Lots of mobile industry executives have worried about 5G monetization. The real concern might not actually be so much whether there will lots of revenue, as there will certainly be.

The issue is more the cost side of the business model, especially capital investment to support dense backhaul networks and small cells. Even discounting new sources of revenue from network slicing, edge computing or internet of things, 5G revenue will mostly approximate 4G revenues.

Some will think that is an argument against deploying 5G. Strategically, 5G investment is necessary to keep the business a mobile service provider already has. In other words, lost market share, gross revenues and profits are at stake if the upgrade to 5G is not made.

That might seem like a paltry return, but that is the history of the mobility business. Every decade, a new next-generation network must be deployed, in large part simply to supply ever-increasing data demand and at the same time reduce the cost of supplying those bits.

Each mobile next-generation network is required as a primary means of accomplishing something else: generating new revenues to replace substantial lost revenues.

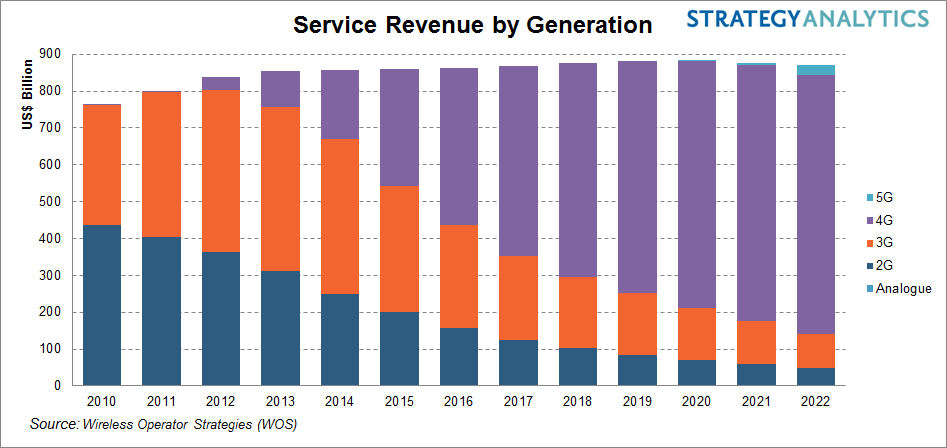

As a rule of thumb--as shocking as it might seem at first--service providers tend to replace about half of their existing revenue every decade. 5G provides one very concrete example, as did 2G, 3G and 4G.

5G accounts will eventually replace half of all other accounts--primarily 4G but also 3G and 2G--over a decade.

The same process happened for analog mobile, 2G, 3G and 4G. By design, each successive mobile next-generation network displaces the older networks. A common pattern is for the latest generation to get about 50 percent share of accounts within five to six years.

The same process arguably also held for home broadband and fixed network internet access services. As typical speeds increase over time, customers upgrade. The product we called “dial-up internet access” was replaced by “broadband” access at single-digit or low double-digit rates.

But speeds keep increasing. And customers gradually replace older services with newer services operating at higher speeds.

Access speeds in the U.S. and other markets have grown by an order of magnitude (10x) every five years, since about 1990.

So, in a real sense, both mobile and fixed network internet service providers do replace at least half of all existing revenue every decade, looking only at a single product: consumer internet access.

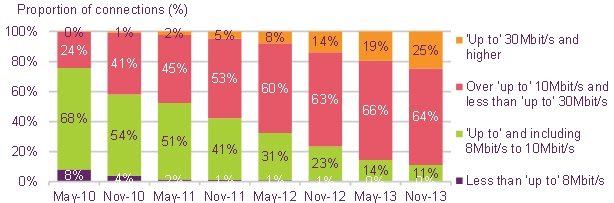

For example, about a third of U.S. home broadband customers in early 2019 bought services operating at 100 Mbps to 150 Mbps. Two years later nearly half were buying services operating between 100 Mbps and 200 Mbps.

In early 2019 some 54 percent of U.S. households purchased services operating at speeds less than 75 Mbps. By mid-2021, all customers buying services at less than 50 Mbps had fallen to 10.5 percent.

Enterprise data services show the same trend. Where enterprises once bought X.25, they later switched to ISDN, also frame relay, then to T-carrier, followed by ATM, then witching to dedicated internet access and MPLS. Now many are moving to SD-WAN.

The point is that the products enterprises purchased--and service providers sold--evolves over time. The same general pattern--replacement of half of current products--every decade also holds.

So, to answer the question about where 5G revenue will come, it will mostly come from the same places it does now. There will be new revenue sources over the decade, including fixed wireless, sensor connections and edge computing revenues. But the mainstay will remain consumer and business mobile connections.