Some changes to the connectivity business model are obvious; others more subtle. The ubiquity of mobile services is obvious, as is the growth of internet access and the waning of fixed network voice and entertainment video.

But other changes happen over such long periods of time that a generation or two can live with a new reality without noticing the differences. There was, for example, a time when the internet did not exist; when PCs and mobile phones did not exist.

Less obviously, the ways mobile network capacity gets created have changed. Some of those ways reduce capital investment and operating costs.

Historically, there are three ways mobile operators have created more capacity on their networks: get new spectrum; use more spectrally-efficient technologies and move to smaller cell sizes. In the 4G era a new tool emerged: use of unlicensed spectrum to offload traffic to local networks.

Buying additional spectrum and shrinking cell sizes obviously increase capex. Shrinking cell radii 50 percent quadruples the number of cells, for example. Deploying new radios and using new modulation schemes arguably is relatively neutral as a cost driver.

Use of unlicensed spectrum, on the other hand, clearly reduces both capex and operating expense. The spectrum does not have to be bought; the radios do not have to be installed or operated; and third parties pay for energy consumption.

5G brings advances in using unlicensed spectrum, particularly in the area of allowing aggregation of available unlicensed spectrum to licensed spectrum resources.

Prior to the 4G era, it can be argued that smaller cell sizes and radio technology or modulation advances have created more usable capacity than new spectrum allocations. But widespread Wi-Fi offload has changed the toolkit. Wi-Fi offload might account for 30 percent to 40 percent of customer data consumption.

During the Covid pandemic the percentage of consumption shifted to Wi-Fi was certainly much larger than that. In the 5G and succeeding eras, the ability to aggregate unlicensed spectrum to licensed spectrum will be an important new source of effective capacity.

source: Science Direct

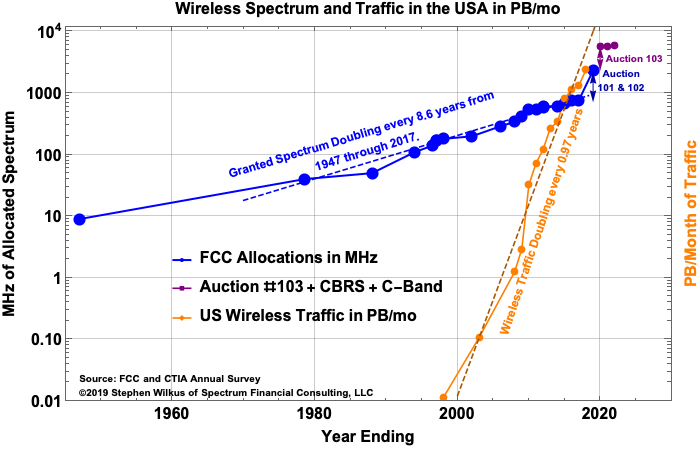

It is not yet clear how well that pattern will hold up in the 5G and coming eras. Though both network densification (smaller cells) and new spectrum resources will be applied, in addition to better radio technology and more advanced signal modulation, new spectrum allocated will be discontinuous.

From 1947 to 2017, allocated mobile spectrum doubled about every 8.6 years. The 5G auctions have broken the scale.

In large part, new spectrum allocations have been relatively small and incremental. The allocations for 5G are discontinuously larger, involving both larger amounts of spectrum per auction and also much more effective bandwidth per unit.

Simply, capacity is related to frequency. The higher the frequency, the higher the potential bandwidth.

source: Lynk

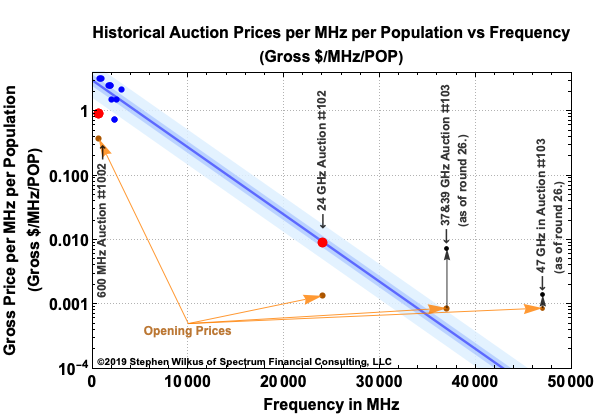

Spectrum auction behavior also shows that price per unit decreases as frequency increases, with several drivers at work. Higher-frequency spectrum simply involves more capacity per unit, but also requires more-expensive (denser) networks. So spectrum value is partly the result of expected costs to deploy networks using that spectrum

Historically, the highest prices were obtained for spectrum with good coverage capabilities, hence lower infrastructure cost. Business models also play a role. The problem mobile internet service providers face is that customers require more bandwidth every year, but are generally only willing to pay the same amount.

source: Lynk

So additional bandwidth is a cost of remaining in business, not necessarily a driver of incremental revenue. Also, relative scarcity plays a role in setting value and prices per unit. Low-band spectrum was the most scarce. Mid-band spectrum is less scarce and high-band (millimeter and above) is relatively plentiful. As always, scarcity increases prices. Abundance reduces prices.

The point is that the traditional rules of thumb about how mobile network capacity gets increased might have changed. Better modulation and radios; new spectrum allocations and smaller cells still are three ways capacity gets increased.

But use of unlicensed network capacity has become a fourth tool. Even if, historically, smaller cell sizes have driven most of the capacity increase, there will be more balanced improvements in the future, relying much more on the use of additional spectrum, licensed and unlicensed.