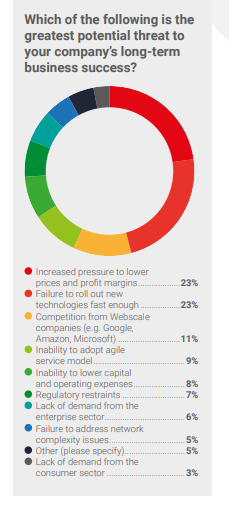

In most industries, “ruinous” levels of competition often are said to represent a “race to zero” in terms of retail pricing, with negative implications for firm or industry sustainability.

But AWS has chosen such a strategy deliberately. AWS rationally has decided to keep cutting prices as the foundation of its business model.

“How can that be?” is a reasonable question for any outside observer. How can a market leader in cloud computing literally price its core services at nearly zero, in either consumer (free computing, free storage, free apps) or business markets (cloud computing, storage, apps or platform)?

After all, big data centers and the software, hardware, real estate and energy required to run them are substantial.

The business advantages of huge scale are part of the answer. Firms such as Amazon and Google count on the fact that only a few providers, with enormous scale, can afford to compete in such a market.

So gaining scale, then lowering prices, feeds a virtuous cycle where additional customers, buying more services, allow the supplier to gain even more scale and drop prices even more, attracting yet more customers.

With sufficient scale, “scope” also becomes relevant: AWS and other leading cloud computing suppliers can sell additional services and features to the customers they already have aggregated.

So even if a “race to zero” has generally been considered dangerous and unsustainable in big existing markets, it is the foundation of strategy in many new digital--and some emerging physical markets--as well.

It is hard to compete with a competitor that gives away what you sell. That, in fact, is precisely the logic often driving business strategy in the Internet realm.

That strategy is at work with voice over IP, instant messaging, online streaming video and audio, Internet access, search and most “print” content. Many would agree, but note that these all are non-tangible, digital products. That notion is correct.

In most “physical product” areas, the Internet has lead to reduced prices, or less friction, but surely not to “near zero” levels.

That, of course, is not really the issue. The issue is a competitor’s ability to destroy enough gross revenue--and strategically, profit margin--as to break the market leader’s business model.

This is a rational strategy for some new contestants because they actually have other revenue models that are enhanced when an existing supporting market is “destroyed.”

In a real sense, Apple gains business advantage when content prices are very low. That helps it sell devices enabling content consumption. Facebook and Google gain when each additional Internet user is added, since they make money on advertising.

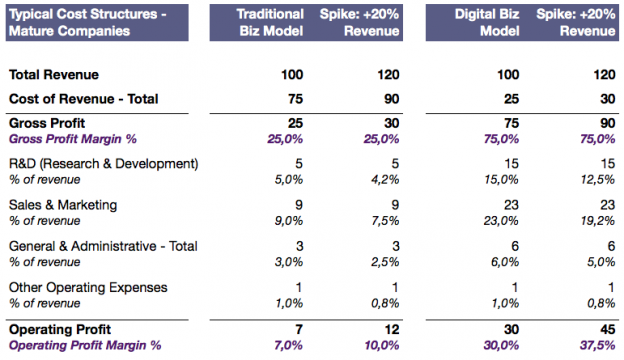

Prices for physical good distribution do not have to reach “near zero,” only “near zero profit,” for whole markets to be disrupted.

An attacker able to create a positive and sustainable business case in a market that is perhaps smaller (in terms of overall revenue) still wins is the attacker emerges as a market leader in the reshaped market.

One example: many observers would say that the chief revenue stream for Costco, the discount groceries retailer, is membership fees, not groceries. Likewise, the business model for most movie theaters is concessions, not admission tickets.

That is one sense of the term “zero billion dollar market.”

The strategy is inherent in business models used by many leading application, device or service providers.

The difference is that the trend is extending beyond businesses that are inherently “digital.” Some see shared vehicle businesses as disrupting the automobile market on a permanent basis. Shared accommodations businesses have potential to disrupt the commercial lodging business.

Without a doubt, we will see spreading efforts to replicate such sharing models in most parts of the economy where ownership is the dominant retail model.

Suppliers of cloud computing, especially infrastructure as a service (IAAS) but even the biggests segment--software as a service--also must directly confront pricing strategies that deliberately aim to reach near-zero levels.

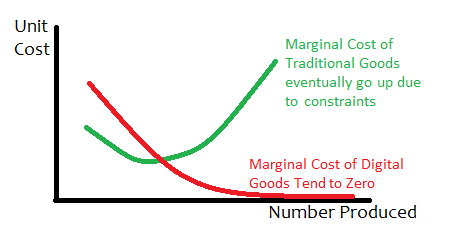

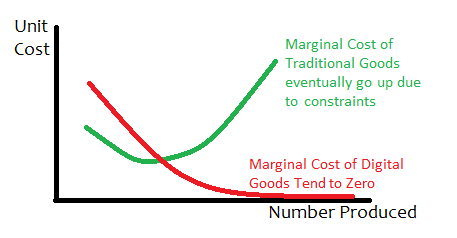

There are several analogies you might might apply, to Moore’s Law, marginal cost pricing or experience curves, for example. Some might say that same logic is embedded in much of the economics of the Internet as well.

The notion is that, over time, performance vastly improves while retail price either remains the same or also shrinks, not just on a per-bit or per-instance basis, but absolutely, adjusted for inflation or not.

Suppliers of network bandwidth and computer chips long have had to create or recraft businesses built on such assumptions.

The obvious business implications are stark. Many firms, in a growing range of industries, face competitors who literally base their business models on marginal cost pricing, near zero pricing or actual “free” prices.

Those competitors can do so because widespread use of the “near zero” or “zero” price function allows them to make money indirectly. For Amazon, the other way is retailing all manner of products. For Google and Facebook the other way is advertising. For Apple the other way is device sales.

In all those cases, the direct revenue contribution for one input--while important--is less important than ubiquity or huge scale as it relates to the primary revenue model.

“Zero” levels of pricing are a fundamental reality in a growing range of industries. How successfully the legacy providers can adapt always is the issue. In many cases, the answer is “we won’t be able to do so.”

Some would say that is an example of creative destruction. But it is destruction, nevertheless.