If there are 60 million U.S. homes able to buy fiber-to-home services, and a total of 139 million U.S. housing units, then FTTH availability stands at 43 percent. The average of European Union homes able to buy FTTH services is 30 percent.

Wednesday, July 17, 2019

U.S. FTTH Coverage Exceeds EU

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, July 16, 2019

What Matters More, Inputs or Outputs?

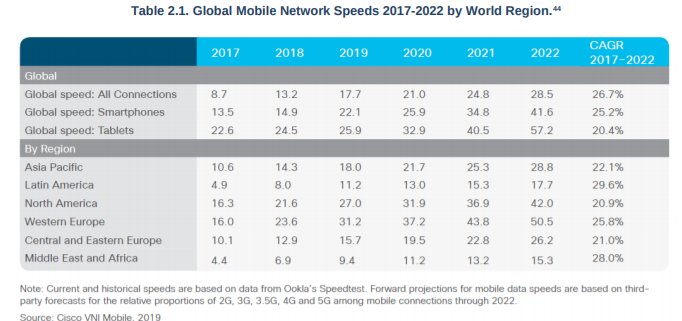

Productivity is one thing, internet access speed another. Knowledge creation is one thing, average speeds another. Though a few small countries rank higher, the most productive larger country is the United States.

That rarely is discussed when observers complain about the speed, price or availability of internet access in the United States. The point is that what matters is the ability to wring economic and social value out of communications. Without context, it is difficult to evaluate the value of speeds, coverage or other measures of quality.

Nor, it should be noted, are various speed estimates in agreement. Looking only at mobile network speeds, some point out that U.S. mobile speeds are well down the rankings. Other estimates suggest North American speeds (a proxy for U.S. speeds) are among the highest in the world.

Put simply, all measures of internet speed are input measures. What matters are output measures. The value any nation can wring from internet access is what matters.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

How Wrong is FCC Broadband Data? Not that Much, Says Phoenix Center

Many critics rightly say the Federal Communications Commission’s methods for determining broadband coverage by terrestrial networks (25 Mbps minimum downstream) are wrong, and overstate the amount of access.

Virtually everyone might agree with the general statement. What has never been clear is the magnitude of the collection error. Is broadband availability wildly overstated, or just a little overstated?

George Ford, chief economist at the Phoenix Center for Advanced Legal and Economic Policy Studies, has an answer: 3.3 percent overstatement. Put another way, some four million U.S. homes are assumed to have broadband that do not. Ford uses a 126 million figure for U.S. housing units.

Using a national housing units base of 138.5 million, that is an overcount of less than three percent. Estimates of housing units are nuanced, as some units are not occupied, occupied for only parts of a year, and include rooms in other structures, boats and other unusual situations.

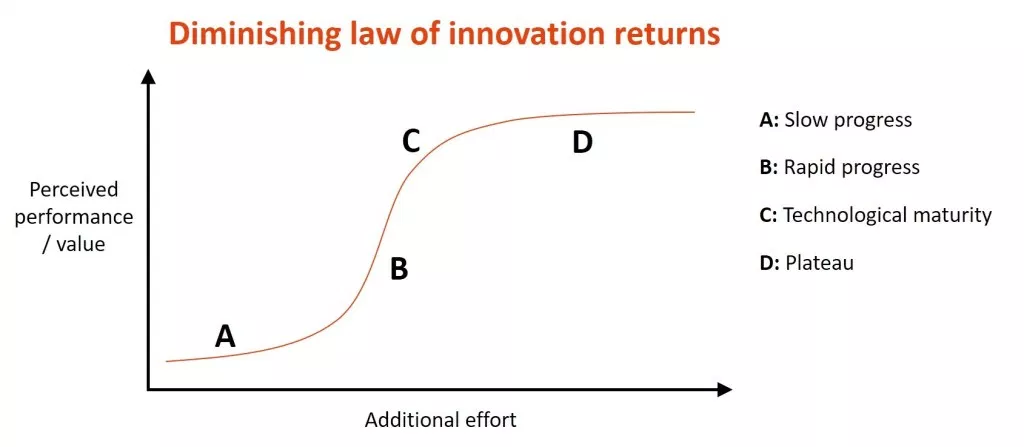

One might argue that the overstatement is relatively minor. At a larger level, one might also argue that getting the last few percentage points of “solution” for any “problem” tends to be wildly more expensive or difficult than producing solutions for the middle 80 percent to 90 percent of cases.

