“Near-zero pricing” (or the perhaps-better known expression of “marginal cost pricing”) is a business principle that underpins and complicates business strategy in a wide range of industries, ranging from internet apps to computing; retailing to media; communications and consumer electronics.

Marginal cost is a universally accepted pricing principle, representing the incremental cost to produce one more unit. The key idea is that it is profitable to keep producing additional units right up to the point where marginal cost and marginal revenue hit zero. At that point, one stops producing, as losses will occur.

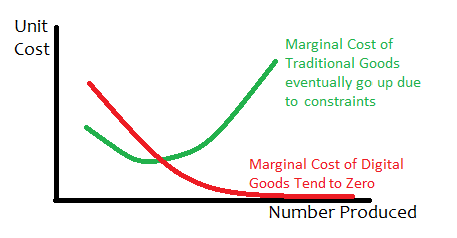

But physical goods and digital goods have different marginal cost curves. For a communications service provider, at some point there is so much demand that a network has to be upgraded. That adds capital investment cost, so the marginal cost actually has to rise.

Digital products are different. Once the original is created, the marginal cost can actually remain infinitesimal, even with vastly-greater usage. That also implies that retail price can be very close to zero, and still yield a profit.

In fact, some believe zero marginal cost might be among the most-important business drivers in the early 21st century, though the idea remains controversial.

A company that is looking to maximize its profits will produce “up to the point where marginal cost equals marginal revenue.” In a business with economies of scale, increasing scale tends to reduce marginal costs. Digital businesses, in particular, have marginal costs quite close to zero.

In other words, the incremental cost of adding one more Gmail user or one more Facebook user are infinitesimally small.

But marginal costs also are immeasurably small even in some industries with high capital intensity. What, for example, is the incremental cost to supply one more megabyte of internet access capacity; one more minute of voice usage; one more text message, on a network that already is built and operating?

To be sure, additional sales help most businesses, digital or physical.

But the danger of pricing at marginal cost (increasingly a price very nearly zero) is that “where there are economies of scale, prices set at marginal cost will fail to cover total costs.”

Think of the “sunk cost” of building a mobile or fixed network. Retail pricing has to be set at a level that allows recovery of that initial network cost, plus profit. So overall pricing cannot be set at the marginal cost of the last units, but at a rate including recovery of sunk costs.

Add to that the possibility that product prices for the end user also include revenue generated by third party partners (advertisers, retailers on a platform) and end user consumption can actually be subsidized.

The point is that even if the incremental cost of supplying one more megabyte of data consumption, one more minute of a voice call or one additional text message is quite close to zero, a service provider cannot price at marginal cost, forever.

That accounts for the business advantage many app, content and services providers hold over a facilities-based connectivity provider selling apps and services. An over-the-top app provider does not have to recover a physical network’s sunk costs.