U.S. broadband prices are not the lowest in the world, by any means, and some worry that neither speeds nor prices will improve much, in the future. That inevitably will lead to calls to “do something” about national broadband policy.

There are a couple issues there. The first is whether, under present fiscal circumstances, the federal government and U.S. States can do much of anything about direct investment of their own. Like it or not, the answer is that policy frameworks can be adjusted, but that there is precious little “investment” possible, from government quarters.

The more contentious issue is likely around what incentives properly can be provided for cable operators and telcos to voluntary boost their own investment, and how much those incentives matter, where it comes to investment decisions.

Some might say that almost no amount of incentives would convince a rational executive to invest “too much” in a business that cannot return a market rate of return, compared to all other alternatives that promise a higher return. It is not easy to balance end user welfare and industry incentives, under conditions of great uncertainty.

A new FCC study released in July 2012 does show that progress is being made. As always, the issue is whether the progress is fast enough.

Whether Google Fiber in Kansas City, Kan. and Kansas City, Mo. will have the intended effect of spurring more investment by telcos and cable operators remains to be seen. So some might say handwringing about the state of progress in the U.S. broadband market are overblown.

That is not to say issues exist. There clearly is an argument to be made that most telcos cannot outline a solid business rationale for aggressive fiber to the home upgrades, in many, if not most cases. In part the problem is that financial return is questionable. In other cases the argument is simply that alternative capital investments in mobile assets will drive a higher return.

Also, unlike the situation in many other markets, a powerful, facilities-based competitor with arguably better cost structure (both in terms of capital requirements for bandwidth upgrades, and workforce cost issues), competes head to head in virtually every market, with two powerful satellite contenders that reduce the potential gain from offering video entertainment services, a key element of the telco business case for deploying fiber to the home.

As far as the retail pricing, where the U.S. never ranks among the “best” providers, measured in terms of price per megabyte of access speed, one problem is simply that costs are higher in the U.S. market.

Population density might be the single most important factor determining the cost of any fiber to home network build. A related issue is average “loop length,” a metric that is roughly related to population density.

U.S. service providers have to supply service over much longer average loops than service providers in Europe, or in many “city states” that feature high-density housing. Basically, retail cost everywhere is related rather directly to network investment cost.

So Google Fiber’s $70 a month benchmark for symmetrical 1-Gbps access, along with a similar offering by Sonic.net, probably are best viewed as “stretch goals” for most U.S. telcos, arguably less a stretch for cable operators, and out of reach, for technical reasons, by satellite broadband providers.

Perhaps progress in the U.S. broadband market is not “the best of all possible worlds.” But options simply are not unlimited, or investment drivers very easy.

Friday, July 27, 2012

Is "National Broadband Policy" Needed, or in Need of Adjustment?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Notice What is Missing on Google Fiber

Virtually unmentioned in discussions about Google Fiber as it is being deployed in Kansas City, Kan. and Kansas City, Mo. is that voice is available as part of the service. That’s largely because the really unique aspect is the 1-Gbps broadband access.

Even the video service is a relatively basic offer lacking many channels many consumers will prefer.

But voice is less than an afterthought. it’s just something users can supply themselves, using over the top applications such as Google Talk.

That tells you much about potential future models for at least some access providers, if Google Fiber proves it can make an actual profit, offering 1-Gbps symmetrical Internet access and entertainment TV, on its own fiber to the home network.

Broadband access will be the foundation. Google Fiber believes video entertainment is a crucial service to drive higher average revenue per user. Sonic.net believes Internet access and voice is the more logical bundle for it to offer.

In either case, the real top draw is Internet access at 1 Gbps for $70 a month. Basically, voice or video are complementary services.

Cable operators and telcos, with higher operating costs, might always feel it necessary to offer the triple play as a way of creating enough gross revenue to support their services. But some service providers might try and optimize their offerings around broadband access, using either voice or video as a complement, but not both.

Even the video service is a relatively basic offer lacking many channels many consumers will prefer.

But voice is less than an afterthought. it’s just something users can supply themselves, using over the top applications such as Google Talk.

That tells you much about potential future models for at least some access providers, if Google Fiber proves it can make an actual profit, offering 1-Gbps symmetrical Internet access and entertainment TV, on its own fiber to the home network.

Broadband access will be the foundation. Google Fiber believes video entertainment is a crucial service to drive higher average revenue per user. Sonic.net believes Internet access and voice is the more logical bundle for it to offer.

