It is hard to make good long-term decisions when industries are changing in fundamental ways, and that could be an issue for the U.S. mobile industry, which is expected to change quite a lot over the next decade.

One reason for believing that any merger of Sprint and T-Mobile US would lead to less competition is that this is precisely what equity analysts say are the advantages of such a merger: it would lead to less competition.

To be sure, there is an argument to be made (and will be made by Sprint and T-Mobile US if such a merger is attempted) that the combination would create a stronger competitor to AT&T and Verizon, which likely is quite true. But “stronger” for what purpose is a reasonable question.

It might be reasonable to argue that Sprint is in danger of business failure, or to argue that T-Mobile US might be able to grow itself enough organically to become a stronger competitor, but would get there right away by merging with Sprint.

But no equity analyst seems to make the argument that a Sprint merger with T-Mobile US will increase competition. They all seem to argue such a merger will lessen competition, and lead to higher prices.

That might be considered a good thing if what one wants is sustainable levels of competition beyond a duopoly. Three nearly evenly sized competitors might mean more competition is possible, long term, since that new firm would have greater scale and financial resources to compete with AT&T and Verizon.

Beyond that, the structure of the market might also be changing. With Charter Communications and Comcast entering the market, and others with niche business plans (internet of things networks using unlicensed spectrum; possibly app providers with e-commerce or advertising models), it is not clear that even three or four traditional mobile operators are the only contenders.

At least in principle, one can envision a market that blurs significantly, becoming more porous and harder to define. If Comcast and Charter cooperate, effectively operating as one national firm, it remains possible that no matter what happens, there will still be four or more leading national operators.

In fact, some would argue that already is happening, with the “mobile ecosystem” already changing, with new competition coming from the device supplier and app supplier parts of the value chain.

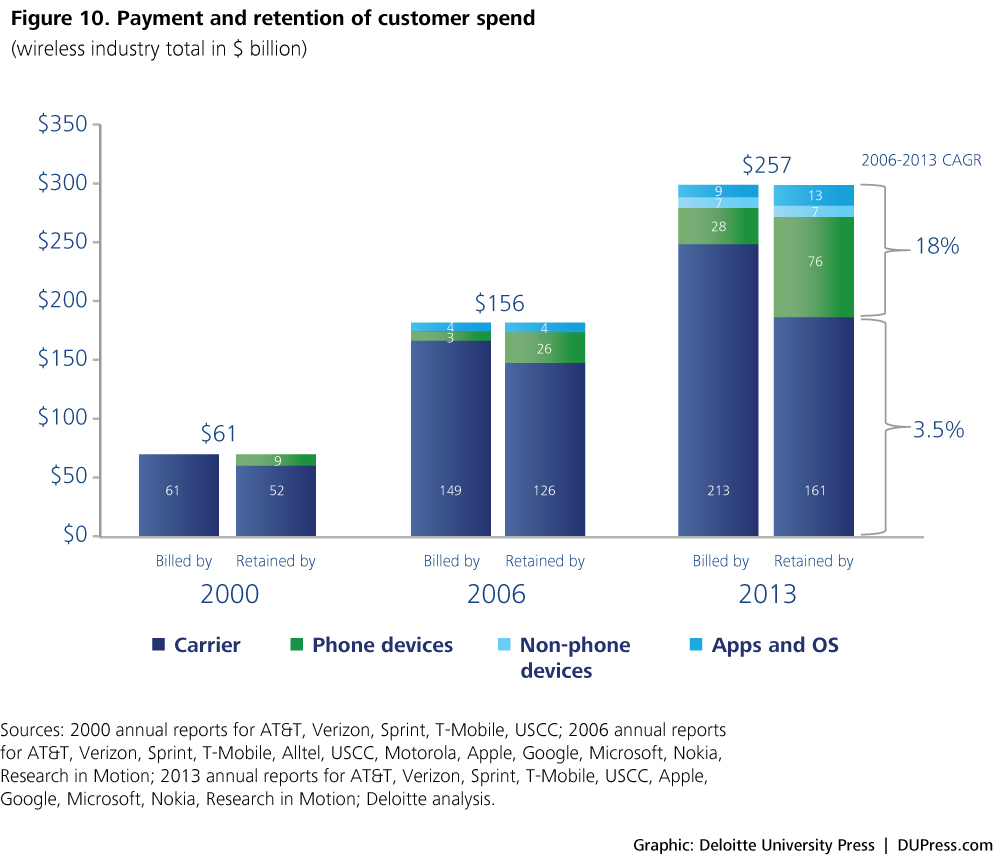

That is what Deloitte consultants now argue. In the mobile industry, handset and other ecosystem players are capturing an increasing share of revenue.

App providers also are effectively removing demand from the wide area data transport business, and operating their own captive networks. At the same time, value is migrating up to the app layer of the business.

And, in some cases, app providers are entering the access and device businesses as direct providers.

As a result, though total mobile ecosystem revenue is growing, more of the revenues now accrue to app and device partners, not access providers. Where in 2000 U.S. mobile operators might have retained about 85 percent of billed revenues, by 2013 access providers were retaining only about 63 percent of billed revenues.

Where we will be in a decade is not so clear.