Who wins, and who loses, as mobile apps and services, especially cloud-based apps and services, gain more traction? The “obvious” answer is that device and app providers are “winning,” while service providers “lose.” Though obviously true in the case of over-the-top voice, messaging, videoconferencing and entertainment video realms, the larger reality is more complicated.

In many cases substantial and real competition now is occurring between firms in different ecosystems, not only within single ecosystems. And, as has been the case for a couple of decades, contestants have to balance effort between protecting existing businesses and growing new lines of business.

The difference now is that many of the new revenue streams and businesses actually cross ecosystems and redefine them.

For example, mobile payment systems offered by Square, Intuit and PayPal arguably represent incremental revenue within the credit card and debit card transaction business, rather than primarily a shift of transaction volume within the business. The reason is that such services are used primarily by businesses that would not have used merchant point of sale systems in the past.

Likewise, to some extent, services that turn smart phones and tablets into merchant point of sale systems will compete with supplier of traditional merchant terminals, as well.

Enterprise cloud services might compete with packaged software suppliers, data centers or server manufacturers, for example. That would mean some amount of competition between segments of one industry.

Small business cloud services might reduce the amount of revenue earned by value-added resellers or system integrators, for example. That also is a form of intra-ecosystem competition.

Consumer cloud services, especially those related to storage, will displace some of the need for local storage, and could reduce demand for external hard drive storage and some amount of PC sales. That might be more an example of competition between ecosystems

Cloud storage might reduce need for PCs and storage devices, for example, reducing some amount of device spending and shifting that spending into software and services. So some device manufacturers might lose, while others might gain (PCs, external storage lose; mobile devices win).

By the end of 2013, consumer cloud services for accessing content will be integrated into 90 percent of all connected consumer devices, according to Gartner.

The other dynamic is that, in the case of brand-new services, such as cloud storage, there could also be winners within and between ecosystems. App providers could win, as well as hosting facilities.

Traditional entertainment video suppliers such as cable companies hope to win, even as some amount of entertainment video shifts to cloud mechanisms, even as rivals think cloud delivery will eventually displace traditional distribution mechanisms.

Likewise, cloud services could help device manufacturers as much as app providers. Certain handsets and environments, such as iOS iTunes and Apple tablets and phones, or Google Drive and Android-based devices, provide early examples. That might be an example of value and revenue shifts within the mobile ecosystem.

In other cases, such as many parts of the mobile commerce business, competition might entail substantial amounts of competition between ecosystems. Services offered by the likes of Square, Intuit and PayPal that turn a smart phone into a merchant point of service terminal represent competition between those firms and other existing payment systems, merchant POS terminal providers and emerging application provider or mobile communications service provider payment systems.

“Inside the spending envelope, market dynamics will collapse some markets while creating others that expand the captured revenue,” says Gartner managing vice president Andrew Johnson.

Providers of consumer devices, services and content must anticipate the risk of sweeping changes to their business models,” said Johnson. “The personal cloud will force technology providers not only to rethink how they approach markets, but also, more importantly, how they define markets.”

Emerging and mature markets are no longer useful form of market segmentation, Johnson argues.

Monday, May 7, 2012

Cloud Winners and Losers Will Cross Ecosystems

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, May 6, 2012

Online Video Still Needs Scale to Attract More Advertising

The online-video market represented about $1.8 billion worth of ad spending in 2011, with half of that going to just two players: Hulu (about $300 million) and YouTube (about $600 million), according to Brian Wieser, an analyst at Pivotal Research Group, and reported by Ad Age.

The online-video market represented about $1.8 billion worth of ad spending in 2011, with half of that going to just two players: Hulu (about $300 million) and YouTube (about $600 million), according to Brian Wieser, an analyst at Pivotal Research Group, and reported by Ad Age. Most of the advertising growth in online video could happen because it shifts spending from the $70 billion spent annually on TV ads in the U.S. market.

High-quality video lots of people want to watch might be necessary. But it is not sufficient for success, simply because video advertisers want large audiences.