In either case, the real top draw is Internet access at 1 Gbps for $70 a month. Basically, voice or video are complementary services.

Cable operators and telcos, with higher operating costs, might always feel it necessary to offer the triple play as a way of creating enough gross revenue to support their services. But some service providers might try and optimize their offerings around broadband access, using either voice or video as a complement, but not both.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will Google Fiber Economics Work?

“There’s no sense selling a product at a loss,” says Google CFO Patrick Pichette. “But it’s not only about profits, it’s about changing the access costs,” Pichette also has said.

Assuming you believe that Google is serious about "making money" selling symmetrical 1-Gbps connections at $70 a month, and video service starting at $50 a month, the issue is what Google can do that cable operators or telcos have not been able to do to get capital investment and construction and other costs down to a point where retail prices at such levels still turn a profit.

Sonic.net might agree that it is possible, under some circumstances, to offer very high speed broadband access at shocking prices. Sonic.net already offers consumers 1-Gbps service for $70 a month. But Sonic.net also notes that its construction cost is about $500 for each home passed. And since Sonic.net gets about 33 percent take rates, the effective network cost for each customers is about $1500.

If Google gets similar economics for the network, and few observers are likely to think Google has found some magical way to avoid the actual costs of installing cabling, and also gets about 33 percent penetration, it should be possible to make money at $70 a month for a 1-Gbps service.

Of course, operating costs will have to be kept in check as well, and that is an area of potential friction for Google, which arguably will not have the infrastructure a service provider might normally be expected to support.

On the other hand, significant portion of the cost of delivering service is not the actual backbone network, but the drop network and then customer premises equipment. Google's "$300 connection fee" suggests the cost of activating a drop is that amount.

Then there is the cost of the customer premises equipment. Some might argue Google has a cost advantage in that area. To be sure, building custom boxes, in low volume, is not generally the key to low costs.

But perhaps Google has built a really simple box, using its new Motorola expertise, that dramatically lowers CPE investment. On the other hand, some observers will note that Google actually supplies three separate boxes, plus a Nexus 7 tablet, for a customer buying the 1-Gbps plus video entertainment service.

Some will argue it is hard to see significant cost savings when using a discrete approach such as Google is employing, but perhaps that saves significant money.

Others might argue that Google will save on marketing costs or other overhead, and that might be a more-reasonable argument. Sonic.net probably does not spend as much money on marketing as Comcast, Time Warner Cable or Verizon does. Google might be able to do as well as Sonic.net

Assuming you believe that Google is serious about "making money" selling symmetrical 1-Gbps connections at $70 a month, and video service starting at $50 a month, the issue is what Google can do that cable operators or telcos have not been able to do to get capital investment and construction and other costs down to a point where retail prices at such levels still turn a profit.

Sonic.net might agree that it is possible, under some circumstances, to offer very high speed broadband access at shocking prices. Sonic.net already offers consumers 1-Gbps service for $70 a month. But Sonic.net also notes that its construction cost is about $500 for each home passed. And since Sonic.net gets about 33 percent take rates, the effective network cost for each customers is about $1500.

If Google gets similar economics for the network, and few observers are likely to think Google has found some magical way to avoid the actual costs of installing cabling, and also gets about 33 percent penetration, it should be possible to make money at $70 a month for a 1-Gbps service.

Of course, operating costs will have to be kept in check as well, and that is an area of potential friction for Google, which arguably will not have the infrastructure a service provider might normally be expected to support.

On the other hand, significant portion of the cost of delivering service is not the actual backbone network, but the drop network and then customer premises equipment. Google's "$300 connection fee" suggests the cost of activating a drop is that amount.

Then there is the cost of the customer premises equipment. Some might argue Google has a cost advantage in that area. To be sure, building custom boxes, in low volume, is not generally the key to low costs.

But perhaps Google has built a really simple box, using its new Motorola expertise, that dramatically lowers CPE investment. On the other hand, some observers will note that Google actually supplies three separate boxes, plus a Nexus 7 tablet, for a customer buying the 1-Gbps plus video entertainment service.

Some will argue it is hard to see significant cost savings when using a discrete approach such as Google is employing, but perhaps that saves significant money.

