Access services are a mature market in developed countries, and eventually will become mature even in developing markets, even as new revenue sources are created to replace declining legacy services. That has business consequences.

Most large tier-one service providers (cable, telco, satellite) eventually grow more by acquisition than organic growth. That is not the pattern for smaller firms, but you get the point. In any “mature” market, where accounts are essentially saturated, any provider tends to get account growth mainly by taking an account away from another existing provider.

So supplier consolidation is a long-term process in the global telecom industry. The only question is how fast, and how intense, that process is at any moment in time.

But what sorts of acquisitions make sense? The easy answer has been to make “horizontal” acquisitions to gain scale in the existing business. In other words, acquire more access assets.

That is the thinking when analysts float trial balloons such as Comcast buying Verizon, or Verizon buying Comcast or Charter, or when smaller telcos do the same sort of thing.

At least in the near term, doing so is a faster, surer way to boost gross revenue, and boost profit margins, than investing in “long game” moves “up the stack.”

To be sure, in the near term, such horizontal acquisitions are likely to be the main trend in the global telecom industry (in terms of revenue accretion). Moving up the stack takes time, and might often contribute less incremental revenue than a simple horizontal acquisition.

But taking the “long game” route to moving up the stack is possible.

Consider Comcast, which is among the U.S. access providers with the best execution “moving up the stack.” In the first quarter of 2017, Comcast booked $20.5 billion in total revenue. The access part of the company booked $12,9 billion in revenue, while the NBCUniversal portion of the company generated $7.9 billion in revenue.

So the “up the stack” (content) part of the company represented about 39 percent of revenue, access about 61 percent of total revenue.

If any other major telco could claim it now earns 39 percent of revenue from “application layer” sources, it would be considered a major strategic success.

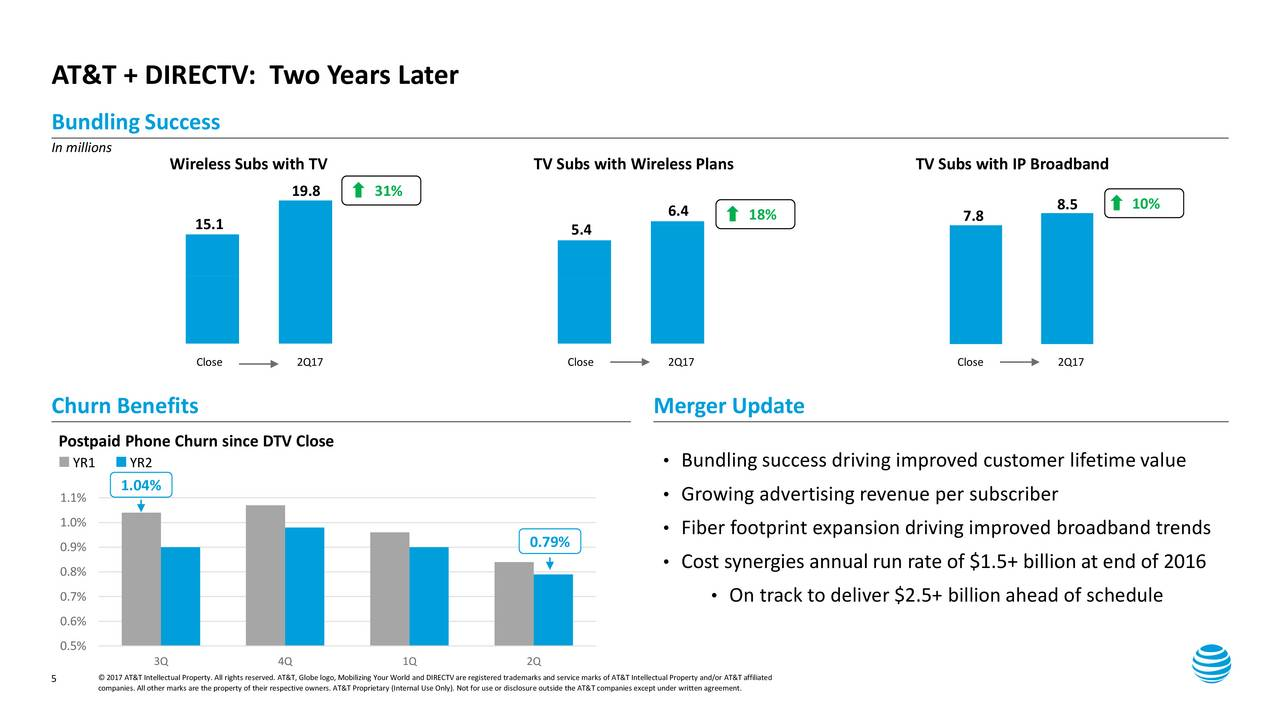

In the second quarter of 2017, AT&T earned virtually all its $39.8 billion in quarterly revenue from access services. That will change, assuming AT&T’s acquisition of Time Warner is approved.

In the first quarter of 2017, Time Warner booked $7.7 billion in revenue. In other words, after the acquisition, AT&T would earn just about as much as did Comcast in its most-recent quarter. That would boost content revenue at AT&T to about 16 percent of total.

It might not seem like much, but that would mean AT&T earns significant revenue, for the first time, from “up the stack” sources. AT&T of course will eventually want to do the same in enterprise and business areas related to internet of things, for example. But that will take time, both because the IoT market is nascent, and because the available acquisition targets therefore also are small.

Verizon has made a similar, if smaller move, by acquiring first AOL and then Yahoo, to create a new advertising business. In the first quarter of 2017, Verizon booked $29.8 billion in revenue. Revenue from its telematics unit was negligible as a percent of total, while, revenues from the “Oath” unit were not disclosed. The point is that Verizon has not yet gotten to a point where “up the stack” revenues are significant.

But you see the point. Moving up the stack is hard, risky and often not able to move the revenue needle quickly. So the an emphasis on horizontal acquisitions is going to be hard to resist. But if you believe the access business is going to be fundamentally challenged, moves to gain scale in businesses “up the stack” is necessary.

The issue is, how to balance horizontal acquisition that boosts revenue and profit now, with investments in “up the stack” growth. Or, in an ideal scenario, can access providers move up the stack now, by acquiring assets that throw off enough significant current cash flow, to move the revenue needle immediately?

Comcast is the model for the U.S. market.

That illustrates an asymmetry for Comcast and Verizon, if you wantt to speculate on where value might lie, even if the odds of such an event are slim.

Comcast might value Verizon’s mobile assets, significantly growing the amount of its access revenues. But if you think a reliance on access revenues, going forward, is problematic, then Verizon gains more in any acquisition of Comcast, as it immediately gains “up the stack” assets, in addition to greater horizontal scale.

That is why some observers might argue that vertical acquisitions, where the synergy is clear, make more sense than horizontal acquisitions that increase scale in the access business.

Some will argue AT&T erred in buying Time Warner. Some of us would argue it is the right move, to move up the stack, when total revenue includes almost no “up the stack” contributions. If Verizon remains a buyer of assets, not a seller, “up the stack” makes more sense than a horizontal acquisition that simply adds more scale in access.

Some would focus on strategic angles, such as a faster path to “fiber deep” or “bandwidth deep” assets.

Others of us might argue that firms such as Verizon and AT&T, if they wish to remain leaders in the future (and not sell themselves), must create much more “up the stack” revenue. It is the only way to reposition their value in the ecosystem and escape a “dumb pipe,” low value, low margin existence.