Internet pioneer Vint Cerf talks about where the internet might be going.

Tuesday, February 13, 2018

Vint Cerf on Where the Internet is Going

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Are We in the Pipe Business? If Not, What?

Dean Bubley, Founder, Disruptive Analysis, and Connie Wightman, CEO and Chairman of Interserra Consulting Group, interviewed by Gary Kim, trying to think seriously about the future. Sources of value, roles and functions, prices trending to zero and other hairy challenges.

Part of the problem is that customers "want as little as possible, and don't want to pay for it," said Bubley.

Part of the problem is that customers "want as little as possible, and don't want to pay for it," said Bubley.

“Voice mail is irrelevant,” says Wightman. “I don’t think telecom is a separate sector, anymore.” And eventually, app interfaces will be as ubiquitous as electrical outlets.”

“There are many more blurred boundaries,” says Bubley. “That makes it hard to classify things with a bright line.” Basically, the old monopoly on creating “telecom services” is over, and “anybody” can create communications features. In other words, private communications networks will be possible and common.

“Telecom is a tail on an internet dog, and cannot determine its own fate,” Kim said. “What drives value,” in that context?”

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, February 12, 2018

Cable Dominates U.S. Internet Access

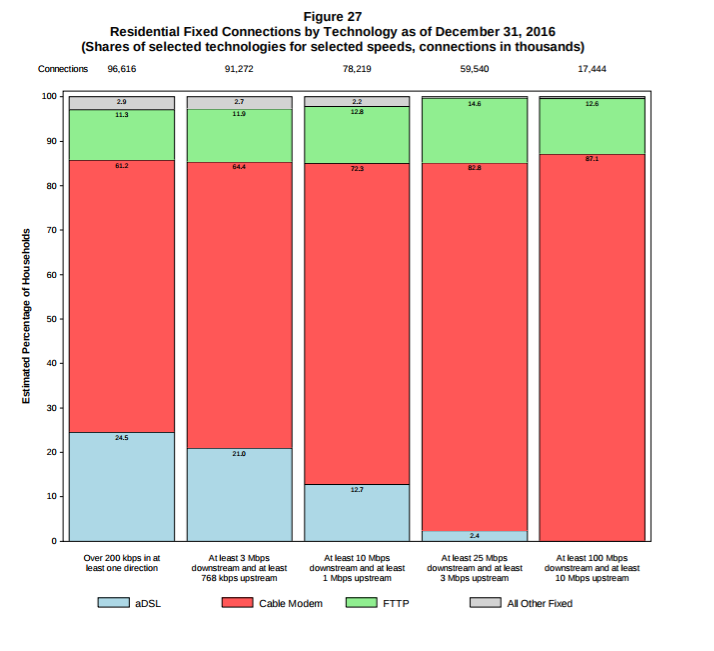

It is hard to overestimate the impact cable TV companies have had in the U.S. internet access business. At every speed tier, cable operators have overwhelming market share, as you immediately can tell from the following graph, where “red” represents cable market share at various speeds. At the higher end, cable has well over 80 percent of sold connections operating at a minimum of 100 Mbps.

But even at the low end, at speeds less than 3 Mbps, cable has 60 percent share.

For better or worse, those adoption statistics reflect deliberate capital investment decisions by U.S. telcos other than Verizon. Basically, many independent telcos have been financially unable to invest faster, while AT&T arguably has made a priority of mobile capital investment.

Verizon “benefits” from having made most of its fiber to premises investments a decade ago.

What comes next is not so clear. Some argue cable operators are in position to leverage their market control to raise prices.

Others might argue that telco fixed wireless is part of the strategy for catching up with cable. And AT&T recently has stepped up investment in gigabit services where it believes their is a business model.

Others might argue that at least AT&T and Verizon are looking past fixed segment competition and hoping to lead in the future mobile and untethered markets. That is part of the interest in both mobile video and fixed wireless built on the mobile network.

Yet others might argue that apps and services beyond internet access will drive revenue in a decade, not access, per se, reducing the value of access investments, in any case.

Still, the market impact cable TV has had is foundational. Its reliance on its own facilities, using different platforms than telcos use, has allowed it to upgrade faster, at lower cost, than telcos have been able to do using fiber to the home.

