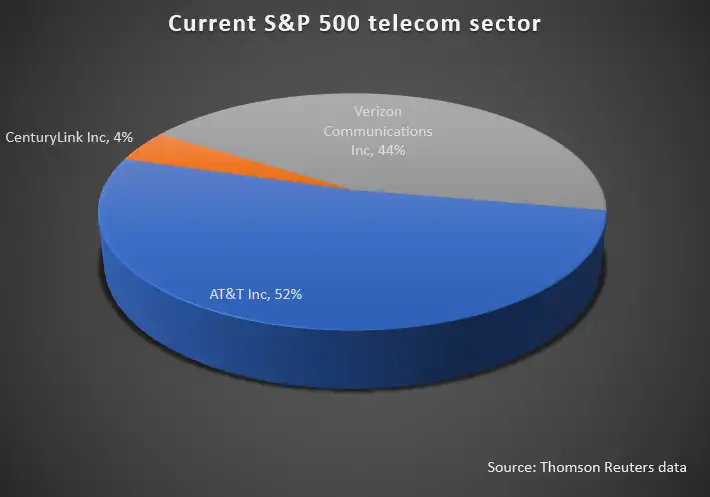

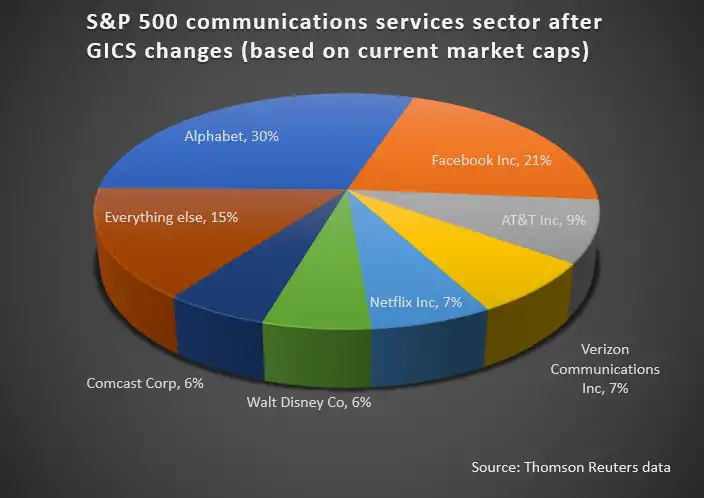

The S&P500 telecom services sector index will change in September, and be renamed “communications services.” And that is the least of the changes.

Internet app firms Facebook, Netflix, Google-owner Alphabet, Disney and Comcast will be in the index as well.

Irrespective of you views on the wisdom of putting traditional value plays into the same index with media and internet apps, the new index might lead to a reevaluation of the price-earnings multiple for telecom assets.

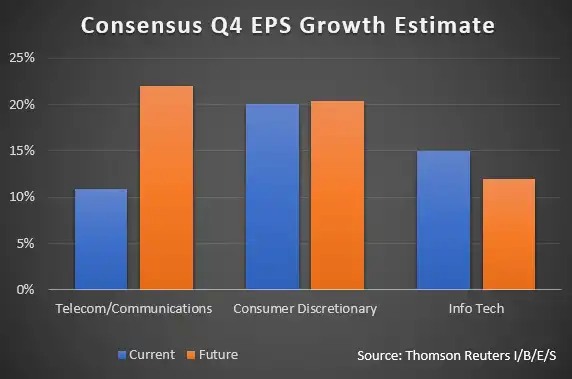

The new communications sector index implies a price-to-earnings ratio of perhaps 19 times (the impact of adding internet app firms) expected earnings, nearly double the sector’s current multiple, according to Thomson Reuters, reflecting the different profiles of internet sector firms.

That does not mean an automatic reevaluation of the underlying values of assets in the index, which will continue to feature some slow-growing and high-dividend firms, plus some fast-growing, low or no dividend growth plays.

Still, many observers believe there is some potential lift for “telecom” asset values, if the mix of assets held by the constituent firms continues to evolve, producing companies with a mix of assets and growth profiles.

Some might argue the index changes do reflect a larger underlying transformation of the media, communications and internet application industries, though. The new index assumes connectivity services, content and applications are logically part of a single ecosystem.

The boundaries between media, content, apps and access are porous. Firms such as Comcast and AT&T already derive significant percentages of core revenue outside the realm of connectivity services.

In fact, some might accuse Comcast of running away from its core business as it contemplates buying Twenty-First Century Fox assets, a move that, if successful, would further diversify Comcast away from connectivity revenues.

No matter. The growing reality is that the formerly-separate media, internet app and access businesses are “converging and fusing.” Any particular firm is going to own a mix of such assets.

And so the creation of a new communications index is suggestive of the new industry structure that is emerging. In the immediate future, the talk is going to be of big mergers in the media space. That is going to fuel even more talk--informed or uninformed--about the dangers of “bigness” in all of these formerly-separate spaces.

That brings dangers as well. We thought breaking up the AT&T system would enhance innovation and competition. It has, but perhaps less so than expected. We thought the Telecommunications Act of 1996 would also help. It has, though perhaps much less than was expected.

We might argue about whether the antitrust actions taken against Microsoft actually were effective, or whether the shift from “personal computing” to an “internet-lead” industry would have lead to a weakening of potential Microsoft monopoly in any case.

Now we have some observers arguing that traditional notions of monopoly are wrong; that even when there is lots of innovation; lots of new product commercialization; declining prices and higher value, consumer welfare might still be harmed.

That is a potential danger. Economists cannot measure everything that matters, and not all that matters can be measured. But numbers still matter when trying to assess consumer welfare and consumer harm. Perhaps the new thinking is that more weight needs to be placed on externalities.

But even externalities have to be quantified to assess potential benefit and risk. And regulatory history should not lead us to be too optimistic about the intended and unintended consequences of our actions.

What is clear is that content, media, apps, internet and communications can be viewed as aspects of the current reality of “computing.” And that means change is coming. No computing era lasts forever. In fact, every couple of decades there seems to be a new era arriving, as a new mobile generation arrives every decade or so.

The computing (and content, and app, and access) industry will evolve in the next era. We have no idea what we will call it. We have no idea how to quantify the impact on industries, firms and revenue models. We can predict that--based on history--not even Facebook or Google can dominate the next era as they dominate the present.

No firm that lead in one era has ever lead in the succeeding era. The implication is that regulating the leaders of the present era is less important than watching for, and promoting the next era, which naturally will produce new leaders.

We can debate the value of throttling today’s leaders to allow tomorrow’s leaders to emerge. History suggests those leaders are going to emerge anyhow, and that our policy actions might, or might not, help. In fact, they might well harm as much as they help.

source: Reuters