What is true of global aggregate performance in the telecom business might not be so true for discrete service providers in specific markets. So it appears that prospects for voice and messaging revenue might be robust in some markets, even if that is not the case in other regions, or for the global market as a whole, an analysis by Infonetics Research might suggest.

Despite the popularity of over-the-top messaging applications like Apple’s iMessage and WhatsApp, Infonetics Research predicts that text messaging (short message service, or SMS) revenue will grow, on a global basis, every year from 2012 to 2016, delivering a cumulative $1 trillion in operator revenue during those five years.

Over that same period, voice revenue will decline slightly,, Infonetics Research predicts. Voice revenue dipped 0.8 percent worldwide in 2011, despite the growing use of voice services in China, for example.

On a global basis, Infonetics expects mobile service providers will see a six-percent increase overall in revenue from mobile voice, mobile broadband, and mobile messaging services in 2012. The issue is the specific contribution from each of those services, in each country and market.

The highest growth in 2012 will come from Asia Pacific and Latin America regions, while the Europe, Middle East and Africa region is expected to see a slight decline.

Globally, the mobile services market is forecast to grow to $976 billion by 2016, with the bulk of the growth coming from mobile broadband services, as you might expect.

Mobile data (text messaging, multimedia messaging, and mobile broadband) service revenue rose in every region in 2011, driven by an increase in smart phone usage, though the specific contributions made by messaging and mobile broadband are important.

Mobile broadband subscribers will grow from 15 percent to nearly 40 percent of all mobile subscribers between 2011 and 2016, Infonetics Research suggests.

Tuesday, July 17, 2012

Some Mobile Service Providers Will Face More Challenges in Voice, Text, Than Others

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

One Mobile Operator Apps Consortium Dies, Another Gets Ready to Launch

One very large mobile service provider effort to create a stronger Web applications business has given up the chase, while another more-focused consortium is getting ready to launch.

The Wholesale Applications Community, a large consortium of leading GSM-based mobile service providers from around the world, has decided to sell off it sassets and merge the remainder of the effort into a parallel GSM Association effort.

Separately, AT&T, Deutsche Telekom, Vodafone Group, Verizon Wireless and Telefónica, for example, separately are setting up an interoperable way of allowing all of their customers to buy any mobile application available in any member application store.

As often is the case, very-large consortia can become unwieldy, especially when time to market is a concern, as arguably is the case for any mobile service provider effort to create a viable app store effort able to compete with the likes of Apple and Google.

Apigee, a leading provider of API products and services, has acquired the technology assets of WAC, principally a carrier billing programming interface. for in-app purchases.

WAC was started in 2010 and was backed by 60 operators and suppliers, including Samsung, Intel, Nokia, Ericsson, Qualcomm, Fujitisu, NEC, Hewlett-Packard, HTC, LG and Research in Motion.

The objective was to create a common standard for Web applications usable by all GSM service providers, rather than common mobile applications in a direct sense.

As you might guess, the initiative was intended to create more value for mobile service providers in a world where applications were viewed as rapidly consolidating in the ecosystems run by Apple and Google.

You might say the results have been unspectacular, but that might not be surprising to industry watchers who have been saying the odds of success were high to begin with. The global telecom industry has had a rather mixed record of success creating key standards that drive a significant amount of market success.

ncluding the building of substantial third party and “owned” applications that can use the APIs.

The Wholesale Applications Community, a large consortium of leading GSM-based mobile service providers from around the world, has decided to sell off it sassets and merge the remainder of the effort into a parallel GSM Association effort.

Separately, AT&T, Deutsche Telekom, Vodafone Group, Verizon Wireless and Telefónica, for example, separately are setting up an interoperable way of allowing all of their customers to buy any mobile application available in any member application store.

As often is the case, very-large consortia can become unwieldy, especially when time to market is a concern, as arguably is the case for any mobile service provider effort to create a viable app store effort able to compete with the likes of Apple and Google.

Apigee, a leading provider of API products and services, has acquired the technology assets of WAC, principally a carrier billing programming interface. for in-app purchases.