And the simple fact is that not many providers have both attractive programming and large audiences. Subscription revenue is dominated by Netflix.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, May 4, 2012

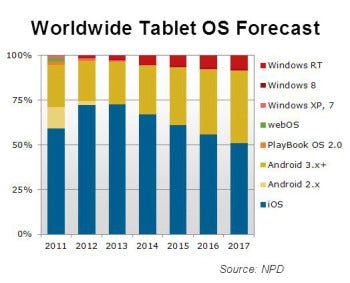

Apple Tablet Share 51% in 2017

Apple, after reaching a market share high of nearly 75 percent in 2013, will see its share decline steadily to 50.9 percent in 2017, according to forecasts by the NPD Group.

Apple, after reaching a market share high of nearly 75 percent in 2013, will see its share decline steadily to 50.9 percent in 2017, according to forecasts by the NPD Group.Shipments of tablet PCs are expected to grow from 81.6 million units in 2011 to 424.9 million units by 2017, according to NPD Group.

That forecast suggests that in 2016 more tablet PCs will be shipped than notebook PCs.

The iOS operating system has been dominant in tablet PCs, but it is expected to lose share, from 72.1 percent in 2012 to 50.9 percent in 2017, as Android increases from 22.5 percent in 2012 to 40.5 percent over the same period.

Meanwhile, share for Windows RT is also expected to grow, but from a very small base of 1.5 percent in 2012 to 7.5 percent in 2017.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscription Video Market Shrinks 1.5% in 2011

U.S. cable operators lost about 2.9 million video subscribers in 2011, shrinking the overall subscription TV market by 1.5 percent even as telcos added 1.1 million and satellite TV providers were roughly flat at 280,000 net adds, according to Nielsen data.

U.S. cable operators lost about 2.9 million video subscribers in 2011, shrinking the overall subscription TV market by 1.5 percent even as telcos added 1.1 million and satellite TV providers were roughly flat at 280,000 net adds, according to Nielsen data.The big take away is that cable TV subs fell five percent. That steady drip, drip, drip of deserting customers now is the cable analogy to telco wired voice.

Meanwhile, households with broadband and only free, over-the-air broadcast TV increased by 631,000 over the course of last year, climbing 14 percent to 5.1 million.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Why Google Has to Go "Mobile First"

Three numbers explain why Google has taken the "mobile first" approach to application development, why it has chosen to lose some money on Android and create mobile devices.

A recent survey by Strata Marketing of 1,000 advertising agencies that together process $50 billion in media buys annually found 69 percent focused their digital spend on social media.

That's more than those who focused on search (65.5 percent) and just short of online display (71.3 percent), Strata says.

Keep in mind that Google built its business on search advertising. So leading ad agencies now are placing inventory on display and social more than search.

Within social media, the majority of advertising agencies (85.1 percent) said they and their clients focused most on Facebook, 44.8 percent on YouTube, 39.1 percent on LinkedIn, 24.1 percent on Google , 9.2 percent on Foursquare and 1.1 percent on MySpace.

The YouTube figures are helpful, but the fact remains that Google has to do better in display and social advertising, as well as mobile, to remain a force in advertising. And it is mobile where the opportunity is greatest, and the market as yet unconsolidated.

A recent survey by Strata Marketing of 1,000 advertising agencies that together process $50 billion in media buys annually found 69 percent focused their digital spend on social media.

That's more than those who focused on search (65.5 percent) and just short of online display (71.3 percent), Strata says.

Keep in mind that Google built its business on search advertising. So leading ad agencies now are placing inventory on display and social more than search.

Within social media, the majority of advertising agencies (85.1 percent) said they and their clients focused most on Facebook, 44.8 percent on YouTube, 39.1 percent on LinkedIn, 24.1 percent on Google , 9.2 percent on Foursquare and 1.1 percent on MySpace.

The YouTube figures are helpful, but the fact remains that Google has to do better in display and social advertising, as well as mobile, to remain a force in advertising. And it is mobile where the opportunity is greatest, and the market as yet unconsolidated.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, May 3, 2012

Tablet Market Grew Less than Expected in First Quarter, 2012

The global tablet market did not grow as fast as analysts at International Data Corporation had expected in the first quarter of 2012. A steep drop in shipments of Android-based tablets offset a strong quarter from Apple, according to International Data Corporation Worldwide Quarterly Media Tablet and eReader Tracker.

