About 2.5 percent of U.K. household spending each month goes to purchases of communication services, Ofcom, the U.K. communications regulator, says. Of that spending, nearly two percent is for mobile services, with combined fixed network voice and Internet access accounting for about a half percent of monthly spending.

That suggests total communication spending is less than 2.5 percent of household income, and could be as low as one percent of household income.

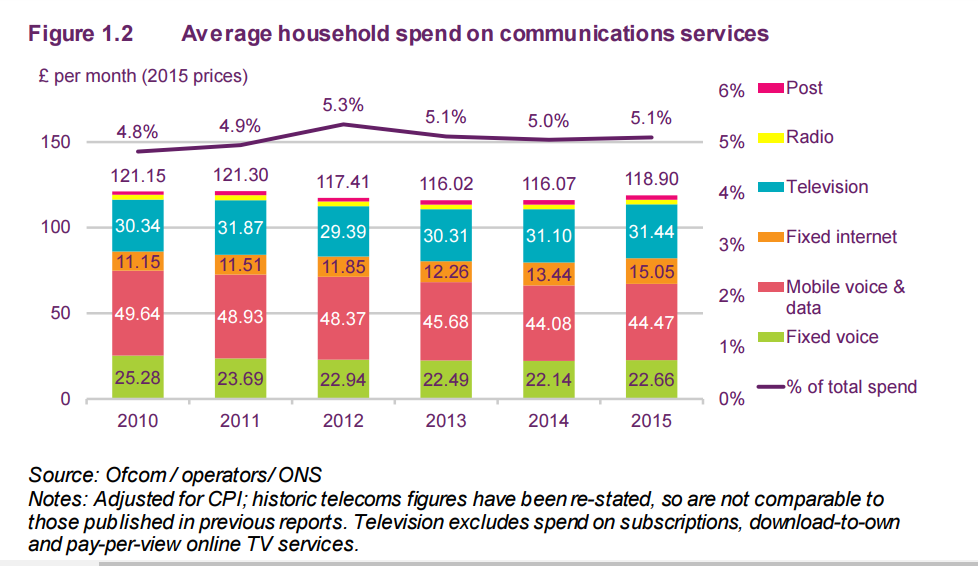

Since 2010, spending on fixed voice and mobility services have dipped slightly, while spending on Internet access has grown.

Average monthly household spend on communication services has decreased in real terms over the past five years (adjusted for inflation), Ofcom says, from £121.15 in 2010 to £118.90 in 2015, representing a monthly decrease of £2.25, or £27 per year.

At the same time, the average U.K. fixed broadband connection speed has climbed from 6.2 Mbps to 28.9 Mbps from 2010 to 2015, an order of magnitude increase.

However, monthly household spend rose between 2014 and 2015, with telecoms spending rising £2.52 per month, driven by a 12% increase in fixed internet spending: from £13.44 to £15.05 in 2015.

This is largely a result of consumers switching to faster high speed access services.

There also has been a steep increase in the proportion of adults going online on a mobile phone: with 66 percent of users 16 or older saying they used their mobile phone in 2016 to access the internet, up from 61 percent in 2015.

But U.K. mobile users increasingly are shifting their messaging activity to Instant messaging (IM), and away from text messaging.

The proportion of people using IM services such as WhatsApp is up from 28 percent to 43 percent, and photo or video messaging (MMS) has risen to more than 20 percent of adults in a given week. Both SMS text messaging and email use are dropping.

Still, 70 percent of mobile users use email every week, while 63 percent use text messaging.