It is highly unusual and rare for any “telco-owned” over the top service to compare well with other application provider offers of the same type. Think about telco-owned messaging, voice or mobile app platforms and you get the point.

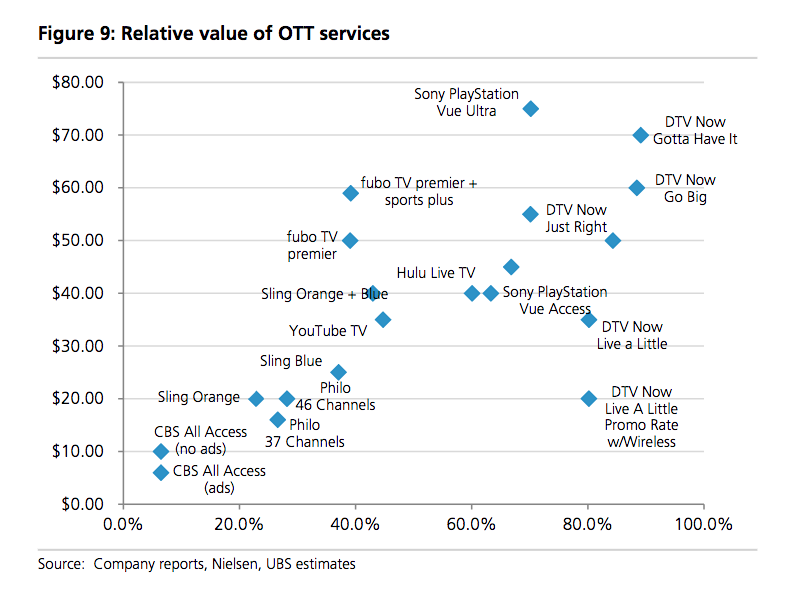

Unusually, then, AT&T’s “DirecTV Now” service gets top marks from analysts at UBS evaluating the value of current over the top “live” video services, which lead in “value’ rankings at numerous price points from $20 a month up to $70 a month.

The UBS analysis did not look at the full on-demand services such as Netflix, but only the services offering “live TV.” Some believe the OTT “live streaming” services eventually will develop as an important segment within the overall streaming market that includes “on demand” services such as Netflix that specialize in pre-recorded content, rather than “live” or “real-time” TV.

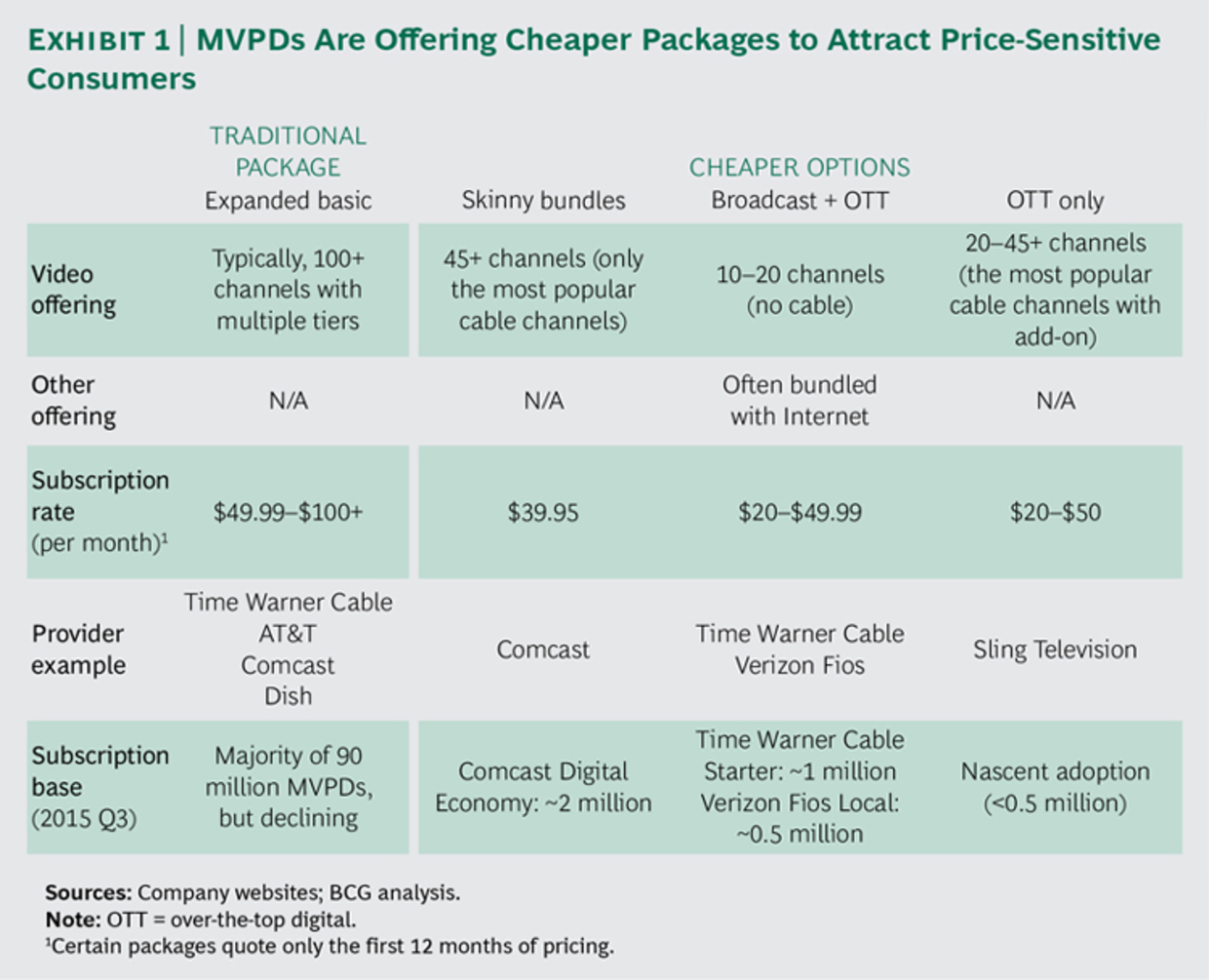

At the moment, the notion of “skinny bundles” captures the idea behind OTT live TV streaming. The idea is that there remains significant demand for “live TV” (linear channels). But there is less appetite for larger, more-expensive live TV bundles.

In many cases, on-demand services such as Netflix are complementary, as Netflix does not support or offer live TV. In essence, OTT live TV streaming captures demand that remains for over the air TV broadcasting, sports, news, events and other scheduled TV series consumption.

The point here is that a tier-one telco seems to be creating OTT live TV services that have appeal at multiple price points, and might even be deemed competitive with other similar services. If that translates into significant market share growth, it will represent a major victory for at least one telco in the effort to fashion OTT apps and services that do have mass appeal and significant market share.

That has not happened in the internet era. DirecTV Now might be among the first examples of an access provider actually creating a new mass market app that gains significant share. To be sure, some will say DirecTV Now mostly cannibalizes AT&T's own DirecTV service. Time will tell.