Others might argue that Google will save on marketing costs or other overhead, and that might be a more-reasonable argument. Sonic.net probably does not spend as much money on marketing as Comcast, Time Warner Cable or Verizon does. Google might be able to do as well as Sonic.net

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Device Sales Hit by Economy, Globally

As much as people love their mobile devices, economic stringency is having an effect.But some would say tougher service provider policies, such as ending device subsidies or making upgrades at affordable prices more difficult, also are having an effect,

Oddly enough, some service providers have concluded that they do better, financially, by slowing the rate of smart phone adoptions. Others have concluded they simply need to shift demand to smart phone brands that provide more favorable operator economics.

The global figures also suggest that current demand now is driven by smart phones, rather than feature phones that traditionally have represented the sales volume.

Global mobile phone shipments grew a modest one percent annually to reach 362 million units in the second quarter of 2012, Strategy Analytics reports.

Samsung was the top performer, shipping 93.0 million handsets worldwide and capturing a record 26 percent marketshare to solidify its first-place lead.

Nokia’s global handset shipments continued to decline, at a negative five percent annually, reaching 83.7 million units in Q2 2012.

Apple shipped 26 million handsets worldwide in the second quarter of 2012.

Samsung was the star performer during the quarter, capturing a record 26 percent marketshare.

Other findings from the research include:

Oddly enough, some service providers have concluded that they do better, financially, by slowing the rate of smart phone adoptions. Others have concluded they simply need to shift demand to smart phone brands that provide more favorable operator economics.

The global figures also suggest that current demand now is driven by smart phones, rather than feature phones that traditionally have represented the sales volume.

Global mobile phone shipments grew a modest one percent annually to reach 362 million units in the second quarter of 2012, Strategy Analytics reports.

Samsung was the top performer, shipping 93.0 million handsets worldwide and capturing a record 26 percent marketshare to solidify its first-place lead.

Nokia’s global handset shipments continued to decline, at a negative five percent annually, reaching 83.7 million units in Q2 2012.

Apple shipped 26 million handsets worldwide in the second quarter of 2012.

Samsung was the star performer during the quarter, capturing a record 26 percent marketshare.

Other findings from the research include:

- ZTE captured 5 percent of global handset shipments as shipments slipped minus 16 percent annually, partly because of weakened demand in major markets of Western Europe and China;

- LG’s shipments nearly halved year-over-year to 13.1 million units, as its feature phone volumes continued to slip. However, its global smartphone shipments encouragingly improved on a sequential basis.

Global Handset Vendor Shipments and Market Share in Q2 2012

| Global Handset Shipments (Millions of Units) | Q2 ’11 | Q2 '12 |

| Samsung | 74.0 | 93.0 |

| Nokia | 88.5 | 83.7 |

| Apple | 20.3 | 26.0 |

| ZTE | 19.6 | 16.5 |

| LG | 24.8 | 13.1 |

| Others | 130.8 | 129.7 |

| Total | 358.0 | 362.0 |

| Global Handset Vendor Marketshare % | Q2 ’11 | Q2 '12 |

| Samsung | 20.7% | 25.7% |

| Nokia | 24.7% | 23.1% |

| Apple | 5.7% | 7.2% |

| ZTE | 5.5% | 4.6% |

| LG | 6.9% | 3.6% |

| Others | 36.5% | 35.8% |

| Total | 100.0% | 100.0% |

| Global Handset Shipments Growth Year-over-Year % | 11.9% | 1.1% |

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, July 26, 2012

Apple Still Leads in Enterprise

While Android smartphone usage within the enterprise nearly doubled during the second quarter of 2012, iOS continues to be the dominant smartphone platform, led primarily by the iPhone 4S, a Good Technology study suggests.

On average, the two most recently released iPhones and iPads drove the majority of activations between April 1 and June 30, 2012. The iPhone 4S was the top device, driving nearly twice as many activations as any other smartphone, with 30.8 percent of activations for the quarter.

Apple iOS device activations still account for more than twice the number of Android activations in the enterprise when it comes to overall platform activations. iOS accounted for 70.8 percent, Android was 28.3 percent and Windows Phone 7 was 0.9 percent.

Apple iOS device activations still account for more than twice the number of Android activations in the enterprise when it comes to overall platform activations. iOS accounted for 70.8 percent, Android was 28.3 percent and Windows Phone 7 was 0.9 percent.