Total worldwide media tablet shipments for the quarter reached 17.4 million units in the first quarter of 2012, about 1.2 million units below IDC's projection for the quarter.

While IDC predicted a sharp seasonal slowdown of -34 percent from the previous quarter’s record-breaking 28.2 million units, the actual decline was slightly steeper at -38.4 percent.

The total still represents a robust year-over-year growth rate of 120 percent, up from 7.9 million units in the first quarter of 2011.

Apple shipped 11.8 million iPads during the quarter, down from 15.4 million units in the fourth quarter of 2011, and grew its worldwide share from 54.7 percent in the fourth quarter of 2011 to 68 percent in the first quarter of 2012.

Amazon, which had 16.8 percent of the market on shipment of 4.8 million units, saw its share decline significantly in the first quarter to just over four percent, falling to third place as a result.

Samsung took the number-two position while Lenovo vaulted into the number four spot, followed by Barnes & Noble at number five.

Although total Android shipments were down sharply in the first quarter of 2012, companies such as Samsung and Lenovo are beginning to gain traction in the market with their latest generation of Android products. IDC expects the segment to rebound quickly as other vendors introduce new products in the second quarter and beyond.

"The worldwide tablet market is entering a new phase in the second half of 2012 that will undoubtedly reshape the competitive landscape," said Bob O'Donnell, program vice president, Clients and Displays. "While Apple will continue to sit comfortably on the top for now, the battle for the next several positions is going to be fierce. Throw in Ultrabooks, the launch of Windows 8, and a few surprise product launches, and you have all the makings of an incredible 2012 holiday shopping season."

Total worldwide media tablet shipments for the quarter reached 17.4 million units in the first quarter of 2012, about 1.2 million units below IDC's projection for the quarter.

While IDC predicted a sharp seasonal slowdown of -34 percent from the previous quarter’s record-breaking 28.2 million units, the actual decline was slightly steeper at -38.4 percent.

The total still represents a robust year-over-year growth rate of 120 percent, up from 7.9 million units in the first quarter of 2011.

Apple shipped 11.8 million iPads during the quarter, down from 15.4 million units in the fourth quarter of 2011, and grew its worldwide share from 54.7 percent in the fourth quarter of 2011 to 68 percent in the first quarter of 2012.

Amazon, which had 16.8 percent of the market on shipment of 4.8 million units, saw its share decline significantly in the first quarter to just over four percent, falling to third place as a result.

Samsung took the number-two position while Lenovo vaulted into the number four spot, followed by Barnes & Noble at number five.

Although total Android shipments were down sharply in the first quarter of 2012, companies such as Samsung and Lenovo are beginning to gain traction in the market with their latest generation of Android products. IDC expects the segment to rebound quickly as other vendors introduce new products in the second quarter and beyond.

"The worldwide tablet market is entering a new phase in the second half of 2012 that will undoubtedly reshape the competitive landscape," said Bob O'Donnell, program vice president, Clients and Displays. "While Apple will continue to sit comfortably on the top for now, the battle for the next several positions is going to be fierce. Throw in Ultrabooks, the launch of Windows 8, and a few surprise product launches, and you have all the makings of an incredible 2012 holiday shopping season."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will "Mobile First" Will Wipe Out The Big Software Makers?

"A lot of legacy players — folks that build enterprise apps on prior platforms — will end up being disrupted by new players who are better equipped to take advantage of the new mobile platform, says Kevin Spain, Emergence Partners general partner. That could even happen to Salesforce and SuccessFactors that grew up in the Web world, he believes.

The startups with the greatest potential to generate outsized returns are those creating “mobile-first enterprise applications” – those that leverage the unique capabilities of mobile devices to enable the creation of new categories of enterprise applications.

These applications are very different from mobile-enabled versions of traditional enterprise software such as Salesforce.com and Workday,Spain argues.

True “mobile-first enterprise applications” are built for mobile platforms initially or exclusively and enable a worker or business to do things that simply were not possible before the proliferation of advanced connected devices.

The point is that mobile and cloud delivery and consumption of applications might have disruptive impact on industry suppliers.