But most of the share losses have come from telcos other than AT&T and Verizon, which in recent years have been holding their own. In other words, you might argue both those firms have invested enough to get by, while prioritizing investments in mobility that clearly has driven revenue growth for both firms.

The issue now is how much investment has to be tweaked to maintain the “just enough” capex. Many would argue it does not make sense for either AT&T or Verizon to overinvest in fixed network internet access, as the financial return simply will not be there.

At this point, the fixed network internet access market is nearly a zero-sum game. That means most of the market share gains will have to come from other competitors. Such markets are tough.

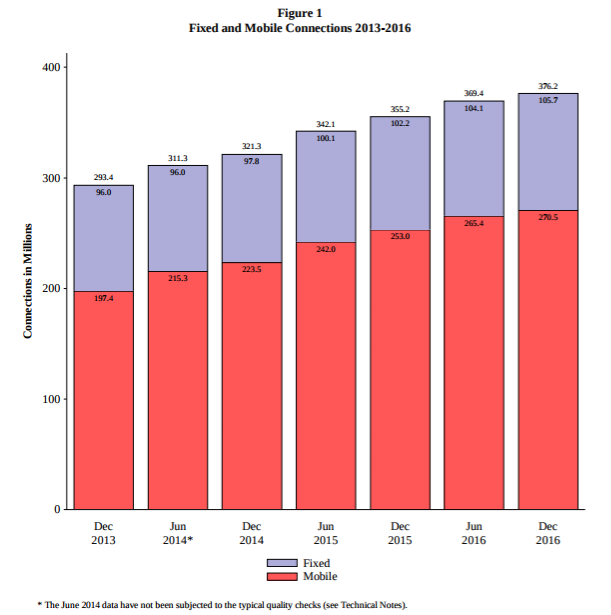

The total number of U.S. internet connections increased by about six percent between December 2015 and December 2016, reaching 376 million, the Federal Communications Commission reports. So there was growth, but at low and slowing rates.

With the caveat that speeds offered by some providers seems to be increasing about 50 percent per year, the 106 million fixed connections at the end of 2016 included 37 percent (39 million connections) operating between 25 Mbps and 100 Mbps, while 23 percent (or 25 million connections) offered speeds of at least 100 Mbps.

That suggests the policy of gradually investment by AT&T, for example, is largely defensive. That makes sense, one might argue, in the context of a business driven by mobility or video services, not internet access.

In the fourth quarter of 2017, for example, AT&T earned 85 percent of revenue from apps, not internet access.

Keep in mind that the FCC figures also represent consumer buying choices, not the services available to buy. Consumers make rational choices about internet access, buying services that provide the best perceived value proposition, not necessarily always the “fastest available” tiers of service.

They buy what is “good enough,” more often than they buy what they deem “best.”

So 62 percent of consumers chose to buy services running faster than 25 Mbps.

Some 38 percent of consumers bought services operating at slower speeds, though it is impossible to say for sure whether those customers were unable to buy faster services, or chose to buy slower services even when faster alternatives were available.

Some four percent of consumers (four million connections) bought services operating slower than 3 Mbps downstream.

Some 14 percent bought (15 million connections) services operating between 3 Mbps and 10 Mbps. Some 22 percent (23 million connections) purchased services running between 10 Mbps and 25 Mbps.

The median (half of connections faster, half slower) downstream speed of all reported fixed connections was 40 Mbps and the median upstream speed was 5 Mbps.

For residential fixed connections, the median downstream speed was 50 Mbps and the median upstream speed was 5 Mbps.

Most of the growth in total Internet connections is attributable to increased mobile Internet access subscribership. The number of mobile Internet connections increased 7% year-over-year to 270 million in December 2016, while the number of fixed connections grew to 106 million – up about 3% from December 2015.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Jio is Succeeding at "Destroying" the India Mobile Market

By now, telecom executives are well aware of the “disruption” market strategy, whereby new entrants do not so much try and “take market share” as they attempt to literally destroy existing markets and recreate them.