Corporate use of Android smart phones nearly doubled quarter over quarter, capturing 36.9 percent of total activations, led by the popular Samsung Galaxy SII, which ranked fifth in “Top 10” devices this quarter at 4.6 percent.

Other “Top 10” Android devices include Samsung’s Galaxy SII and the Motorola Droid Razr which claimed the fifth and sixth spots. Both of these Android smartphones outpaced the original iPad and iPhone 3S, which ranked seventh and eighth, down slightly from their respective fifth and sixth place spots last quarter.

Additionally, while tablet adoption by the enterprise continued to grow—dominated by the iPad, which accounted for 94.5 percent overall tablet activations— smart phone usage still outnumbered tablet usage by three to one, accounting for 73 percent of total mobile device activations.

Android saw another increase in this category for the quarter, as Android tablets captured 5.5 percent of total tablet activations, up from 2.7 percent last quarter.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

U.S., Korea, Japan Represent 90% of LTE Subs

Operators in the United States, South Korea and Japan have established themselves as the early leaders in Long Term Evolution, jointly accounting for almost 90 percent of the world’s LTE connections in the second quarter of 2012, according to Wireless Intelligence.

Operators in the United States, South Korea and Japan have established themselves as the early leaders in Long Term Evolution, jointly accounting for almost 90 percent of the world’s LTE connections in the second quarter of 2012, according to Wireless Intelligence.It is estimated that global LTE connections topped 27 million at the end of the second quarter, up from around 10 million at the end of 2011.

U.S. operators accounted for 47 percent of the total, followed by South Korea (27 percent) and Japan (13 percent).

Wireless Intelligence estimates that the number of global markets with live LTE networks has grown from 30 at the end of 2011 to over 40 six months later, with LTE launching for the first time in 2012 in major markets such as India and Russia.

The world’s largest LTE operator is currently the US market leader, Verizon Wireless. The U.S. number-one first launched its next-generation network at the end of 2010 and it is now live in 337 regional markets, covering nearly 75 percent of the US population (233 million POPs).

Last week, Verizon announced that it had sold 3.2 million LTE devices in Q2, bringing its cumulative total past 10 million, and representing over 12 percent of retail postpaid connections. Its major rivals are playing catch-up.

AT&T launched LTE in September last year and is currently live in 47 markets, with plans to complete rollout by the end of next year. It claims its 4G-branded network (HSPA+/LTE) covers 260 million of the population; it had a third of its postpaid smartphone subscribers (2.5 million) using its '4G' devices by Q2.

Number-three US operator Sprint switched on its first LTE networks in 15 markets earlier this month, while several US regional operators have also launched, including the two largest, MetroPCS and Leap Wireless.

Meanwhile, the South Korean market leader SK Telecom announced this week that it had surpassed 4 million LTE subscribers, adding the last million in just 44 days (it hit the 3 million mark on 6 June), with an average of 41,000 LTE users signing up per day in July.

It is targeting 7 million in total by year-end. The operator also claims to be the first in the world to launch multi-carrier LTE, planning to roll-out the technology across Seoul and six other metropolitan cities this year.

Japan’s largest operator, NTT Docomo, launched LTE in December 2010 and also this week announced it had hit the 4 million milestone. The Xi-branded network passed the 4 million subscriber mark on 22 July, around one and a half months after reaching 3 million.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Google Fiber Offers "Free" 5 Mbps Broadband Access in Kansas City

Google Fiber, which is launching service in Kansas City, Kan. and Kansas City, Mo., will offer consumers a "free" broadband access services, offering downstream speeds up to 5 Mbps, with a 1Mbps upload speed, with free service guaranteed for at least seven years.

Google Fiber, which is launching service in Kansas City, Kan. and Kansas City, Mo., will offer consumers a "free" broadband access services, offering downstream speeds up to 5 Mbps, with a 1Mbps upload speed, with free service guaranteed for at least seven years.Users have to pay a one-time $300 "construction fee," optionally payable in 12 monthly payments of $25), plus applicable taxes and fees.

The "standard" symmetrical 1 Gbps upload and download service, with no data caps, requires a one-year contract and costs $70 a month, plus taxes and fees.

The "entertainment television and 1-Gbps service costs $120 a month, and includes a number of standard video channels. The nominal pricing of the video service is $50 a month. A number of the leading networks, including ESPN, Disney and Fox channels are unavailable at that price.

But Google Fiber at launch will be a "beta" in some ways, so programming line-ups might change, over time.

