Sunday, April 5, 2020

After Corona, We are One, But We are Many

Stay safe out there, planet Earth. Corona Will Lose.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

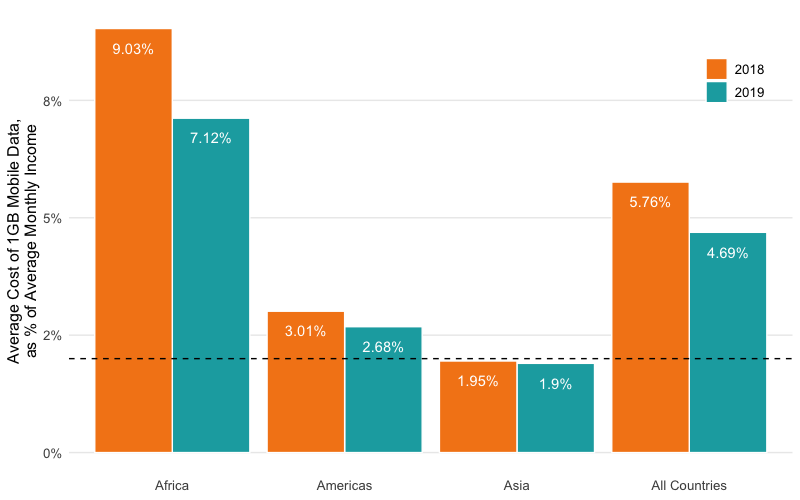

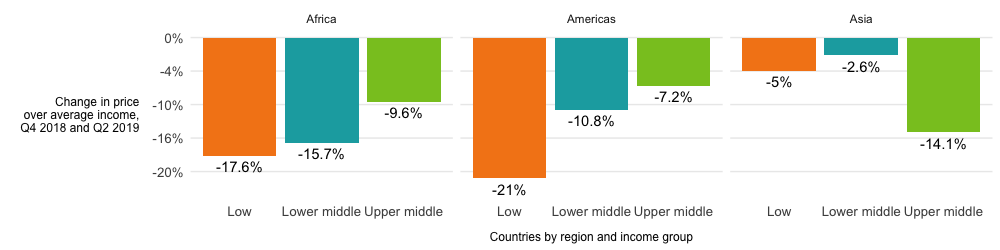

Mobile Internet Prices in Low-Income Countries Confirms Long-Term Telecom Price Trends

Since the 1980s, connectivity product prices have fallen over time. That is true of mobile internet prices, voice and messaging, internet transit, cloud computing, mobile service, long distance calling and fixed network internet access.

The latest study by the Alliance for Affordable Internet confirms the trend.

In 2019, low-income countries made impressive strides towards affordability. In 2019, low-income countries increased their affordability scores three times as much as middle-income countries, on average, according to the Alliance for Affordable Internet.

source: Alliance for Affordable Internet

The AAI index measures infrastructure availability and take rates, not actual prices. But the index then is correlated with prices for 1 gigabyte mobile prepaid plans.

As always, the correlations might be different if other plans offering more usage are compared, as price-per-gigabyte tends to drop as volume rises, but absolute price might climb. That is important, as typical usage varies by country.

In other words, if users in some countries buy plans featuring 3 GB or 10 GB, that means spending will be higher, because usage is higher. Conversely, spending will be lower when most users buy 500 MB to 1GB.

Posted rates are one thing; actual buying behavior and usage can be quite different. But prices are dropping, everywhere.

source: Alliance for Affordable Internet

The report also confirms what you would expect, that competition also increases affordability.

Still, low-income countries saw a 15.6 percent increase in their affordability scores from 2018 to 2019, as well, compared to 4.5 percent and 5.1 per for lower-middle and upper-middle-income countries, the Alliance reports.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, April 4, 2020

