There was a time when millimeter wave spectrum was considered too limited for widespread consumer communications, as useful as it was for point-to-point trunking and backhaul. That has changed. Now we look at where and why it is useful for enterprise, service provider and consumer use cases. That's a big change.

Sunday, October 24, 2021

Where Does Millimeter Wave Add the Greatest Value?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, October 21, 2021

5G Adoption Seeingly Follows Old Consumer Electronics Adoption Pattern

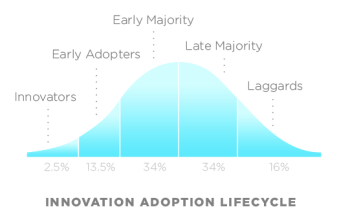

5G seems to be following a traditional consumer electronics rule of thumb, which is that adoption reaches an inflection point at about the point that 10 percent of households have bought.

According to researchers at Omdia, the important inflection point for 5G is is “the point where 5G starts being revenue positive.” Omdia says about 14 percent of 5G networks have reached that point of 10-percent subscriber penetration.

Of 150 mobile operators with at least some 5G coverage by June 30, 2021 only 21 had managed to get to a point where at least 10 percent of their subscribers had regular 5G access, according to Omdia.

The reason 10 percent seems to be the trigger, one might argue, is that it is the point where early adopters have become customers and users, setting the stage for behavior to extend to the majority of consumers.

One can see an example in cell phone adoption by U.S. households. About 1994, household adoption reached 10 percent or so, after a longer period of slow adoption. An analogous pattern happened with smartphone adoption as well.

The adoption pattern perhaps is easier to visualize with a longer time frame. Here is a chart showing cell phone adoption in the United Kingdom.

A wide range of physical products have shown the same pattern. Automobile adoption shows adoption accelerating once the 10-percent threshold was hit.

source: Our World in Data

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

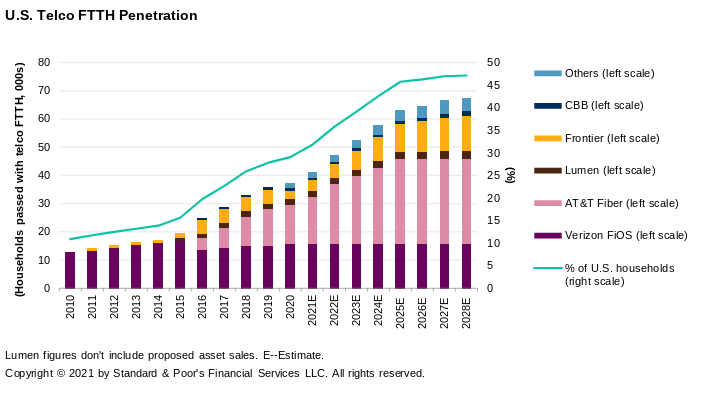

Telco FTTH Assault Will Intensify

The growing rule of thumb for telcos pondering fiber-to-home upgrades is whether the business model works, especially in a context where internet access is the mainstay of the business, and a major support for what remains of the voice business, is the take rate.

The consensus is that when take rates are about 40 percent, the FTTH upgrade is worth doing. That might also have been the case in years past, but many telcos had enough leverage (debt) that priority for available cash flow had to be debt reduction, rather than network upgrades.

Now that most telcos have deleveraged themselves, more cash flow is available for other purposes, including network investment. This is true not only for AT&T, but for other fixed network providers as well.

This is perhaps most obvious in the cases of Windstream and Frontier Communications, for example. Lumen Technologies has divested about half its largely-rural fixed network assets, though some would note this actually will reduce free cash flow, albeit allowing Lumen to concentrate on a footprint that is smaller and better suited to FTTH business cases.

The potential big change is market share possibly to be gained by AT&T. Frontier Communications arguably will be a significant potential source of net account additions as well.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Between FTTH and DSL Lies Fixed Wireless

We might all agree that telcos would prefer to build their next-generation networks on fiber to the home. We might also agree that the business case remains difficult in perhaps half of all locations.

For that reason, 5G fixed wireless has gained traction in some quarters, and might be increasingly attractive to others if fixed wireless traction is gotten.