The startups with the greatest potential to generate outsized returns are those creating “mobile-first enterprise applications” – those that leverage the unique capabilities of mobile devices to enable the creation of new categories of enterprise applications.

These applications are very different from mobile-enabled versions of traditional enterprise software such as Salesforce.com and Workday,Spain argues.

True “mobile-first enterprise applications” are built for mobile platforms initially or exclusively and enable a worker or business to do things that simply were not possible before the proliferation of advanced connected devices.

The point is that mobile and cloud delivery and consumption of applications might have disruptive impact on industry suppliers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Samsung Galaxy S III the Challenger to Apple iPhone?

Virtually every smart phone supplier aspires to compete head to head with the Apple iPhone. You can make your own assessment about how well all those efforts have fared.

But at least some observers believe Samsung might be in position to do so. That is based in part on the profitability of Samsung's smart phone business, as well as sales volume.

Samsung has displaced longtime mobile device market share leader Nokia as the world's top mobile phone vendor.

According to International Data Corporation, vendors shipped 398.4 million units in the first quarter of 2012 compared to 404.3 million units in the first quarter of 2011.

Samsung's ascension to the market's top spot is largely a reflection of its gains in the smart phone market over the past two years, said Kevin Restivo, IDC senior research analyst.

Apple and Samsung also accounted for a stunning 95 percent of the handset industry's profits during the fourth quarter, according to a study by Canaccord Genuity.

The issue now is whether the Galaxy S III can legitimately compete head to head with the iPhone.

But at least some observers believe Samsung might be in position to do so. That is based in part on the profitability of Samsung's smart phone business, as well as sales volume.

Samsung has displaced longtime mobile device market share leader Nokia as the world's top mobile phone vendor.

According to International Data Corporation, vendors shipped 398.4 million units in the first quarter of 2012 compared to 404.3 million units in the first quarter of 2011.

Samsung's ascension to the market's top spot is largely a reflection of its gains in the smart phone market over the past two years, said Kevin Restivo, IDC senior research analyst.

Apple and Samsung also accounted for a stunning 95 percent of the handset industry's profits during the fourth quarter, according to a study by Canaccord Genuity.

The issue now is whether the Galaxy S III can legitimately compete head to head with the iPhone.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Is Mobile VoIP More Reliable than Mobile Service Provider Voice?

Most observers would agree that dropped calls are a driver of customer churn. The perhaps-unknown question is whether mobile VoIP offered by over-the-top providers is more reliable than carrier-provided voice.

Ask yourself whether you ever have seen a study comparing mobile VoIP dropped call rates to mobile carrier voice dropped call rates. It's difficult to impossible.

Some 39 percent of mobile users surveyed on behalf of Rebtel experienced more than five dropped calls per month. Perhaps the implication is that over-the-top mobile VoIP can be as reliable, if not more reliable, than carrier-supplied voice. But it is hard to test the assertion.

Do you believe that mobile over-the-top VoIP will lead to fewer dropped calls than a mobile service provider's own voice service?

The general rule of thumb is that over-the-top VoIP, in general, is less reliable than landline voice, but good enough to match mobile call quality and reliability. One might argue that service provider or enterprise IP telephony are as reliable as landline voice, though even that claim is hard to test.

The study also showed that having a clear call connection is very important to 89 percent of respondents, with 84 percent of those claiming they are at least somewhat likely to switch smart phones as a result of poor quality.

About 78 percent said they would be likely to switch carriers due to poor network performance, according to Rebtel.

Dropped calls raise the likelihood of customer churn. What is difficult to determine is whether mobile VoIP, over the top, actually provides reliability that is better than what most consumers experience with mobile voice. Try to find any studies on that particular subject. It is virtually impossible.

Ask yourself whether you ever have seen a study comparing mobile VoIP dropped call rates to mobile carrier voice dropped call rates. It's difficult to impossible.

Some 39 percent of mobile users surveyed on behalf of Rebtel experienced more than five dropped calls per month. Perhaps the implication is that over-the-top mobile VoIP can be as reliable, if not more reliable, than carrier-supplied voice. But it is hard to test the assertion.

Do you believe that mobile over-the-top VoIP will lead to fewer dropped calls than a mobile service provider's own voice service?