That might be as true for weight loss as it is for building or enumerating communications infrastructure.

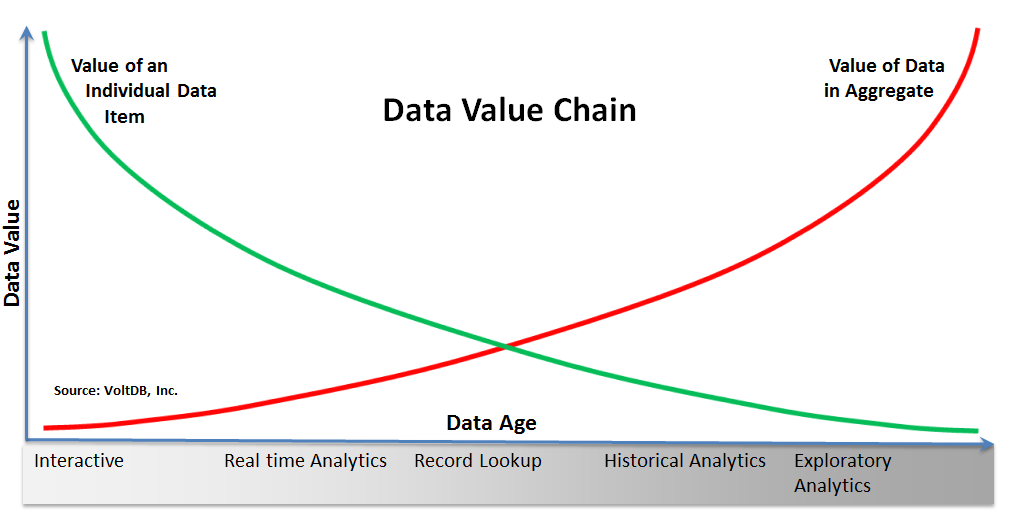

One might argue that most of the value of a data set related to individual behavior is captured in the first 50 percent of acquired data (much of the latter behavior is repetition of past behavior). The incremental value of the last few percentage points of data is low, relative to the earlier data.

The Gaussian distribution (Bell curve or normal distribution) probably illustrates the concept as well. Most of the results of any construction project (homes connected, miles built) are likely to occur in the middle 90 percent of activities. That has the same general implications as the law of diminishing returns might suggest.

Slow progress at first results in a rapid rate of change in the middle, until incremental value slows, stops or becomes negative.

That is true for fixed communication network costs as well. Connecting the last few percent of locations, typically the most isolated and rural places, is the most expensive.

The concern about rural broadband coverage is well placed. Progress also tends to be slow, in part because we keep moving the goalposts (faster speeds over time mean the work never ends), and partly because supplying the last couple of percent of locations with fixed network access is wildly expensive to prohibitive, even with subsidies.

Rural networks might cost three times more than urban networks. Rural networks might cost four to five times more than suburban networks.

The general point is that there is a law of diminishing returns at work, as elsewhere in life.

Better data collection is better than worse data collection. But the FCC’s data seems to have captured most of the value, if inaccurate at the margins. Improvement is possible, but not as much as many seem to believe.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, July 15, 2019

Frontier Says West Virginia Business Model Unsustainable

The whole idea behind subsidies for communications in rural areas is that there is, in effect, no viable business model without the subsidies, at least where it comes to cabled networks with provider of last resort (universal service) obligations. An analysis by CostQuest suggests the capital investment per customer location, for conduit and poles, is approximately 5.6 times higher in rural areas as in suburban areas.

For fiber optic cable, the capital investment is approximately 4.2 times higher in rural areas as in suburban areas. Those two expenses account for 66 percent of total capex.