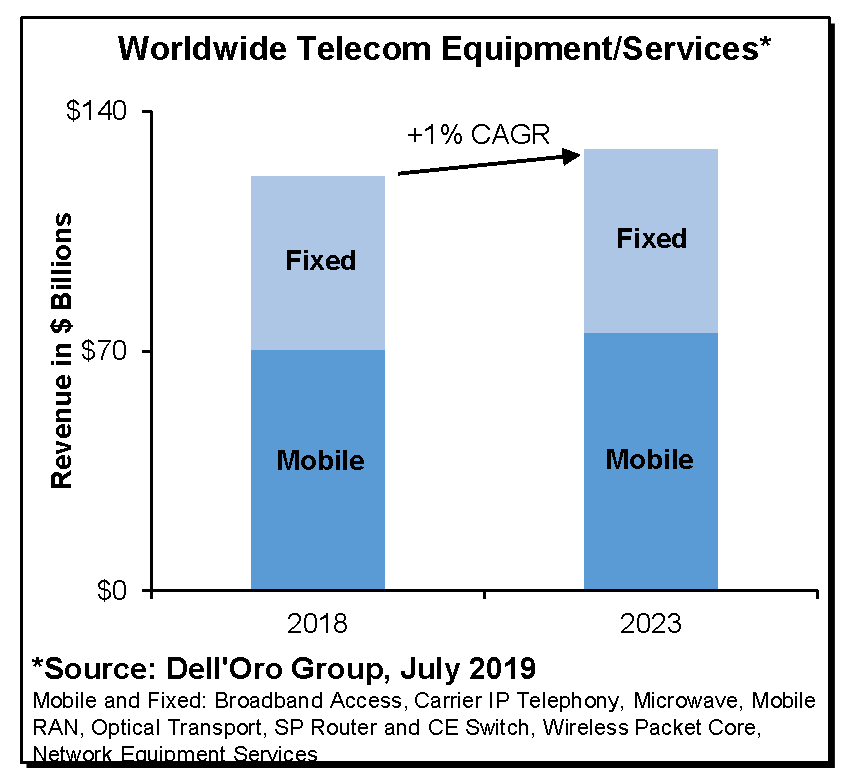

Capex Forecasts Suggest Expectations of Slow Revenue Growth

Global connectivity supplier capital investment (mobile and fixed) is projected to grow at a one percent compound annual growth rate between 2019 and 2022, according to the Dell’Oro Group. Other forecasts call for a decline in capex after 2022, as 5G and fiber investments to support 5G and fixed network broadband projects are completed.

As a rule, capex budgets for service providers in developed markets are relatively fixed, year over year, with some ebbs and flows largely related to construction of each new next-generation network.

As always, mobile investment is higher than fixed network investment, for one simple reason: mobility is where the bulk of revenue growth is expected.

There also are regional differences, as Latin America and Asia are where growth will be higher, compared to Western Europe and North America, where growth will be lower, according to Standard & Poors.

Still, mobile capex often grows when a new next-generation network has to be built, and then tapers off as construction moderates. So there is some chance that even mobile capex might not grow too much as 5G networks are built.

In fact, fears that mobile operators could not afford 5G are proving incorrect. Just a few years ago, projections of 5G infrastructure cost were so high that many argued the networks could not be built. In fact, some speculated that 5G networks would cost 10 times that of 4G. Others only expected 5G costs to double or triple.

Capital investment levels, though, seem not to be skyrocketing, even as 5G is built. In fact, there is growing evidence that 5G can be built within existing capex budgets.

There are several reasons. First, mobile operators are being deliberate in their spending and build rates. Also, capital expense is shifted from 4G to 5G, as always happens when a next-generation network is under construction.

Also, network architects, working with better radios, have found that 5G mid-band signal coverage is almost identical to that of 4G, meaning less physical infrastructure actually turns out to be necessary. Also, low-band spectrum is being used for 5G rollouts, limiting capacity growth, but also requiring fewer new tower or radio sites and backhaul construction.

Better technology, allowing lower cost builds, also is at work.

The bottom line is that mobile and fixed network capex reflects assumptions about revenue growth, as capex typically is set as a percentage of expected revenue.

Current capex assumptions suggest connectivity suppliers generally expect slow revenue growth in Europe, North America, South Korea, Japan and Taiwan, with faster growth expected generally in wider Asia and Latin America.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, April 3, 2020

Google Shows Value of Location Data, Also Spotlights Why Much Telco Data has Little Value

Google Maps now is being used to produce Community Mobility Reports, using anonymous data, showing how busy retail locations are, in the wake of pandemic-driven stay-at-home policies.

In Canada, for example, visits to retail and recreation sites are down 59 percent, while visits to transit stations are down 66 percent. Visits to workplaces are down 44 percent. In France, trips to retail and recreation locations are down 88 percent, visits to grocery stores are down 72 percent, while trips to parks are down 82 percent. Transit station trips are down 87 percent.

One observation: Location data has been touted as one data source mobile service providers possess that has value in a commercial sense. In the internet era, it also is clear that app providers have reasonable approximations to that same data store.

So what entity ends up creating a useful information service for health planners and governments that actually uses location data to show whether citizens are obeying the shelter in place rules? Google, not any single telco, collection of telcos, or non-profit entities funded by telcos.

Connectivity providers seem to insist they are not just dumb pipes, but perhaps reality suggests they truly are. There is a business model for access and transport, to be absolutely certain.