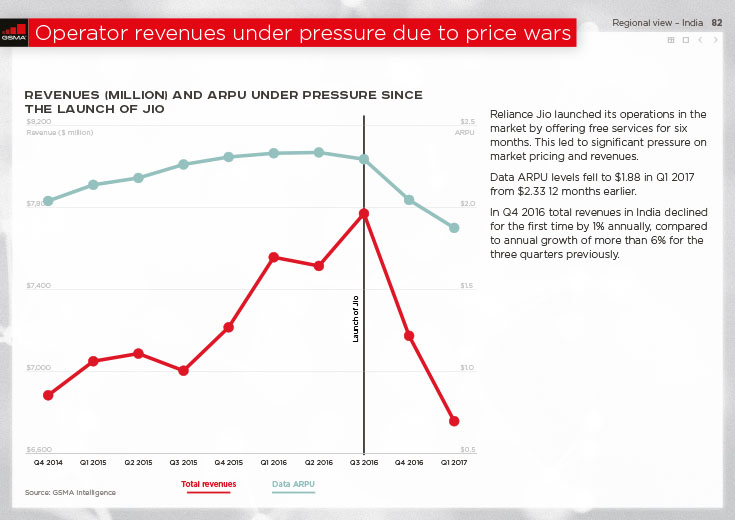

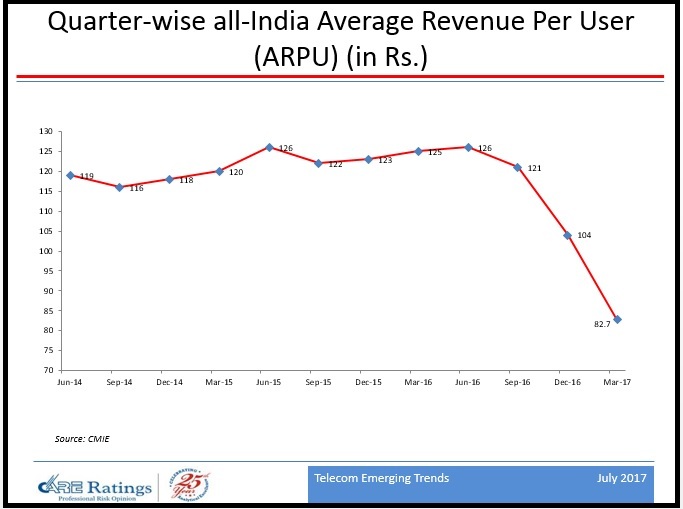

Skype and VoIP provider one example. The “Free” services run by Illiad provide other examples. Most recently, we have seen Reliance Jio disrupting the economics of the mobile market in India, offering free voice in a market where voice drives service provider revenues.

“Free” is a difficult price point in most markets. But free voice forever is among the pricing and packaging foundations for Reliance Jio’s fierce attack on India’s mobile market structure. “Free voice” does not only lead to Jio taking market share, but reshapes the market, destroying the foundation of its competitor business models.

At the same time, Jio hopes to become the leader in the new market, driven by mobile data, with far-higher usage and subscribership, and vastly-lower prices.

Disruption really is the strategy, not “take market share.”

RJio says it will reduce tariffs by another 20 percent whenever a rival matches its offer. You might guess at what will happen. Competitors will drop tariffs, but not to match Jio’s offers exactly, as that will simply trigger another deep discount in retail pricing that depresses revenue for virtually all service providers.

At the end of 2016, Reliance Jio did not appear as a market share leader. Some seven months later, Reliance Jio had taken about nine percent share, and kept growing. By the second quarter of 2018, Reliance Jio might have 14 percent revenue market share.

Where Jio really dominates is in mobile data, where Jio represents about 94 percent of mobile data usage and 34 percent of mobile data accounts.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, February 10, 2018

Convergence Means Vertical Integration; Horizontal Role Expansion

Formerly-separate industries--media, telecom and computing--have been converging for the better part of three decades. The industries have not yet completely fused, to be sure. But no longer is it possible to clearly delineate the boundaries.

Google and Facebook are huge ad-supported technology companies (hardware and software; content and access, in Google’s case). Comcast is a content creator, packager and distributor; so is Netflix. And so AT&T wants to be, also.

Are Netflix, Google and Facebook in the same business as Comcast, AT&T and Verizon? The answer actually matters for government policymakers and regulators, as well as firms and customers.

AT&T Chairman and CEO Randall Stephenson argues that its acquisition of Time Warner, a classic vertical merger, removes no competitors from any of the relevant markets and only positions AT&T the same way as other key competitors such as Netflix and Amazon.