Ignoring for the moment the thorny issue of costs for different types of platforms (mobile, fixed wireless, cable hybrid fiber coax, fiber-to-home, digital subscriber line), overhead and public policy choices, fixed networks in rural and isolated areas are quite expensive to build.

Recently, a Frontier Communications executive even said the firm’s business model was unsustainable. That might well the case elsewhere as well. That includes areas of low population density but also in highly-urban areas such as Singapore. But Southeast Asia also is an area where the business model is becoming unsustainable.

It is becoming clearer that the fixed network telecom business is losing its ability to sustain itself, as it becomes harder to generate core revenue. The point is that, over time, a greater number of service providers might well find their business models are becoming unsustainable

In other words, one might argue, the core business model is failing. That is why firms such as Frontier Communications now are in greater danger of bankruptcy. Windstream and its facilities unit Uniti might also face bankruptcy danger.

A difficult business model is why Verizon and AT&T (and other telcos and internet service providers) are looking to fixed wireless as an alternative to fiber to the home.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

New Proposal for Freeing Up 370 MHz of C-Band Spectrum for U.S. 5G

ACA Connects, the Competitive Carriers Association (“CCA”), and Charter Communications have filed a new proposal for clearing C-band spectrum with the Federal Communications Commission.

The proposal proposes to free up at least 370 megahertz, while satisfying incumbent user requirements for C-band video delivery, compensating satellite users and providing an alternative way for users to replicate their C-band requirements.

As always, each proposal, while clearing spectrum, also serves the discrete financial interests of each proposing group. The straw man proposal by the C-Band Alliance releases a much-smaller amount of spectrum, raises the value of the remainder of the spectrum C-Band Alliance members would hold, and also creates scarcity of C-band spectrum, which raises likely prices for any auction of the assets.

The new proposal by ACA Connects, CCA and Charter likewise provides benefits. It would create a big national fiber transport network that also provides other advantages for the cable operators and programming networks in providing data services, for example.

“C-band customers and earth station users made whole and given long term certainty through funding (subject to true up) and reimbursement of certain costs: a. For all multichannel video program distributor (“MVPD”) C-band users and MVPD programmers to transition off the C-band, funding and reimbursement to include the cost of redundant, future-proof assets that they would own and operate (fiber construction in some cases and Indefeasible Rights of Use (“IRUs”) in others); and b. For all satellite industry providers and existing C-band users that remain on the C-band, funding and reimbursement to include the costs of transitioning to a reduced amount of spectrum for continued satellite service,” the filing notes.

In other words, the consortium shifts spectrum use from video to 5G in a way that gives the cable operators funding for, and control of, a new national optical fiber transport network that supports all their current and future services.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

FCC Prepares to Limit Franchise Fees

Since the mid-1980s, municipalities have collected franchise fees from cable operators providing video entertainment services, as cable operators use municipal rights of way. Those fees traditionally are set on a “percent of gross revenue basis.”

The new issue is whether the “percent of revenues” formula applies solely to video services or also includes communication services. The other issue is whether the statutory five-percent maximum franchise fee includes both cash and other in-kind payments.

The U.S. Federal Communications Commission plans to address those issues at its August 2019 meeting.

The new rules would prohibit franchising authorities from using their video franchising authority to regulate most non-cable services, including broadband Internet service, offered over cable systems by incumbent cable operators.

New rules would treat video-related, in-kind contributions required by franchises as well as cash payments as part of the statutory five-percent franchise fee cap.

The new rules also would preempt any imposition of fees on a franchised cable operator that exceeds the formula set forth in section 622(b) of the Cable Television Consumer Protection and Competition Act of 1992, and the rulings contained in the Third Report and Order, whether called as a “franchise” fee, “right-of-access” fee, or a fee on non-cable (telecommunications or broadband) services.

The new rules would also bar additional franchise requirements for providing communications services once a cable operator already has a franchise agreement for video.

