The million accounts AT&T has gotten in just about a year’s time suggest that AT&T might--in this case--have found a way to compete in a mass market over-the-top market that has eluded it and most other tier-one telcos in the voice, messaging and other markets.

That is a not-insignificant achievement.

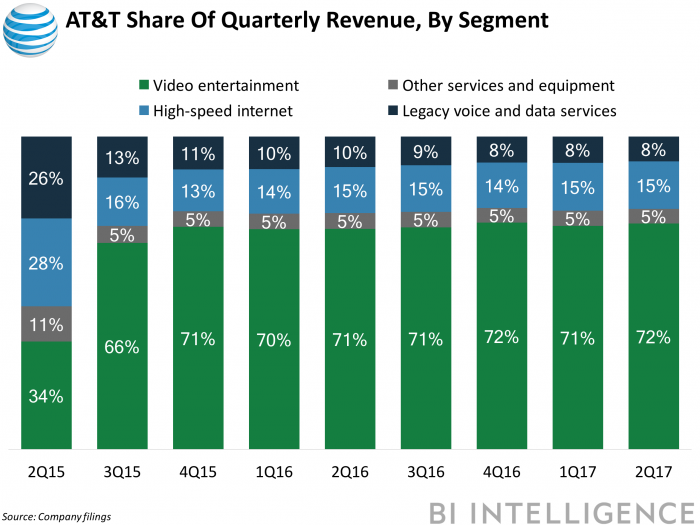

Some might say that is the second of two big achievements AT&T has pulled off recently. The first was the DirecTV purchase itself, which radically transformed AT&T’s revenue sources. The entertainment group, which includes consumer video and internet access revenues, now is a key reporting segment for AT&T, along with business solutions and consumer mobility.

“If you look at what we're getting in our DTV Now customer base now, about 50 percent comes from cord shavers and cord-nevers and 50 percent come from our competitors,” said John Stephenson, AT&T CFO.

Cord shavers are customers who reduce their levels of service; cord-nevers are people who never have purchased a linear TV service (generally younger people). Presumably the “cord shavers” include former DirecTV customers have switched to DirecTV Now.

Presumably, “competitors” refers to other OTT linear services (Hulu, for example).

The other interesting angle is that the OTT business model might turn out to be better than the linear model it replaces, even with the possible disparities in revenue per account. Stephenson notes that activating a DirecTV Now account “requires virtually no capex, because we don't have to send a truck, pull up the ladder climbing the ladder and put on a satellite dish on the side of your house.”

One other advantage is the elimination of the need for decoders and any inside wiring (jumper cables, for example).

Also, since linear accounts are postpaid, there is some bad debt exposure. DirecTV Now is prepaid, which eliminates the bad debt exposure.