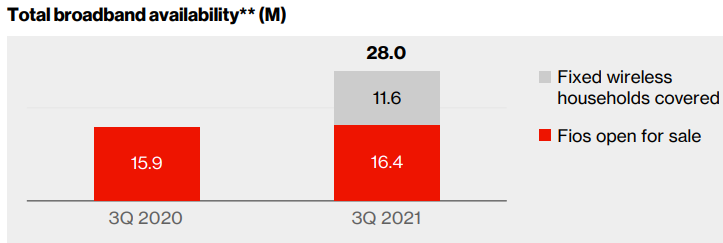

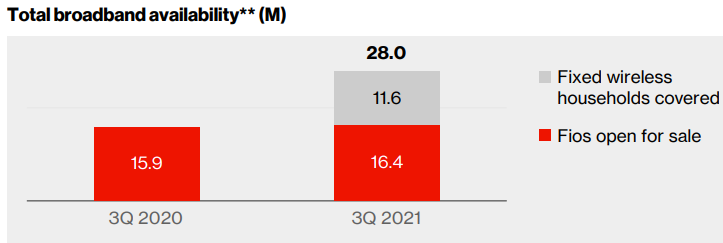

AT&T now has about 15 million homes reachable with its fiber to home facilities, with plans to expand to about 30 million locations by about 2025. All together, AT&T’s fixed network passes about 60 million locations, however.

So the business model--as presently constituted--does not seem attractive for FTTH in about half the total fixed network passings, at the moment. Whether AT&T believes fixed wireless will be important in that regard is less than certain. Up to this point, AT&T has not been as bullish on fixed wireless as Verizon or T-Mobile.

But AT&T does have national 5G assets that could underpin a wider move to fixed wireless, even if executives do not prefer that strategy at the moment.

Other major operators without 5G assets would have to rely on partner agreements before such a strategy would make sense.

Lumen Technologies has about 15 million homes in its access network footprint, 2.5 million of which are passed by the fiber-to-home network. So less than 17 percent of locations presently are deemed feasible for FTTH.

With 21 million locations served by the access network, that implies about six million business locations. Perhaps more important, Lumen now has about 97 percent of all U.S. enterprises within a five-millisecond latency range.

After partnering with T-Mobile for 5G access, Lumen argues it can span “the last 100 feet” of the access network in that manner.

One area where AT&T should be able to improve is FTTH take rates, which have been at about 35 percent of marketable locations, and might now be up to 37 percent, at the end of the third quarter 2021.

On the other hand, it appears that take rates for new FTTH accounts might in most cases--80 percent according to AT&T CEO John Stankey--be market share taken from another provider. If that continues, it is reasonable to suggest that AT&T could eventually reach 50 percent share of the installed base, up from the 30 percent or so share it has gotten over the last decade or two.

At the moment, AT&T’s rule of thumb is that unless 40 percent share is possible, new FTTH does not make sense.

Verizon and T-Mobile, on the other hand, are much more bullish on fixed wireless, for reasons related to their present revenue models. T-Mobile has had zero share of the home broadband market, so fixed wireless offers an opportunity for top-line revenue growth that by shifting just a few percent of market share could generate billions in new revenue.

Verizon now says it will pass 15 million homes with its fixed wireless services, using both 4G and 5G, while total fixed wireless accounts at the end of the third quarter 2021 were 150,000, of which 55,000 were added in the third quarter alone.

In the past Verizon has talked about a fixed wireless footprint of about 50 million homes as a planned-for goal as the C-band assets are turned up, possibly by the end of 2021.

Most of that coverage will occur in areas outside the Verizon fixed network territory. At the moment, about half the Verizon fixed wireless customers represent new accounts, while half are existing Verizon customers.

“I would say, there are probably, roughly, half and half,” said Hans Vestberg, Verizon CEO. “Half meaning coming from our existing base and half we're taking from other suppliers.”

Significantly, Verizon also reports that fixed wireless average revenue per user is “similar” to a mobility account. That suggests that most of the installed base is on 4G or lower-speed 5G at the moment, and also suggestive of pricing suggesting that most customers also use Verizon for mobility service ($40 a month for Verizon mobility customers, $60 for non-customers).

Some of us would expect ARPU to begin climbing as more of the customer base adds services using millimeter wave and mid-band spectrum. The pricing for those plans runs from $50 a month (Verizon mobility customers) up to $70 a month (non-mobile subscribers).

As will be the case for 5G generally, Verizon fixed wireless might come in three flavors. Some customers might only be able to buy 4G versions, which are the most speed-constrained, and generally topping out somewhere between 25 Mbps and 50 Mbps.

Most customers will be able to buy mid-band 5G fixed wireless, which likely will be able to support the 100 Mbps to 200 Mbps services most households buy at the moment. Some lesser percentage of locations will be able to buy the wireline-equivalent millimeter wave services operating up to a gigabit per second or so.

Over the last year, though the fiber-to-home footprint grew by 500,000 locations, the fixed wireless footprint added 11.6 million locations.

In fact, fixed wireless now accounts for about 41 percent of Verizon’s home broadband passings.