The general rule of thumb is that over-the-top VoIP, in general, is less reliable than landline voice, but good enough to match mobile call quality and reliability. One might argue that service provider or enterprise IP telephony are as reliable as landline voice, though even that claim is hard to test.

The study also showed that having a clear call connection is very important to 89 percent of respondents, with 84 percent of those claiming they are at least somewhat likely to switch smart phones as a result of poor quality.

About 78 percent said they would be likely to switch carriers due to poor network performance, according to Rebtel.

Dropped calls raise the likelihood of customer churn. What is difficult to determine is whether mobile VoIP, over the top, actually provides reliability that is better than what most consumers experience with mobile voice. Try to find any studies on that particular subject. It is virtually impossible.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

20% of Americans, 34% of Smart Phone Owners Purchased Using a Mobile Phone in 2011

A new survey conducted by Harris Interactive on behalf of Placecast claims that 20 percent of adult mobile phone owners in the U.S. made an online purchase with their phone last year.

Those with smartphones were more likely to make purchases on their phones.

Thirty-four percent of smart phone owners made a purchase on their phone last year, compared to 11 percent of those with feature phones. Thirty-eight percent of the respondents to the study said that making a purchase on their mobile phone was at least somewhat important to them.

Those with smartphones were more likely to make purchases on their phones.

Thirty-four percent of smart phone owners made a purchase on their phone last year, compared to 11 percent of those with feature phones. Thirty-eight percent of the respondents to the study said that making a purchase on their mobile phone was at least somewhat important to them.

Overall interest in using phones for purchases has grown by eight percentage points in the past two years, with 38 percent of all mobile phone owners saying it is at least somewhat important.

Some 59 percent of smart phone owners surveyed say it is at least somewhat important to be able to make a purchase on their device.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

U.S. TV Viewers Using More Screens

The average American watches nearly five hours of video

each day, 98 percent of which they watch on a traditional

TV set, according to Nielsen.

After several years of consistent year-over-year growth, traditional TV viewing declined one half of one percent or roughly 46 minutes per month. Nielsen suggests that dip could be explained by any number of drivers other than a shift in viewing habits.

As more homes adopt DVRs and move to greater use of time-shifted viewing, time-shifted TV growth has offset the bulk of live TV declines. Other potential factors include time spent using game consoles, tablets and other emerging devices, or even short-term weather, Nielsen says.

Still, in the fall of 2011 there was a slight decline in the number of TV homes in the U.S. market. This shift is prompting an important conversation around the definition of a “TV household” and a “TV viewer,” as some homes not using "TV" might be watching video on tablets, PCs and smart phones.

Some 33.5 million mobile phone owners now watch video on their phones—an increase of 35.7 percent year over year.

After several years of consistent year-over-year growth, traditional TV viewing declined one half of one percent or roughly 46 minutes per month. Nielsen suggests that dip could be explained by any number of drivers other than a shift in viewing habits.

As more homes adopt DVRs and move to greater use of time-shifted viewing, time-shifted TV growth has offset the bulk of live TV declines. Other potential factors include time spent using game consoles, tablets and other emerging devices, or even short-term weather, Nielsen says.

Still, in the fall of 2011 there was a slight decline in the number of TV homes in the U.S. market. This shift is prompting an important conversation around the definition of a “TV household” and a “TV viewer,” as some homes not using "TV" might be watching video on tablets, PCs and smart phones.

Some 33.5 million mobile phone owners now watch video on their phones—an increase of 35.7 percent year over year.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Greater Reliance on Wholesale in Telecom Future?

It seems likely that most tier-one service providers, especially in the mobile end of the business, will be relying on more "wholesale" services in the future. To some extent, this already is the case, as when a facilities-based service provider leases capacity and features to a mobile virtual network operator.

Likewise, enterprise customers have for many decades created their own voice services using their own phone systems, while buying bulk access from service providers only to carry and terminate those derived services.

Telecom service providers likewise have sold bulk capacity and features to third parties that create enterprise services for retail sale.

But there now is much talk of ways service providers can increase the volume of services and access sold to third party business partners. Content delivery networks provide one example. Cloud computing services provide other examples.