The thinking here is broadly that incentives to invest in internet access and other communications services are discouraged when new taxes on gross revenue up to five percent are levied--in the form of franchise fees--on the additional gross revenues from those services.

The background is that franchising agreements often include requirements that cable operators provide free cable and broadband service to government or educational entities, construction of special fiber networks to government buildings, and payments for public access channels that seldom are watched.

The issue now is whether that franchise fee applies to all services cable operators deliver over their cable systems--including internet access, voice services, public Wi-Fi, mobile service or other enterprise special access connections-- even if the operator has already paid for access to the right of way.

Some franchise authorities, such as Los Angeles, are piling up surpluses because the city is not sure how to spend the franchise fee collections, some note.

As often is the case, financial interests collide. U.S. cable TV revenues peaked in 2010 or 2011 at about $54 billion and are predicted to fall to $36.75 billion by 2023, by some estimates.

Regulators naturally want to replace that lost revenue (a percentage of gross revenue) by tapping communications services covered by other regulatory rules (Communications Act of 1934, as amended).

Cable operators in turn argue they already have paid for use of rights of way for a single network that now provides multiple services.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sunday, July 14, 2019

A "Hellishly Difficult" Challenge

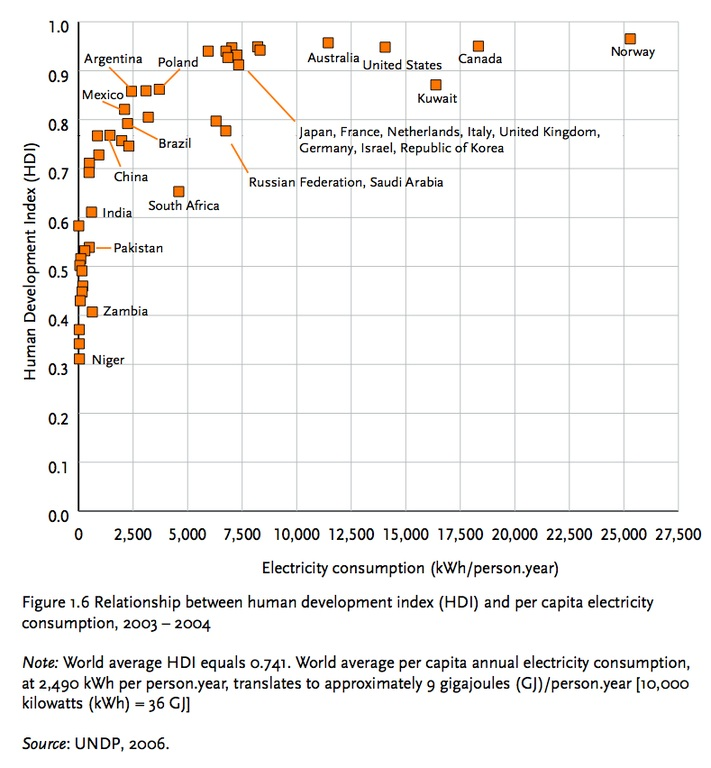

Some argue that most countries can supply their current energy requirements using only

But that is probably not the right question. The bigger questions are whether future energy consumption requirements can be met, using renewable sources, and whether the historic correlation between energy consumption and economic development can be broken.

What is not so clear--and will require both lots of human ingenuity and some technology development--is whether most nations can improve living standardsf or their people while at the same time reducing carbon and other footprints.

It is likely to be hellishly difficult. Some will argue we do not need “growth.” Others will argue that is an immoral position, where it comes to most people of the developing world.

source: Anthropocene

source: Anthropocene

As Dennis Anderson argues in the UN Development Program’s Energy and Economic Prosperity, modern, abundant energy can improve living standards of billions of people, especially in the developing world, who lack access to services or whose consumption levels are far below those in industrialized countries.

But that means energy production and consumption levels far above what we now experience.

"No country has been able to raise per capita incomes from low levels without increasing its commercial energy use," said Anderson.

The issue is whether that correlation can change, allowing development at lower levels of energy consumption. That is where the ingenuity and technology development will be required.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...