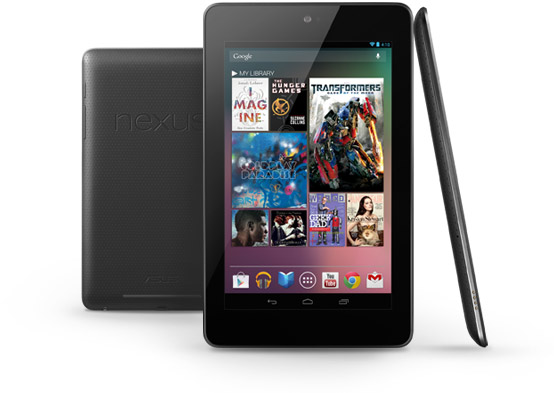

The standard package also includes a free Nexus 7 tablet, though, at least in part because the tablet provides remote control features, as well as the ability to eamlessly watch on your tablet in other rooms of a customer's house.

The standard package also includes a free Nexus 7 tablet, though, at least in part because the tablet provides remote control features, as well as the ability to eamlessly watch on your tablet in other rooms of a customer's house.Of course, users who want broadband access and television will have three different boxes, one for broadband, one for TV decoding, and a third to provide digital video recorder functions.

There are some ways in which the Google video service offers advantages. There is no separate box or fee for HDTV viewing, for example. Many service providers charge extra for DVR functionality as well. Google video service does not have those add-on fees.

- 3Net

- A&;E

- Action Weather

- Animal Planet

- Antenna TV

- Bandamax

- BET

- BET Gospel

- Biography Channel

- BlueHighways TV

- Bounce TV

- Bravo

- C-SPAN

- C-SPAN 2

- C-SPAN 3

- CBS Sports Network

- Centric

- Chiller

- cloo

- CMT

- CMT Pure Country

- CNBC

- CNBC World

- Comedy Central

- Cooking Channel

- Create

- Crime & Investigation Network

- Current TV

- De Pelicula

- De Pelicula Clasico

- Destination America

- Discovery

- Discovery en Espanol

- Discovery Familia

- Discovery Fit & Health

- DIY

- E! Entertainment

- Encore

- Encore Action

- Encore Drama

- Encore Espanol

- Encore Family

- Encore Love

- Encore Suspense

- Encore Westerns

- Flix

- Food Network

- FOROTv

- G4

- GAC

- Galavision

- Game Show Network

- Golf Channel

- H2

- Hallmark Channel

- Hallmark Movie Channel

- Halogen

- HGTV

- History

- IndiePlex

- INSP

- Investigation Discovery

- ION Life

- KCPT (PBS)

- KCTV 5 (CBS)

- KCWE 29 (CW)

- KMBC 9 (ABC)

- KMCI 38

- KPXE 50 (ION)

- KSHB 41 (NBC)

- KSMO 62

- KUKC 48 (Univision)

- La Familia Cosmovision

- Lifetime

- Lifetime Move Network

- Lifetime Real Women

- Live Well

- LOGO

- MeTV

- MGM

- Military Channel

- Military History

- MLB Network

- MoviePlex

- MSNBC

- MTV

- MTV Hits

- MTV Jams

- MTV tr3s

- MTV2

- MTVU

- mun2

- NASA

- NBC Sports Network

- NFL

- NFL Redzone

- NHL

- Nick 2

- Nick Jr.

- Nickelodeon

- Nicktoons

- Olympics Channel 1

- Olympics Channel 2

- Outdoor Channel

- OWN

- Oxygen

- Palladia

- PBS Encore

- PBS Kids Sprout

- qubo

- QVC

- REELZChannel

- RetroPlex

- Ritmoson Latino

- Science channel

- Sho2

- Showtime

- Showtime Beyond

- Showtime Extreme

- Showtime Family Zone

- Showtime Next

- Showtime Showcase

- Showtime Women

- Smithsonian

- Spike TV

- Sportsman Channel

- Starz

- Starz Cinema

- Starz Comedy

- Starz Edge

- Starz in Black

- Starz Kids and Family

- Style!