"Reality is, the biggest distributor of content out there is totally vertically integrated,” said Stephenson, referring to Netflix. “They create original content; they aggregate original content; and they distribute original content.”

That is true for other major platforms as well, including Amazon, Google, YouTube and Hulu, he argues.

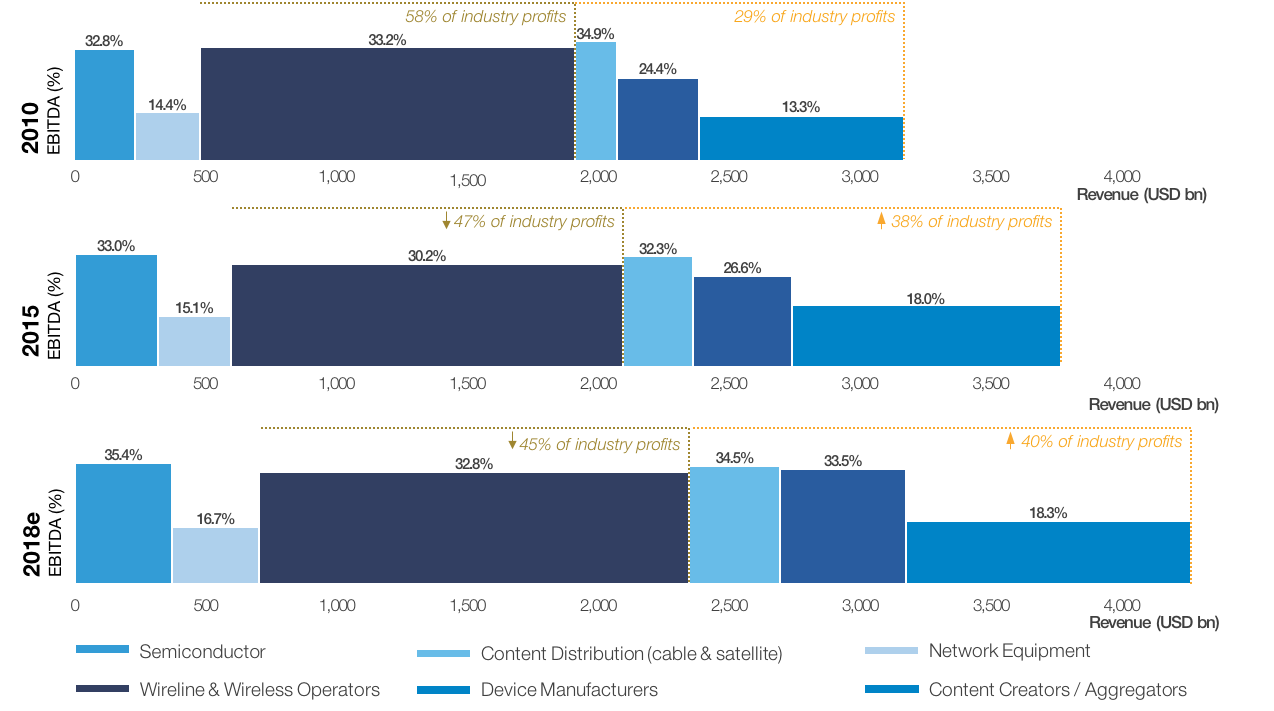

The issue is that roughly half of internet ecosystem profits now are earned by app providers, content creators and aggregators, device suppliers and others, while perhaps half are earned by access providers.

In the recent past as much as 60 percent of ecosystem profits were earned by access providers. So it is easy to describe the migration of value: it is moving towards apps, content and devices, and away from access.

That, in a nutshell, is why tier-one service providers who hope to survive must do as Comcast has done: transition from access to multi-role firms with assets in content creation and apps.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, February 9, 2018

The Next Big Switch

A new “big switch” is coming for the communications industry. Back in the 1980s, much was made of the idea that former over-the-air (wireless) broadband traffic (TV) was moving to the fixed network (cable TV networks) while narrowband traffic (voice) was moving to the mobile network. That was dubbed the Negroponte switch.

In more recent years, we have seen something different, namely the shift of all media types to wireless access, starting with voice, continuing with messaging and web surfing, and now video. Mobile bandwidth improvements are part of the explanation. But offload to Wi-Fi also drives the trend.

