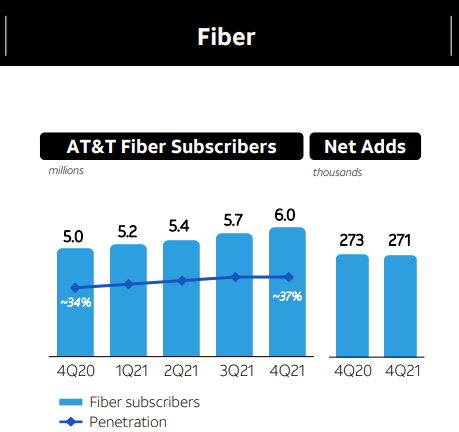

AT&T added a million fiber-to-home fiber-to-home accounts in 2021, the fourth consecutive year the firm has done so. AT&T says it boosted broadband revenues up 5.4 percent with average revenue per user growth of 4.2 percent.

Consumer fixed network revenue climbed 1.4 percent, adding $3.2 billion in additional revenue.

To be sure, AT&T still makes most of its revenue from mobility services. In the fourth quarter of 2021, AT&T earned $41 billion in revenue. Mobility represented $21 billion of quarterly revenue, or about 51 percent of total.

Business fixed network revenues were $5.9 billion, or 14 percent of total.

Consumer fixed network revenue was $3.2 billion, or about eight percent of total revenue.

Warner Media generated $9.9 billion, or 24 percent of revenue. Latin America contributed about $1 billion in revenue, or two percent of total.

Direct business and consumer revenues driven by access and other fixed network services amount to about 22 percent of AT&T revenues, compared to mobility at about 51 percent of total.

Just how much revenue contribution overall hinges on the AT&T optical fiber network is a matter of some interpretation. To the extent that the optical fiber distribution networks supports the small cell mobile network, which will grow in importance over time, the value of optical fiber investments is more than what is shown by direct business and consumer service revenue.

Indirectly, the FTTH investments also support the Warner Media streaming content business.

Still, to the extent the fixed network now supports the key mobile business, plus supporting the business and consumer fixed network business, the relative revenue contribution from FTTH arguably understates the strategic value of those investments.

Perhaps consumer FTTH, by itself, does not double consumer segment revenues. But investments in consumer FTTH also support the small, medium and enterprise portions of the business market, plus underpinning the small cell mobile network that will be increasingly important going forward.

Still, the argument can be made that the fixed network retail business hinges on home broadband. To have a business at all--simply to “keep the business”--AT&T and other telcos have to shift to FTTH.

In its competitive battle for home broadband customers, AT&T’s fortunes depend on three key drivers: fiber to home coverage; take rates and any average revenue per account gains that could supply, with the primary variable being coverage.

The reason is simply that AT&T cannot challenge dominant cable TV providers for installed base and market share until the company has much-greater FTTH coverage. Simply put, AT&T and most other local exchange carriers cover too few homes to go head to head with cable home broadband.