- SyFy

- TBN Enlace

- Teen Nick

- Telefutura

- Telehit

- Telemundo

- Tennis Channel

- The History en Espanol

- The Hub

- This TV

- TLC

- TMC Extra

- TMC: The Movie Channel

- Travel Channel

- TV Land

- TVG

- Universal

- Univision Deportes

- Univision tlnovelas

- USA Network

- VH1

- VH1 Classic

- VH1 Soul

- WDAF 4 (FOX)

- WealthTV

- Weather channel

- WGN

- Youtoo TV

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Tops Consumer Spending for Technology

Consumer spending on mobile products tops all consumer categories in 2012, according to analysts at Gartner, who point out that "the three largest segments of the consumer technology market are, and will continue to be, mobile services, mobile phones and entertainment services," according to Amanda Sabia, principal research analyst at Gartner.

Mobile services are expected to generate 37 percent of total worldwide consumer technology spending in 2012, $0.8 trillion, rising to almost $1 trillion by 2016.

Mobile phones will account for 10 percent of total spending in 2012, about $222 billion, rising to almost $300 billion by 2016.

Similarly, entertainment services including cable, satellite, IPTV and online gaming, will account for 10 percent of total consumer spending on technology products and services in 2012, at $210 billion, rising to almost $290 billion in 2016.

Gartner predicts that consumer spending on mobile apps stores and content will rise from $18 billion in 2012 to $61 billion by 2016, and that spending on e-text content (e-books, online news, magazines and information services) will rise from $5 billion in 2012 to $16 billion by 2016.

Consumers will spend $2.1 trillion worldwide on digital information and entertainment products and services in 2012, according to Gartner, Inc. This amounts to a $114 billion global increase compared with 2011, and spending will continue to grow at a faster rate than in the past, at around $130 billion a year, to reach $2.7 trillion by the end of 2016.

The $2.1 trillion consists of what the consumers will spend on mobile phones, computing and entertainment, media and other smart devices, the services that are required to make these devices connected to the appropriate network, and software and media content that are consumed via these devices.

Mobile services are expected to generate 37 percent of total worldwide consumer technology spending in 2012, $0.8 trillion, rising to almost $1 trillion by 2016.

Mobile phones will account for 10 percent of total spending in 2012, about $222 billion, rising to almost $300 billion by 2016.

Similarly, entertainment services including cable, satellite, IPTV and online gaming, will account for 10 percent of total consumer spending on technology products and services in 2012, at $210 billion, rising to almost $290 billion in 2016.

Gartner predicts that consumer spending on mobile apps stores and content will rise from $18 billion in 2012 to $61 billion by 2016, and that spending on e-text content (e-books, online news, magazines and information services) will rise from $5 billion in 2012 to $16 billion by 2016.

Consumers will spend $2.1 trillion worldwide on digital information and entertainment products and services in 2012, according to Gartner, Inc. This amounts to a $114 billion global increase compared with 2011, and spending will continue to grow at a faster rate than in the past, at around $130 billion a year, to reach $2.7 trillion by the end of 2016.

The $2.1 trillion consists of what the consumers will spend on mobile phones, computing and entertainment, media and other smart devices, the services that are required to make these devices connected to the appropriate network, and software and media content that are consumed via these devices.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Telefonica Suspends Dividend, Share Buybacks

Telefónica will cancel the payment of all remaining dividends and share buybacks for 2012, an action that shows the stresses now experienced by businesses of all sorts in Spain, as a result of the economic and financial crises roiling Spain.

Telefonica's suspension of dividend payments is a risky step, as it would be for any public firm viewed as a "value" stock paying hefty dividends. The problem is partly a debt overhang that has to be rectified, plus a complete lack of revenue growth for the remainder of the year.

The company said it now anticipates no significant revenue growth this year, compared with a previous expectation of revenue growth of at least one percent. Telefónica said it will resume its dividend payments in 2013, with a dividend of 75 European cents a share to be delivered in two tranches, in the fourth quarter of 2013 and second quarter of 2014.

That of course assumes Telefónica can fix its immediate problems, namely controlling operating costs and getting debt to below 2.35 times operating profit in 2012.

Telefónica's Spain operations, in the second quarter of 2012, saw revenue drop 13 percent year over year, compared with a six-percnet decrease for the European unit overall.

Perhaps most shockingingly, mobile phone usage revenue dropped 18 percent. You might conclude either that people indeed are not as attached to their mobile phones as once was thought, or that the Spanish economic crisis is so bad people have no choice, or that substitutes are being used, such as lower-cost services using "SIM-only" approaches.