It remains to be seen how many customer accounts will be driven by fixed wireless, to be sure. In the past, many observers have suggested fixed wireless suppliers can get take rates in the 15 percent to 20 percent range.

In a saturated market, those gains largely represent market share taken from another supplier. So the market share implications are quite significant, representing a change between 30 percent to 40 percent in overall share.

The expansion of millimeter radio and C-band radio assets will be important. Roughly half the U.S. home broadband base has been content to buy service in the 100 Mbps to 200 Mbps range.

C-band will help boost fixed wireless into those ranges, while millimeter wave will enable speeds approaching the top tier of consumer demand (gigabit service).

Such lower-speed home broadband might appeal to customers content to purchase service operating at the lower ranges of bandwidths at or below 50 Mbps. That still represents 10.5 percent of the market, according to Openvault.

Notably, the third quarter 2021 earnings report was the first ever when Verizon actually began reporting fixed wireless subscriber growth. That is normally an indication that a firm believes it has an attractive story to tell, with volume growth expected.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Fixed Wireless Finally Becomes a Material Financial Matter for Verizon

Fixed wireless has been touted as a possible strategic enabler in the U.S. home broadband business, and it does now appear deployments at scale, with customer gains large enough to note on earnings calls, has begun. Verizon and T-Mobile are the leading firms to watch, as both firms have the most to gain from widespread fixed wireless deployments.

The implications for the home broadband market are highly significant. T-Mobile has had zero share of that market, while Verizon has been sharply limited by its limited footprint outside its New England and Mid-Atlantic states focus.

Since the U.S. home broadband market is nearly saturated, most account gains by any provider will come at the expense of an existing provider. That, in turn, is important because fixed wireless is one platform telcos can use to reverse a 20-year pattern of cable operators leading in installed base and market share.

In addtion to stepped-up fiber-to-home activity, fixed wireless is a primary tool that could change the U.S. home broadband installed base from a 70 percent cable lead to a more-balanced 50-50 market, with cable and telcos each eventually holding about half the installed base share.

Since home broadband now is the foundation service for any fixed network services provider, such a shift would be highly significant.

Verizon now says it will pass 15 million homes with its fixed wireless services, using both 4G and 5G, while total fixed wireless accounts at the end of the third quarter 2021 were 150,000, of which 55,000 were added in the third quarter alone.

In the past Verizon has talked about a fixed wireless footprint of about 50 million homes as a planned-for goal as the C-band assets are turned up, possibly by the end of 2021.

Most of that coverage will occur in areas outside the Verizon fixed network territory. At the moment, about half the Verizon fixed wireless customers represent new accounts, while half are existing Verizon customers.

“I would say, there are probably, roughly, half and half,” said Hans Vestberg, Verizon CEO. “Half meaning coming from our existing base and half we're taking from other suppliers.”

Significantly, Verizon also reports that fixed wireless average revenue per user is “similar” to a mobility account. That suggests that most of the installed base is on 4G or lower-speed 5G at the moment, and also suggestive of pricing suggesting that most customers also use Verizon for mobility service ($40 a month for Verizon mobility customers, $60 for non-customers).

Some of us would expect ARPU to begin climbing as more of the customer base adds services using millimeter wave and mid-band spectrum. The pricing for those plans runs from $50 a month (Verizon mobility customers) up to $70 a month (non-mobile subscribers).

As will be the case for 5G generally, Verizon fixed wireless might come in three flavors. Some customers might only be able to buy 4G versions, which are the most speed-constrained, and generally topping out somewhere between 25 Mbps and 50 Mbps.

Most customers will be able to buy mid-band 5G fixed wireless, which likely will be able to support the 100 Mbps to 200 Mbps services most households buy at the moment. Some lesser percentage of locations will be able to buy the wireline-equivalent millimeter wave services operating up to a gigabit per second or so.

Over the last year, though the fiber-to-home footprint grew by 500,000 locations, the fixed wireless footprint added 11.6 million locations.

In fact, fixed wireless now accounts for about 41 percent of Verizon’s home broadband passings.

It remains to be seen how many customer accounts will be driven by fixed wireless, to be sure. In the past, many observers have suggested fixed wireless suppliers can get take rates in the 15 percent to 20 percent range.

In a saturated market, those gains largely represent market share taken from another supplier. So the market share implications are quite significant, representing a change between 30 percent to 40 percent in overall share.

The expansion of millimeter radio and C-band radio assets will be important. Roughly half the U.S. home broadband base has been content to buy service in the 100 Mbps to 200 Mbps range.

C-band will help boost fixed wireless into those ranges, while millimeter wave will enable speeds approaching the top tier of consumer demand (gigabit service).