In the coming 5G era, that trend is going to accelerate, with the role of untethered and mobile networks continuing to grow.

The other notable change is that the distinctions between narrowband or wideband and broadband also have shifted. As we continually revise upwards the minimum speeds dubbed “broadband,” more and more use cases and traffic are actually no longer broadband in character.

When a high-definition streaming session only requires 4 Mbps to 5 Mbps, while broadband is defined as 25 Mbps, HDTV has become a wideband--not broadband--application.

Consider the performance characteristics of most networks. Wide area networks mostly will support applications requiring 10 Mbps or less. That is, by definition, no longer “broadband” use cases.

That also will be the case for most untethered networks as well.

In other words, most apps driving revenue (direct subscriptions) or value (indirect revenue streams) will operate in either narrowband or wideband speed ranges.

We might be in a “gigabit” era, but most apps will generate value and revenue in narrowband or wideband use cases.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

"Back" to the Narrowband Future

“Voice” has been steadily losing value as a revenue driver for communications service providers.

Still, voice will matter more in the future, but not “people talking to people.” Voice will be a key interface for interacting with computing resources. In many ways, that is an analogy for what will be happening in other areas of communications as well.

To be specific, even if industry revenue in recent decades has shifted from narrowband to broadband, in the next era revenue growth is likely to shift substantially back to narrowband.

That might seem crazy. It is most eminently realistic. Keep in mind that our old definitions of narrowband, wideband and broadband have evolved. Traditionally, narrowband was any access circuit operating at about 64 kbps. Wideband was any circuit operating between 64 kbps and 1.5 Mbps.

Broadband was anything faster than 1.5 Mbps.

These days, almost nothing matters but the definition of “broadband,” now defined by the U.S. Federal Communications as a minimum of 25 Mbps in the downstream. Using that definition, and recognizing the floor will keep rising, most of the coming new use cases will be “less than broadband, and many will be classically narrowband.

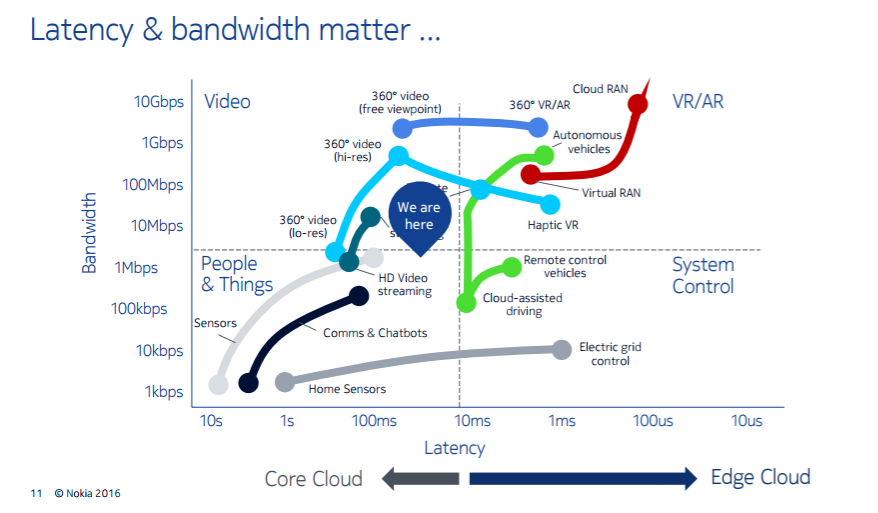

Consider the mix of existing and “future” applications. With the salient exceptions of 360-degree video, virtual reality and augmented reality and some autonomous vehicle use cases, virtually all other applications useful for humans (using smartphones, watches, health monitors, PCs, tablets) or sensors and computers (internet of things) require bandwidth less than about 25 Mbps to 50 Mbps.

The somewhat obvious conclusion is that most of the use cases and potential revenue will be driven by use cases that do not require “broadband” access speeds. Once upon a time, video was the classic “broadband” use case. These days, even high-definition video requires a few megabits per second support.

In that sense, using the 25-Mbps floor for defining “broadband,” even video has become a wideband app, requiring about 4 Mbps to 5 Mbps.

The big switch is coming.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...