Telefonica's suspension of dividend payments is a risky step, as it would be for any public firm viewed as a "value" stock paying hefty dividends. The problem is partly a debt overhang that has to be rectified, plus a complete lack of revenue growth for the remainder of the year.

The company said it now anticipates no significant revenue growth this year, compared with a previous expectation of revenue growth of at least one percent. Telefónica said it will resume its dividend payments in 2013, with a dividend of 75 European cents a share to be delivered in two tranches, in the fourth quarter of 2013 and second quarter of 2014.

That of course assumes Telefónica can fix its immediate problems, namely controlling operating costs and getting debt to below 2.35 times operating profit in 2012.

Telefónica's Spain operations, in the second quarter of 2012, saw revenue drop 13 percent year over year, compared with a six-percnet decrease for the European unit overall.

Perhaps most shockingingly, mobile phone usage revenue dropped 18 percent. You might conclude either that people indeed are not as attached to their mobile phones as once was thought, or that the Spanish economic crisis is so bad people have no choice, or that substitutes are being used, such as lower-cost services using "SIM-only" approaches.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, July 25, 2012

London Olympics Bans Personal Hotspots

Big, temporary events always pose a problem for access service providers. Because the large expected increases in access network use are temporary, it is difficult to add enough temporary capacity to cope with all expected demand. One way to manage expected congestion is simply to allow connections to slow, degrade and essentially create blockages.

So it is that, in addition to banning such obvious things as explosives and weapons from Olympic venues, attendees are advised by the London Olympics that personal wireless access points and and 3G hubs (smart devices such as personal hotspot devices or the personal hotspot functions of smart phones are banned from Olympic venues.

Android phones, iPhone and tablets are permitted inside venues, but must not be used as

wireless access points to connect multiple devices, the London Olympics says.

The ban will be hard to enforce, but organizers say that, in principle, offending devices will be confiscated.

So it is that, in addition to banning such obvious things as explosives and weapons from Olympic venues, attendees are advised by the London Olympics that personal wireless access points and and 3G hubs (smart devices such as personal hotspot devices or the personal hotspot functions of smart phones are banned from Olympic venues.

Android phones, iPhone and tablets are permitted inside venues, but must not be used as

wireless access points to connect multiple devices, the London Olympics says.

The ban will be hard to enforce, but organizers say that, in principle, offending devices will be confiscated.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Satellite Still Makes Sense in Rural Areas, Frontier Bets

The Frontier Communications Corporation wholesale agreement with Hughes Network Systems to create a branded, satellite-based broadband access service shows that debates over "which access network is best" miss the point. A range of networks "make sense" for different population

Frontier will sell satellite-based broadband services, branded "Frontier Broadband, to what Frontier estimates are several hundred thousand households and small businesses within markets previously unserved or underserved by all broadband providers, including cable.

Notice that Frontier did not brand the service "Frontier Satellite Broadband." It is broadband, provided to some potential customers that Frontier cannot reach using its fixed network.

As the mobile network provides huge value, even though raw speed is not as high as is possible on a fixed network, so a variety of technologies and networks make economic sense for urban, suburban, rural and isolated potential customers. No single network is "best" for every scenario.

Still, each type of technology tends to be regulated using different rules.

And it still raises regulatory hackles when contestants using different networks, and regulated under different rules, decide it makes sense to "cross the lines." That seems to be the case with the agency deals allowing Verizon to sell cable operator services, while cable operators can sell Verizon services.

Historically, the industry has seen strife over issues of which types of networks can receive funds from agencies that support rural communications, as well. Incumbent telcos have argued that it is unfair for competitive local exchange carriers or mobile carriers to receive support funds traditionally awarded only to fixed network telcos, even when the functional capability supplied by all of the contestants is precisely what the programs are supposed to support.

Those debates are likely to become sharper in the future.

Frontier will sell satellite-based broadband services, branded "Frontier Broadband, to what Frontier estimates are several hundred thousand households and small businesses within markets previously unserved or underserved by all broadband providers, including cable.

Notice that Frontier did not brand the service "Frontier Satellite Broadband." It is broadband, provided to some potential customers that Frontier cannot reach using its fixed network.

As the mobile network provides huge value, even though raw speed is not as high as is possible on a fixed network, so a variety of technologies and networks make economic sense for urban, suburban, rural and isolated potential customers. No single network is "best" for every scenario.

