Lots of people have offered, and will continue to offer, advice about how Sprint can do better in the U.S. mobile market, whether or not the AT&T deal to buy T-Mobile USA succeeds, or not. Advice, one might argue, is easy to give, especially when it concerns how any firm, lead by any set of talented managers, can change its fundamental position in a market whose structure is fairly well fixed.

Though some will question the continued relevance, a long-standing study of firms in many industries, taking a look at market share, quality and profit margin, suggests that it is very hard to change firm position in an established industry. Market share patterns

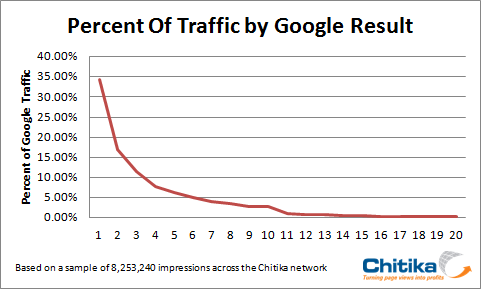

Though the existence of a correlation is not necessarily a causal relationship, there is relatively significant evidence that markets develop patterns. Pareto_principle Among the more-enduring patterns is a tendency towards market concentration by a handful of leaders.

Some might argue, for that reason, that the current U.S. mobile market structure is not unusual, and might become even more concentrated over time. The informal rule of thumb might be that in any market, most of the share i(80 percent or so) is held by a small number of providers (perhaps 20 percent or fewer).

The U.S. mobile industry is more concentrated than that, but you get the point. It would be difficult under the best of conditions for Sprint Nextel to dramatically change its position in the market. But, that noted, there are some apparent differences of end user behavior that could provide something of an opening.

Some of us would not say the differences necessarily offer Sprint a way to change its market position in a dramatic way, but might offer a way to help solidify its current position. The difference is the apparent preference for Android among Sprint users, or perhaps Sprint’s willingness to bank on Android for some highly-popular devices such as the HTC Evo line.

Note recent Yankee Group surveys indicating that Sprint users are heavy users of Android devices. It is of course possible that the data reflects Sprint’s historic inability to sell the Apple iPhone, forcing Sprint to emphasize the HTC Evo as a lead offer, and thus producing the skew Yankee Group found.

One might similarly argue that Verizon Wireless faced the same problem in the days when it also could not sell the Apple iPhone. If so, it always is possible that the Android preferences illustrated by Yankee Group are a tactical, short term user demand trend that easily could change in the future.

Still, no matter what happens with the AT&T bid to buy T-Mobile USA, Sprint is going to have to work pretty hard simply to solidify some distinctive position in the market, even as a “distant third” provider, compared to Verizon Wireless and AT&T.

It does presently appear, however, that Sprint users consume more data, and use Android, more so than customers of the other top four networks.

Though some will question the continued relevance, a long-standing study of firms in many industries, taking a look at market share, quality and profit margin, suggests that it is very hard to change firm position in an established industry. Market share patterns

Though the existence of a correlation is not necessarily a causal relationship, there is relatively significant evidence that markets develop patterns. Pareto_principle Among the more-enduring patterns is a tendency towards market concentration by a handful of leaders.

Some might argue, for that reason, that the current U.S. mobile market structure is not unusual, and might become even more concentrated over time. The informal rule of thumb might be that in any market, most of the share i(80 percent or so) is held by a small number of providers (perhaps 20 percent or fewer).

The U.S. mobile industry is more concentrated than that, but you get the point. It would be difficult under the best of conditions for Sprint Nextel to dramatically change its position in the market. But, that noted, there are some apparent differences of end user behavior that could provide something of an opening.

Some of us would not say the differences necessarily offer Sprint a way to change its market position in a dramatic way, but might offer a way to help solidify its current position. The difference is the apparent preference for Android among Sprint users, or perhaps Sprint’s willingness to bank on Android for some highly-popular devices such as the HTC Evo line.

Note recent Yankee Group surveys indicating that Sprint users are heavy users of Android devices. It is of course possible that the data reflects Sprint’s historic inability to sell the Apple iPhone, forcing Sprint to emphasize the HTC Evo as a lead offer, and thus producing the skew Yankee Group found.

One might similarly argue that Verizon Wireless faced the same problem in the days when it also could not sell the Apple iPhone. If so, it always is possible that the Android preferences illustrated by Yankee Group are a tactical, short term user demand trend that easily could change in the future.

Still, no matter what happens with the AT&T bid to buy T-Mobile USA, Sprint is going to have to work pretty hard simply to solidify some distinctive position in the market, even as a “distant third” provider, compared to Verizon Wireless and AT&T.

It does presently appear, however, that Sprint users consume more data, and use Android, more so than customers of the other top four networks.