But sale of network features and "big data" features likely will be more important as well. The general notion is that application providers could be encouraged to purchase network functions or features in a bulk or wholesale capacity, to enhance or create new application experiences. Advertising or content firms are said to be likely buyers.

There might be quite a lot more of that sort of activity in the future, representing a shift to more business-to-business sales than traditional business-to-end-user sales.

Wholesale strategies could become more radical. A few service providers might opt to become wholesale-only capacity providers, though that is likely to remain a fairly unusual strategy for any tier-one service provider.

But some believe the agency agreements between Verizon and Comcast, Time Warner Telecom and Cox Communications, allowing the cable companies to sell Verizon products, and Verizon to sell cable products, could lead the cable operators to become wholesale providers to Verizon, while Verizon becomes a wholesale supplier to the cable firms.

Likewise, enterprise customers have for many decades created their own voice services using their own phone systems, while buying bulk access from service providers only to carry and terminate those derived services.

Telecom service providers likewise have sold bulk capacity and features to third parties that create enterprise services for retail sale.

But there now is much talk of ways service providers can increase the volume of services and access sold to third party business partners. Content delivery networks provide one example. Cloud computing services provide other examples.

But sale of network features and "big data" features likely will be more important as well. The general notion is that application providers could be encouraged to purchase network functions or features in a bulk or wholesale capacity, to enhance or create new application experiences. Advertising or content firms are said to be likely buyers.

There might be quite a lot more of that sort of activity in the future, representing a shift to more business-to-business sales than traditional business-to-end-user sales.

Wholesale strategies could become more radical. A few service providers might opt to become wholesale-only capacity providers, though that is likely to remain a fairly unusual strategy for any tier-one service provider.

But some believe the agency agreements between Verizon and Comcast, Time Warner Telecom and Cox Communications, allowing the cable companies to sell Verizon products, and Verizon to sell cable products, could lead the cable operators to become wholesale providers to Verizon, while Verizon becomes a wholesale supplier to the cable firms.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will Apple, Google, Facebook, Amazon or Microsoft Become Mobile Service Providers?

Apple will provide wireless service directly to its iPad and iPhone customers, argues consultant Whitey Bluestein. In his hypothetical scenario, Apple first will sell data packages bundled with iPads. Then it will sell data and international roaming plans to iPhone customers through the iTunes Store, Bluestein argues.

Over time, Apple will strike wholesale deals with several mobile operators so that Apple can provide wireless service directly to its customers, as Apple Mobile, Bluestein predicts. As “crazy” as that might sound, it might be a fairly common tack taken by any number of device, service or application providers, eventually.

In fact, it fits well with the general thinking that, over time, mobile and fixed network service providers will increasingly want to sell services to third-party business partners as well as end users.

Other potential moves by a number of leading application or software providers show the ways business advantage is shifting in the mobility business.

Microsoft's recent investment in the new company that will own the Nook tablet and content business shows the growing importance content, advertising and commerce operations are assuming for device and application suppliers, for example.

Some believe the "Four Horsemen" of the Internet include Facebook, Apple, Google and Amazon. Others might say the list actually is "Five Horsemen" and include Microsoft. Either way, the notion is that handful of firms have the ability, at least in principle, to create and own a complete and walled-off ecosystem in which consumers use a single company’s hardware, operating system and storefront to search online, buy apps and purchase digital media and physical products.

What remains less clear is the importance of bundling "access" with those other device, content, commerce and advertising capabilities, though. In principle, the separation of applications from access is quite helpful for any app provider.

That remains less clear. But one approach that might have clear advantages is the ability to create mobile access services that are optimized for media consumption. In other words, the aim might be to optimize the streaming media and gaming experience, not provide a "better" voice or messaging experience.

Over time, Apple will strike wholesale deals with several mobile operators so that Apple can provide wireless service directly to its customers, as Apple Mobile, Bluestein predicts. As “crazy” as that might sound, it might be a fairly common tack taken by any number of device, service or application providers, eventually.

In fact, it fits well with the general thinking that, over time, mobile and fixed network service providers will increasingly want to sell services to third-party business partners as well as end users.