WAC was started in 2010 and was backed by 60 operators and suppliers, including Samsung, Intel, Nokia, Ericsson, Qualcomm, Fujitisu, NEC, Hewlett-Packard, HTC, LG and Research in Motion.

The objective was to create a common standard for Web applications usable by all GSM service providers, rather than common mobile applications in a direct sense.

As you might guess, the initiative was intended to create more value for mobile service providers in a world where applications were viewed as rapidly consolidating in the ecosystems run by Apple and Google.

You might say the results have been unspectacular, but that might not be surprising to industry watchers who have been saying the odds of success were high to begin with. The global telecom industry has had a rather mixed record of success creating key standards that drive a significant amount of market success.

ncluding the building of substantial third party and “owned” applications that can use the APIs.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, July 16, 2012

55% of U.S. Smart Phone Owners Compare Prices Inside Stores, Study Finds

Some 55 percent of smart phone owners said they’ve used a mobile device to compare prices between retailers, while inside retail stores, according to Emphatica.

Thirty-four percent said they’ve scanned a QR code, and 27 percent have read online reviews from their devices before making purchase decisions.

Thirty-four percent said they’ve scanned a QR code, and 27 percent have read online reviews from their devices before making purchase decisions.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

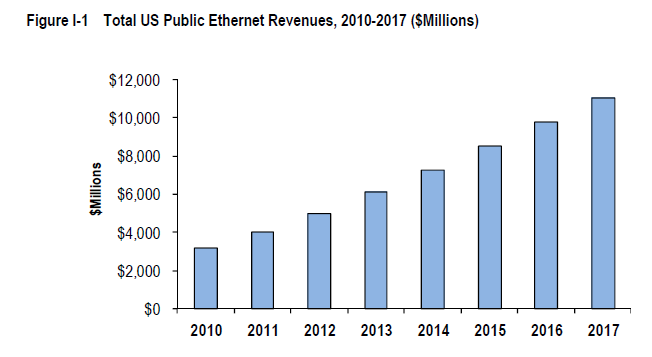

Carrier Ethernet Growing at 17% Annual Rate

U.S. enterprises and consumers are expected to spend more than $47 billion over the next five years on Ethernet services provided by carriers, according to a new market research study from The Insight Research Corporation.

With metro-area and wide-area Ethernet services readily available from virtually all major data service providers, industry revenue is expected to grow from nearly $5 billion in 2012 to reach just over $11 billion by 2017.

However, year over year spending growth is expected to gradually stall and by 2017 the annual revenue growth rate will be half of what it is today, Insight Research says. Growth is generally moderating gradually, for a number of reasons.

For starters, the installed base of revenue is growing larger, so it is harder to maintain higher growth rates. Also, at some point, most U.S. cell sites will have been converted to carrier Ethernet.

Pricing pressures will continue as competition remains significant in the market, and as Ethernet displaces most private line and frame relay services.

According to the study, Ethernet's central driver continues to be its ability to meet seemingly endlessly growing bandwidth demands at lower cost and with greater flexibility than competing services.

A major growth driver in years past had been the large-scale migration of wireless backhaul cell sites from TDM to Ethernet, and though still a contributory growth factor, backhaul growth will start to moderate as LTE deployments are completed.

"Wireless backhaul had been a major factor in this fast-growing telecommunications services sector, but with much of the conversion of TDM to Ethernet completed, we are forecasting that spending on Ethernet will moderate," says Robert Rosenberg, president of Insight Research. "Over the five year forecast period we project a compounded annual revenue growth rate of 17 percent, with growth slowing by 2016 to be more in the range of 12 to 15 percent.”

With metro-area and wide-area Ethernet services readily available from virtually all major data service providers, industry revenue is expected to grow from nearly $5 billion in 2012 to reach just over $11 billion by 2017.

However, year over year spending growth is expected to gradually stall and by 2017 the annual revenue growth rate will be half of what it is today, Insight Research says. Growth is generally moderating gradually, for a number of reasons.

For starters, the installed base of revenue is growing larger, so it is harder to maintain higher growth rates. Also, at some point, most U.S. cell sites will have been converted to carrier Ethernet.