Such lower-speed home broadband might appeal to customers content to purchase service operating at the lower ranges of bandwidths at or below 50 Mbps. That still represents 10.5 percent of the market, according to Openvault.

Notably, the third quarter 2021 earnings report was the first ever when Verizon actually began reporting fixed wireless subscriber growth. That is normally an indication that a firm believes it has an attractive story to tell, with volume growth expected.

To my knowledge, T-Mobile has not reported its fixed wireless account figures. In light of Verizon's reporting, T-Mobile might soon have to respond.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, October 20, 2021

"Asset Light" Still Does Not Solve Big Problems in the Access Business

Many might lament that the access networks business would be a lot easier if only access networks did not cost so much.

So a reasonable and long-term argument can be made for divesting some fixed assets in the asset-heavy connectivity business, especially those that seemingly offer no business model advantages. Cell tower ownership is among those categories of things. Though essential for the mobile business, little strategic advantage can be gained from owning tower assets.

At the other end of the spectrum, ownership of scarce fixed network assets has traditionally been deemed a source of business advantage. Such assets are quite expensive to replicate, and therefore form a competitive moat against new competitors.

So business advantage, to the extent it can be created, then changes if an asset light approach is possible.

The paradox seems to be that the “asset light” approach works better for some business opportunities and entities than others. Asset light works fabulously for application providers, who then get access to potential users without the burden of investing in access networks.

The problem is that the access business itself remains stubbornly dependent on capital-intensive networks, especially in the case of “fixed” services. Mobile businesses, based simply on the number of deployed infrastructures, are inherently more asset light than cabled networks.

Of course, all that arguably changes when regulators decide to implement wholesale-based access regimes. By allowing network access, at mandated prices, to all retailers, the scarcity value of the access network is diminished, and advantage must be sought in other areas such as product packaging and marketing skill.

Since the whole purpose of competition policy is to create supplier incentives to improve product quality and quantity while reducing retail prices, we might as well recognize that lower prices in the core access business are somewhat inevitable. The corollaries are pressures on gross revenue and profit margins as well.

A competition policy that leads to higher prices, reduced quality and quantity would be deemed a failure.

All that leads to constant pressure on firm leaders to seek new ways of reducing capital investment and operating costs. And many advocate an “asset light” approach that reduces need to invest in physical networks.

In practice, that has meant reliance on one wholesale network and retail competition all using the single network. The mobile virtual network operator business strategy likewise is built on leased access to existing networks.

One might say this is akin to the “fabless” approach to the microchip businesses, where an entity designs a chipset, but then outsources its manufacturing to a third party. In that analogy, high value is earned by embedded intellectual property.

The issue for access providers is that it is quite hard to create similar embedded value if relying on a wholesale access and asset-light approach. By definition, differentiation is hard to achieve when every competitor uses the same network, with the same capabilities, at common prices.

So the “secret sauce,” to the extent it can be created, has to rest elsewhere. The search for enduring value “elsewhere” explains much access provider activity.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Fixed Wireless Becomes a Big Deal for Verizon in Just One Year

Fixed wireless has become a hugely-important means for Verizon to expand its home broadband footprint. Over the last year, though the fiber to home footprint grew by 500,000 locations, the fixed wireless footprint added 11.6 million locations.

In fact, fixed wireless now accounts for about 41 percent of Verizon’s home broadband passings.

It remains to be seen how many customer accounts will be driven by fixed wireless, to be sure. But that big an increase in footprint--mostly outside its fixed network footprint--in just a year is significant.

Unless the marketing bundle and packaging are completely inept (and that does not seem the case), Verizon is going to start gaining market share in its fixed wireless areas. In the past, many observers have suggested fixed wireless suppliers can get take rates in the 15 percent to 20 percent range.

In a saturated market, those gains largely represent market share taken from another supplier. So the market share implications are quite significant, representing a change between 30 percent to 40 percent in overall share.

The expansion of millimeter radio and C-band radio assets will be important. Roughly half the U.S. home broadband base has been content to buy service in the 100 Mbps to 200 Mbps range. C-band will help boost fixed wireless into those ranges, while millimeter wave will enable speeds approaching the top tier of consumer demand (gigabit service).

Even where not yet available, services using 4G can support access at speeds between 25 Mbps and 50 Mbps.

Such lower-speed home broadband might appeal to customers content to purchase service operating at the lower ranges of bandwidths at or below 50 Mbps. That still represents 10.5 percent of the market, according to Openvault.

Combined with marketing by T-Mobile, we are going to get a good test of fixed wireless as a major platform for home broadband services in the U.S. market.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

Is Code the Enterprise AI Killer App?

Is code generation the first “killer app” for language models or mostly the killer app for enterprise users? Since 2024, one might argue, m...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...