Still, each type of technology tends to be regulated using different rules.

And it still raises regulatory hackles when contestants using different networks, and regulated under different rules, decide it makes sense to "cross the lines." That seems to be the case with the agency deals allowing Verizon to sell cable operator services, while cable operators can sell Verizon services.

Historically, the industry has seen strife over issues of which types of networks can receive funds from agencies that support rural communications, as well. Incumbent telcos have argued that it is unfair for competitive local exchange carriers or mobile carriers to receive support funds traditionally awarded only to fixed network telcos, even when the functional capability supplied by all of the contestants is precisely what the programs are supposed to support.

Those debates are likely to become sharper in the future.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Virgin Media Says 41% of New Customers Buy Broadband Access at 60 Mbps or Higher

Broadband customers on tiers of service offering speeds of at least 30 Mbps now represent 31 percent of its total broadband user base, according to Virgin Media. About 14 percent of all customers buy services at 60 Mbps or above.

Broadband customers on tiers of service offering speeds of at least 30 Mbps now represent 31 percent of its total broadband user base, according to Virgin Media. About 14 percent of all customers buy services at 60 Mbps or above. At least in part, that is because Virgin Media in April 2012 made 30 Mbps the entry level tier of service.

Around 41 percent of Virgin Media new customers chose took speeds of more than 60 Mbps, while plans to double the speeds of four million users are well underway.

Virgin's experience confirms what most of you would suspect, namely that lower prices drive adoption of faster broadband access services.

Virgin Media now sells service operating at 30 Mbps to 40 Mbps for £14.50 a momth. Also, says Virgin Media, the 30 Mbps service it sells is less costly than the 40 Mbps service marketed by BT.

Virgin Media services operating at 60 Mbps to 80 Mbps cost £18.50. Service at 100 Mbps costs £25.50 a month.

Of course, Virgin Media's prices are lower than BT's prices, at each of the tiers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, July 24, 2012

Amazon.com Launches a new Training Initiative

Amazon is launching a new, and as yet experimental, "Career Choice Program" for people who work at Amazon's fulfillment centers.

The program is unusual. Unlike traditional tuition reimbursement programs, Amazon exclusively funds education only in areas that are well-paying and in high demand according to sources like the U.S. Bureau of Labor Statistics, and funds those areas regardless of whether those skills are relevant to a career at Amazon.

Many of our fulfillment center employees will choose to build their careers at Amazon. For others, a job at Amazon might be a step towards a career in another field. We want to make it easier for employees to make that choice and pursue their aspirations.

For people who've been with Amazon as little as three years, Amazon is offering to pre-pay 95 percent of the cost of courses such as aircraft mechanics, computer-aided design, machine tool technologies, medical lab technologies, nursing, and many other fields.

The program is unusual. Unlike traditional tuition reimbursement programs, Amazon exclusively funds education only in areas that are well-paying and in high demand according to sources like the U.S. Bureau of Labor Statistics, and funds those areas regardless of whether those skills are relevant to a career at Amazon.

Many of our fulfillment center employees will choose to build their careers at Amazon. For others, a job at Amazon might be a step towards a career in another field. We want to make it easier for employees to make that choice and pursue their aspirations.

For people who've been with Amazon as little as three years, Amazon is offering to pre-pay 95 percent of the cost of courses such as aircraft mechanics, computer-aided design, machine tool technologies, medical lab technologies, nursing, and many other fields.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Square Near a Deal to Value It at $3.25 Billion

Square, the mobile payments supplier, is close to raising roughly $200 million in new funding, with an implied valuation of $3.25 billion, the NYTimes reports.

The funding represents the company’s third significant capital raising round in less than two years. In 2011, Square raised $100 million, valuing the company at $1.6 billion. Several months before that, Square had an investment at a $240 million valuation. All told, the company’s valuation has grown by 13.5 times in less than two years.

You can make your own determination about the appropriateness of the valuation.

The funding represents the company’s third significant capital raising round in less than two years. In 2011, Square raised $100 million, valuing the company at $1.6 billion. Several months before that, Square had an investment at a $240 million valuation. All told, the company’s valuation has grown by 13.5 times in less than two years.

You can make your own determination about the appropriateness of the valuation.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple: the Company that Used to Make Computers

These days, phones and other portable devices are what Apple makes and sells. The really surprising number, for some of us, is the dominance of "phones" in the revenue picture.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...