Pricing pressures will continue as competition remains significant in the market, and as Ethernet displaces most private line and frame relay services.

According to the study, Ethernet's central driver continues to be its ability to meet seemingly endlessly growing bandwidth demands at lower cost and with greater flexibility than competing services.

A major growth driver in years past had been the large-scale migration of wireless backhaul cell sites from TDM to Ethernet, and though still a contributory growth factor, backhaul growth will start to moderate as LTE deployments are completed.

"Wireless backhaul had been a major factor in this fast-growing telecommunications services sector, but with much of the conversion of TDM to Ethernet completed, we are forecasting that spending on Ethernet will moderate," says Robert Rosenberg, president of Insight Research. "Over the five year forecast period we project a compounded annual revenue growth rate of 17 percent, with growth slowing by 2016 to be more in the range of 12 to 15 percent.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Digital Local Media Ads to Grow 13.1% in 2012, According to BIA/Kelsey

Mobile search will grow faster, at 77.2 percent. Online video will grow 51.6 percent and social will grow 26.3 percent.

Compound average growth rates between 2011 and 2016 include:

* newspapers – online revenues: 5.0 percent

* radio – online revenues: 11.8 percent

* television – online revenues: 12.8 percent

* digital out of home: 11.7 percent

* online: 9.4 percent

* mobile: 44.9 percent

* Internet Yellow Pages: 12.5 percent

* email, reputation and presence management: 14.9 percent

* social media: 21.0 percent

* online video: 36.7 percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Devices Now Becoming a Way for Application Providers to Connect Consumers with Apps

“We always wanted to be in the hardware business,” Google Chairman Eric Schmidt says. That comment, whether fully accurate as a description of Google's thinking or not, does seem to describe current thinking in much of the applications business.

Sony has for decades argued that ownership of content was important for selling TVs. Apple found that iTunes enabled it to create a dominant position in the MP-3 player market. The App Store has been crucial for iPad and iPhone sales, in the same way that the Android Market and Google Play have been important for sales of Android devices.

Amazon's content richness is a key reason for the success of the Kindle Fire. So though it might not be a feasible strategy for every application provider, it certainly seems true that an integrated device plus content and software strategy makes increasing sense.

In other markets, the success of the Square mobile software that turns a tablet or a smart phone into a retail point of sale terminal provides another example of how hardware enables a software or service business.

And Oracle has seen value in bundling hardware with enterprise applications.

Sony has for decades argued that ownership of content was important for selling TVs. Apple found that iTunes enabled it to create a dominant position in the MP-3 player market. The App Store has been crucial for iPad and iPhone sales, in the same way that the Android Market and Google Play have been important for sales of Android devices.

Amazon's content richness is a key reason for the success of the Kindle Fire. So though it might not be a feasible strategy for every application provider, it certainly seems true that an integrated device plus content and software strategy makes increasing sense.

In other markets, the success of the Square mobile software that turns a tablet or a smart phone into a retail point of sale terminal provides another example of how hardware enables a software or service business.

And Oracle has seen value in bundling hardware with enterprise applications.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sprint Accelerates Roll-Out of Long Term Evolution Network

Sprint appears to be accelerating its deployment of its new 4G Long Term Evolutiion network, announcing availability in 15 cities where it had promised availability in just five cities. Those cities include:

Atlanta

Athens, Ga.

Calhoun, Ga.

Carrollton, Ga.

Newnan, Ga.

Rome, Ga.

Dallas

Fort Worth, Texas

Granbury-Hood County, Texas

Houston

Huntsville, Texas

San Antonio, Texas

Waco, Texas

Kansas City, Mo.-Kan.

St. Joseph, Mo.

Atlanta

Athens, Ga.

Calhoun, Ga.

Carrollton, Ga.

Newnan, Ga.

Rome, Ga.

Dallas

Fort Worth, Texas

Granbury-Hood County, Texas

Houston

Huntsville, Texas

San Antonio, Texas

Waco, Texas

Kansas City, Mo.-Kan.

St. Joseph, Mo.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...