But legitimate questions can be raised about the revenues which can be generated by that function in the ecosystem. Moreover, legitimate questions also can be raised about telco roles in creating apps, as well.

To the claim that “we have lots of valuable data stores, such as location data.” one might well retort that “so do many app providers.” And at least in this case, Google has shown the ability to create useful value from such data stores, where no telco apparently has been able to replicate.

That is not a new story. Most observers who do not work for telcos have argued in the past that telcos are not good at innovation. Worse, the “data stores” they often claim are potentially so valuable might be just that: “potentially” valuable.

Put another way, maybe not so valuable, after all.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, April 2, 2020

North American Retail and Restaurant Visits Dropped 100% in March 2020

These bits of data from Prodco Analytics and OpenTable, reported by the Wall Street Journal, graphically illustrate the effects of Covid-related retail shuttering. Retail visits in North America fell off a cliff in March 2020, reaching a negative 100 percent by the end of the month, while visits to restaurants likewise fell 100 percent about the third week of March 2020.

That could hardly be anything but the case after all restaurants, bars and nearly all retail locations were ordered shut by government order in March 2020, in most jurisdictions.

Small businesses will be severely challenged to come out the other side, and many will likely not make it at all. Unprecedented.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

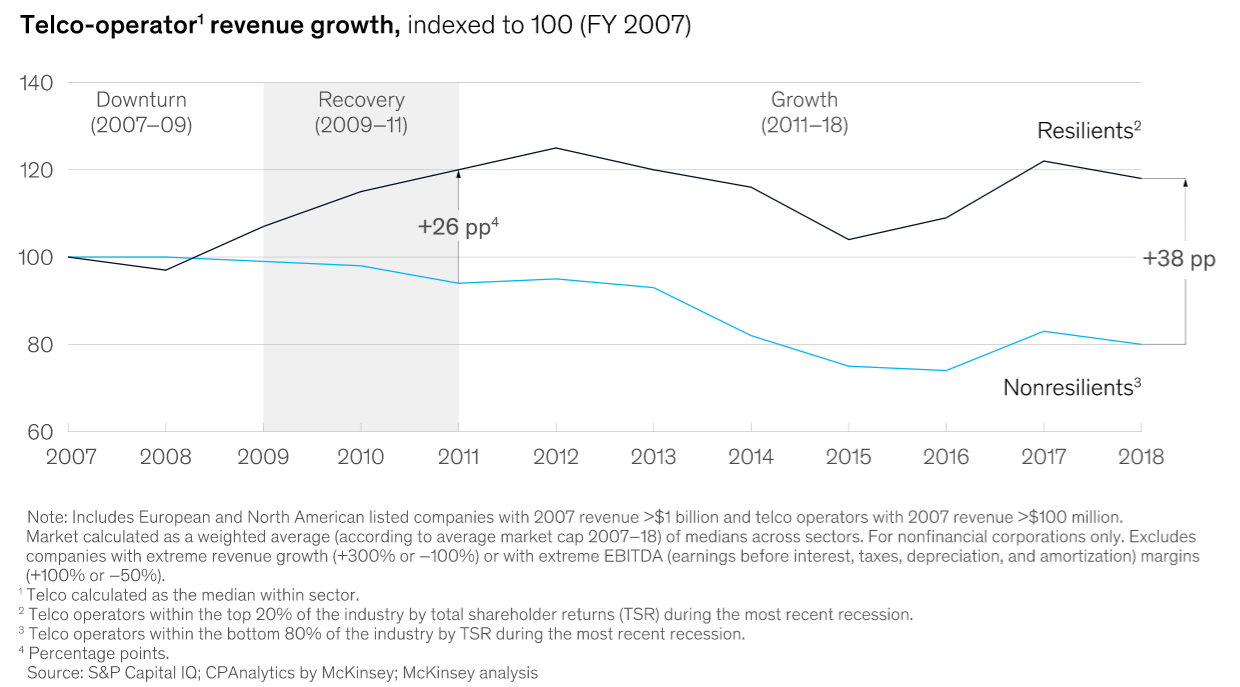

Post-Pandemic Service Provider Growth Rates Might Vary

Nobody yet can predict how consumer behavior could change after the end of the Covid pandemic. If past behavior in the aftermath of major global recessions applies, connectivity providers will see revenue impact based on underlying growth trends in each market.

Developing markets might make a relatively-swift rebound after a modest dip, might see flat revenue or possibly even grow, but only at a slower rate. Service providers in developed markets arguably face more risk, in some regions.

“From 2007 to 2009, many European operators’ average revenue per user dipped by more than 15 percent, and churn rates rose by the same amount for operators in both North America and Europe,” say consultants at McKinsey.

