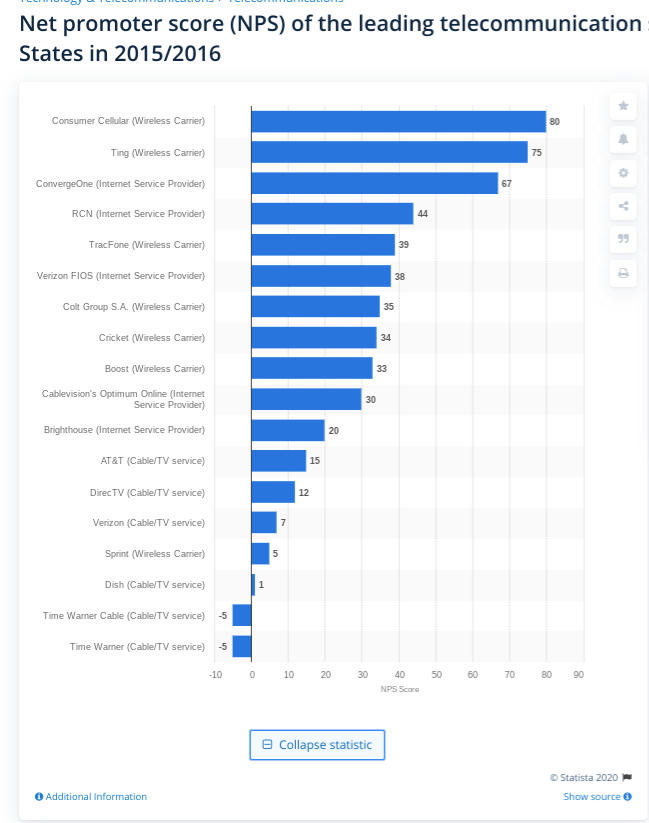

Consider the net promoter score, a measure of customer willingness to refer a company to others. Sometimes the scores are described on a scale of zero to 10, other times on a scale of -100 to +100. Either way, the NPS score tries to determine brand effectiveness at customer experience, boiled down to a willingness to recommend the product to others.

Aside from the potential word of mouth impact, NPS studies tend to find that detractors spend less, promoters spend more. That stands to reason. Any customer that is unhappy will tend to look for other substitutes. Any customer that is quite satisfied will tend to keep buying, might tend to buy more and also look more favorably upon a brand’s other products.

Having taken many such surveys, I would say the results are somewhat misleading. Normally one is asked how willing one would be to recommend a product to others, or sometimes whether one would be proud to work for a certain company, or recommend that someone else work there.

It is a brute force methodology, in many respects. I might recommend a particular product, from a particular company to some people, and not to others. Some buyers are price conscious, some are value conscious and some are brand conscious, irrespective of price.

Some products have a wide zone of tolerance--in terms of value or effectiveness--while others might require more discernment. Flour, sugar, gasoline or salt might not be products where brand matters. For a gourmet cook, spices and meats might be products where high discernment is required.

Most people likely have high preferences in fragrances, clothing, personal electronics, cosmetics, pets, transportation or housing. Most other products, though, might have high zones of indifference and high product substitutability.

I would make different recommendations to each type of buyer, so I often question the relevance of NPS rankings. Some products have very high value for segments of the population; others have relatively low value, or no value. Many products arguably have high substitution potential, simply because the products are commodities, or are items about which a particular customer has no great preferences.

“What to measure” and “what we can do with what we measure” are key issues for efforts to apply artificial intelligence to business processes and network management. Consider the discipline of AIOps, the effort to apply machine learning to network management.

Whether AIOps is about insight or automation often is unclear, especially because the stated goal of AIOps to gain insights that lead to automated action, supervised or unsupervised by humans. Ericsson, for example, talking about applied artificial intelligence in communications networks, prefers the “automation” label.