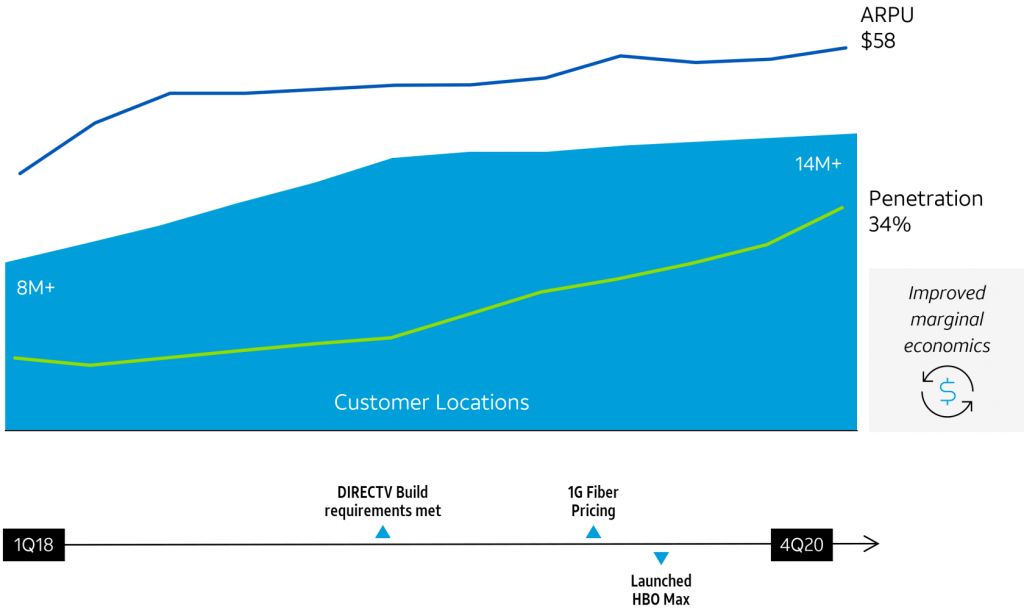

To be sure, AT&T and other telcos are pushing FTTH deployments at an accelerated pace. AT&T expects to have 30 million home locations passed by FTTH by about 2025, up from about 15 million to 15.5 million at the moment.

Keep in mind that AT&T passes a total of about 57 million homes. So the company’s current FTTH coverage is between 26 percent and 27 percent of its total passings.

AT&T will not be able to go head to head with cable, across the full range of home broadband speeds, until it has FTTH available to most homes in its fixed network footprint. By 2025, when AT&T expects to have 30 million FTTH passings, it will be able to compete head to head in about 45 percent of its footprint.

Take rates are arguably the second most-important variable, as there is a difference between an active account and a location able to buy. Over the past year, AT&T has boosted its FTTH take rate from 34 percent of passings up to 37 percent of passings.

The goal is to approach 50 percent take rates, which would exceed the general take rate of about 40 percent telcos have been able to garner over the past couple of decades.

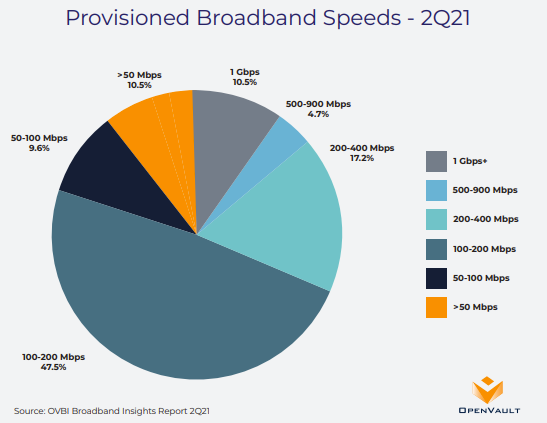

Finally, it remains to be seen how average revenue per account changes as more customers take FTTH home broadband services. At the moment, AT&T’s bottom tier FTTH home broadband service (exclusive of taxes) runs about $55 per month. The mid-range tier costs about $65 a month, while the top gigabit tier sells for $80 a month.

In addition, AT&T has added two premium tiers offering 2-Gbps symmetrical and 5-Gbps symmetrical access for $110 and $225 per month, respectively. The mix of accounts could strongly affect AT&T revenues.

The lowest FTTH tier--offering 300 Mbps--covers more than half of the U.S. home broadband buyer base. Another 17 percent of customers buy services operating between 200 Mbps and 400 Mbps.

Assuming lower-income households take advantage of support programs, those households reached by AT&T could have internet access at 300 Mbps for about $25 a month.

That is why the pace of FTTH upgrades matters so much for AT&T. To reach parity with cable TV operators, which AT&T defines as market share greater than 50 percent and installed base approaching 50 percent. Without nearly-ubiquitous FTTH deployment, those goals are likely unreachable.

To be sure, competition at the lower speed levels--up to about 100 Mbps, is an opportunity for Verizon and T-Mobile. Verizon has a limited fixed network footprint of U.S. homes while T-Mobile has had zero share of the home broadband market.

Even if those two firms use fixed wireless to reach the lower and middle tiers of buyers, that is about 65 percent to 70 percent of today’s home broadband market.

For AT&T and other telcos, though, the pace of FTTH deployment will be the story.