Revenue and profits in North America are stronger, so there might be relatively slight impact.

The Organization for Economic Cooperation and Development countries, on the other hand, saw only a one-year flattening of growth in the wake of the internet bubble in 2001, but saw sustained, multi-year drops in revenue after the great recession of 2008, likely for reasons not related directly to the economy.

But some data suggests global revenue after 2008 was buoyed by growth in developing markets, even if some developed markets did not recover as quickly. -

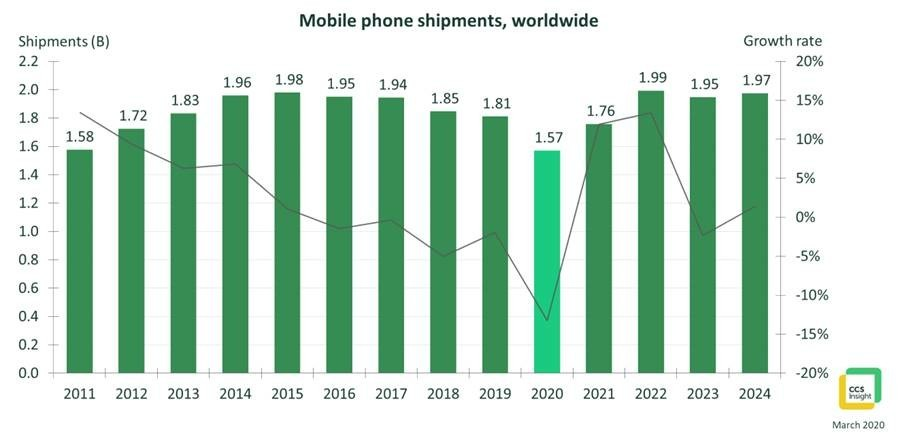

Smartphone sales are likely to suffer in the near term, however.

It could hardly be otherwise when major parts of the economy are simply shut down, supply chains have been disrupted and on top of that we must work through an unprecedented planned effort by governments to throw economies into recession.

Smartphone sales globally dropped 40 percent in February 2020, for example. CCS Insight now predicts that phone sales worldwide will drop to a ten-year low in 2020 overall.

Sales of 1.26 billion smartphones sold globally in 2020 would represent the lowest sales in a decade. The global mobile phone market is expected to slow by 13 percent in 2020, with shipments in the second quarter of the year predicted to fall by 29 percent, CCS Insights predicts.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, April 1, 2020

Will Pandemic Behaviors Persist?

It is to be expected that consumer behavior in unprecedented times will feature at least temporary aberrations. It could hardly be otherwise with much of the economy shut down and people living through a pandemic.

The big issue is whether--and to what extent--those behaviors might persist, on a permanent basis. Some would argue the great recession of 2008 caused permanent changes of behavior, and we might see greater changes for health reasons after the Covid-19 pandemic.

Looking at U.S. consumer spending about seven years after the start of the 2008 recession, Macy’s executives noted a “permanent” shift to automobiles, housing, health care and digital experiences.

Leisure travel, dining out and attending events (experiences) also gained favor. A general increase in buying based on “value” also arguably occurred. A decade later, many of those trends of spending caution still seemed to be in effect.

To be sure, there are other trends not directly related to post-recession thinking: a shift of retail to digital channels, environmental, “buy local,” socially-responsible behavior and organic product trends. Many have noted the preference for experiences rather than goods.

Looking only at content consumption, the pandemic has boosted use of, and interest in, media of all types.

Daytime viewing is overtaking primetime for ratings numbers, according to Samba TV. Daytime viewing numbers are up 121 percent year over year and total viewing time is up 85 percent. Viewing of cable news has also seen a sharp uptick between the hours of 9 a,m, and 4 p.m. as well.

Nobody expects those trends to persist once people go back to work and school. Virtually everybody seems to expect a permanently higher level of online shopping. Some believe a permanent shift in remote work is possible, with a shift of significant higher education to online delivery as well.

A reasonable baseline case is that underlying trends in place before the pandemic become stronger. Even the hard-hit activities that involve larger gatherings of people, travel and lodging are going to recover, albeit with interaction precautions likely persisting in some ways.

Supply chains already were changing, prior to the pandemic. That likely is a permanent shift. But that trend was underway before the pandemic. Disaster preparedness will improve, though. History suggests many far-reaching potential changes are unlikely to happen. But pre-pandemic trends are likely to accelerate.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

Enterprise Leaders Say They Now Use Generative AI Tools Routinely

A new survey by the Wharton School (University of Pennsylvania) Human-AI Research suggests that enterprise leaders now use generative arti...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...