In large part, that might reflect the particular challenges of the connectivity service provider industry, where many revenue and business problems grow from unhappy customers and poor customer experience (dropped calls, no coverage, slow internet speeds, poor connection quality).

“Previous Ericsson research shows that almost 50 percent of consumer network perception is based on personal experiences of the network, indicating the huge importance of network quality as the key to customer satisfaction,” Ericsson says.

Customer satisfaction, in turn, is believed to be causally related to word of mouth referrals, prospect perceptions of quality and value, customer churn, customer acquisition and therefore revenue, profits and market share.

“Whether customers give you US$2 or $20 ARPU, if you do not provide the quality they expect, they will churn,” says Vicente Cotino Director of Network Operation Maintenance, Orange Spain.

To be sure, network performance is not the only driver of satisfaction. “At least one-third of the total NPS (net promoter score, a measure of customer willingness to recommend a product or service to others) score is derived from network performance.”

Of the service providers surveyed by Ericsson, 80 percent use NPS as a key metric in operations. Also, several service providers indicate that 40 percent to 60 percent of operations key performance indicators are business-related.

Service providers, in other words, must do many things right, beyond ensuring that the network works as it is supposed to work. What is hard to untangle is the percentage of benefit that AIOps might provide, and whether it is automating changes or detecting issues that is “more important.”

Clearly the two are related. Action is not possible without insight; nor is insight useful unless changes can be made fast.

In surveys undertaken by Ericsson, 80 percent of respondents say automation is key for the cost and customer experience. About 90 percent of operations personnel say AI is important in protecting customer experience.

As always, methodology matters. I do not know how the questions were framed. It is not clear how the responses might have been different if poll takers were asked about whether better network and consumer behavior insight and prediction would protect customer experience.

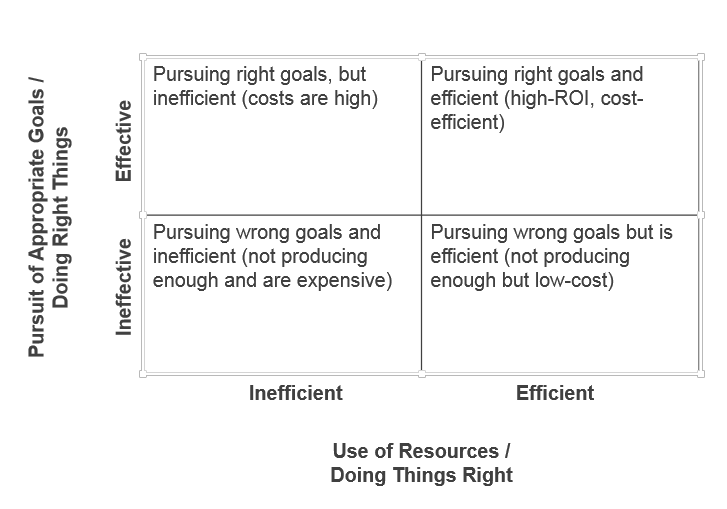

But Ericsson frames the issue as one of “automation.” That might simply be a reflection of our general confusion about effectiveness and efficiency. People often speak about the importance of efficiency, which might be expressed as getting work done faster, with fewer people, at less cost or with fewer mistakes and rework.

Less common are evaluations of effectiveness, which might be expressed as “doing the right things” to produce value or desired outcomes. A traditional way of illustrating the difference is to note that an organization gains little to nothing by automating things that should not be done.

In principle, AIOps as applied to a communications network requires automated insight to produce proactive network responses. So far, we seem to have gotten better at insight, while IT managers still debate the value of unsupervised action by AI-driven systems to correct and modify network operations.

Still, there already are instances where radio resource management, for example, is made both more effective and efficient because AI allows the network to apportion capacity where it is needed most, “right now.”

It is inevitable that human managers are going to want to start small and apply AIOps in narrow areas, gaining confidence to apply more generally. Put simply, “nobody trusts the system to behave autonomously” at the moment.