Other potential moves by a number of leading application or software providers show the ways business advantage is shifting in the mobility business.

Microsoft's recent investment in the new company that will own the Nook tablet and content business shows the growing importance content, advertising and commerce operations are assuming for device and application suppliers, for example.

Some believe the "Four Horsemen" of the Internet include Facebook, Apple, Google and Amazon. Others might say the list actually is "Five Horsemen" and include Microsoft. Either way, the notion is that handful of firms have the ability, at least in principle, to create and own a complete and walled-off ecosystem in which consumers use a single company’s hardware, operating system and storefront to search online, buy apps and purchase digital media and physical products.

What remains less clear is the importance of bundling "access" with those other device, content, commerce and advertising capabilities, though. In principle, the separation of applications from access is quite helpful for any app provider.

On the other hand, are there ways app providers can create a better end user experience by bundling apps, devices and connectivity?

That remains less clear. But one approach that might have clear advantages is the ability to create mobile access services that are optimized for media consumption. In other words, the aim might be to optimize the streaming media and gaming experience, not provide a "better" voice or messaging experience.

That could take the form of a branded content delivery service distinct from general-purpose Internet apps, voice or messaging services. What might be bundled, in other words, is a branded experience enhanced by CDN capabilities. In each ecosystem, content delivered as part of a content app or service might essentially be a "private network" experience taking advantage of available optimization techniques.

Think of a content virtual private network and you get the idea. That sort of optimized access might make more sense than any of the leading ecosystem providers becoming actual general-purpose mobile service providers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Commerce and Shopping Behavior Quite Common

According to a survey conducted by Nielsen, 79 percent of U.S. smart phone and tablet owners have used their mobile devices for shopping-related activities.

Smart phones are used more often than tablets for activities on-the-go, as you would expect. By some studies, up to 95 percent of tablet usage occurs indoors, rather than in a mobile context.

About 73 percent of respondents polled by Nielsen used their smart phone to locate a store, compared to about 42 percent using a tablet to search for a store.

Some 42 percent of respondents used a mobile device to create a shopping list while shopping. About 16 percent of tablet users reported they did so.

Some 36 percent of respondents said they redeemed a mobile coupon on their smart phone, compared to 11 percent of tablet owners.

Some 42 percent of tablet owners have “used their device to purchase an item,” compared to 29 percent of smart phone owners.

Both smart phones and tablets have been used to “research an item before purchase.” About 66 percent of tablet owners and 57 percent of smart phone owners reported doing so.

Some 27 percent of smart phone owners and 28 percent of tablet owners say they have used their devices to make a payment.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple, Google, Amazon Microsoft: Who Wins the Ecosystem War?

Microsoft's recent investment in the new company that will own the Nook tablet and content business illustrates a couple of important strategic shifts now happening in the mobile device and application markets. The biggest shift is the growing importance content, advertising and commerce operations are assuming for device and application suppliers.

Among the secondary issues is a new take on "open" versus "closed" approaches to software development have been a live issue for decades. These days, with the emergence of content and commerce as key elements of device and application strategy, the questions are taking new shape.

Some believe the "Four Horsemen" of the Internet include Facebook, Apple, Google and Amazon. Others might say the list actually is "Five Horsemen" and include Microsoft. Either way, the notion is that handful of firms have the ability, at least in principle, to create and own a complete and walled-off ecosystem in which consumers use a single company’s hardware, operating system and storefront to search online, buy apps and purchase digital media and physical products.

If that proves to be true then a couple of predictions are easy to make. Facebook and Amazon will produce their own smart phones. Facebook might also have to produce a tablet. Apple will have to create a mobile payment service, as will Microsoft.

Google and Facebook will have to get more share of the e-commerce and mobile commerce transactions, and all will deepen the activities they now already support around mobile advertising, promotion and loyalty.

Last week, yet another rumor surfaced that Facebook is getting closer to releasing its own branded smartphone, an obvious attempt at owning a stack component (hardware) that’s currently missing from its line-up, Wired reports. Rumors about an Amazon smart phone have circulated for a couple of years, on and off, as well.

“A smartphone would be a logical next step for Amazon,” ABI Research Analyst Aapo Markkanen says.

Either of those moves, plus an eventual move to create a Facebook tablet, illustrate the changing role of devices and connectivity in the mobile space. Traditionally, mobile phones simply were devices carriers had to provide to sell voice and messaging services.

These days, matters are more complex. In addition to communications, hot consumer devices frequently are used for content consumption. That means smart phones are more important to application providers as platforms for selling content and advertising.

Everyone expects a mobile device to handle voice and texting. Beyond that, more users expect the ability to consume content and conduct transactions. That changes the strategic importance of being a device manufacturer.

For mobile service providers, phones have been a sort of prop to produce revenue indirectly, in the form of service subscriptions. But that also now is increasingly true for application providers.

For Apple, which merchandises all sorts of content to sell devices, the tight bundling of content and commerce is a major reason it can sell so many devices. That also is true for some other mobile device manufacturers. But not for all.

For Google and Amazon, devices are a way to sell more advertising, content and merchandise. Microsoft has a slightly different take, as it always has preferred to sell operating systems to partners who make phones. But Microsoft has to succeed in mobile operating systems to profit from the device ecosystem that supports the advertising, commerce and content businesses.

Such thinking is not terribly new. Consumer electronics manufacturers have for decades understood that content was important for the devices business. Sony is probably the best example of that. Apple arguably was the first consumer devices firm to really achieve that integration, with its iPod and iTunes.

These days, gaining the ability to lock consumer into a particular content ecosystem is the reason producing devices matters.

Among the secondary issues is a new take on "open" versus "closed" approaches to software development have been a live issue for decades. These days, with the emergence of content and commerce as key elements of device and application strategy, the questions are taking new shape.

Some believe the "Four Horsemen" of the Internet include Facebook, Apple, Google and Amazon. Others might say the list actually is "Five Horsemen" and include Microsoft. Either way, the notion is that handful of firms have the ability, at least in principle, to create and own a complete and walled-off ecosystem in which consumers use a single company’s hardware, operating system and storefront to search online, buy apps and purchase digital media and physical products.

If that proves to be true then a couple of predictions are easy to make. Facebook and Amazon will produce their own smart phones. Facebook might also have to produce a tablet. Apple will have to create a mobile payment service, as will Microsoft.

Google and Facebook will have to get more share of the e-commerce and mobile commerce transactions, and all will deepen the activities they now already support around mobile advertising, promotion and loyalty.

Last week, yet another rumor surfaced that Facebook is getting closer to releasing its own branded smartphone, an obvious attempt at owning a stack component (hardware) that’s currently missing from its line-up, Wired reports. Rumors about an Amazon smart phone have circulated for a couple of years, on and off, as well.

“A smartphone would be a logical next step for Amazon,” ABI Research Analyst Aapo Markkanen says.

Either of those moves, plus an eventual move to create a Facebook tablet, illustrate the changing role of devices and connectivity in the mobile space. Traditionally, mobile phones simply were devices carriers had to provide to sell voice and messaging services.

These days, matters are more complex. In addition to communications, hot consumer devices frequently are used for content consumption. That means smart phones are more important to application providers as platforms for selling content and advertising.

Everyone expects a mobile device to handle voice and texting. Beyond that, more users expect the ability to consume content and conduct transactions. That changes the strategic importance of being a device manufacturer.

For mobile service providers, phones have been a sort of prop to produce revenue indirectly, in the form of service subscriptions. But that also now is increasingly true for application providers.

For Apple, which merchandises all sorts of content to sell devices, the tight bundling of content and commerce is a major reason it can sell so many devices. That also is true for some other mobile device manufacturers. But not for all.

For Google and Amazon, devices are a way to sell more advertising, content and merchandise. Microsoft has a slightly different take, as it always has preferred to sell operating systems to partners who make phones. But Microsoft has to succeed in mobile operating systems to profit from the device ecosystem that supports the advertising, commerce and content businesses.

Such thinking is not terribly new. Consumer electronics manufacturers have for decades understood that content was important for the devices business. Sony is probably the best example of that. Apple arguably was the first consumer devices firm to really achieve that integration, with its iPod and iTunes.

These days, gaining the ability to lock consumer into a particular content ecosystem is the reason producing devices matters.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...