European Commission telecom regulators apparently are circulating a draft proposal creating a new regulatory framework intended to spur faster investment in next generation fiber to the home networks. The general outlines appear consistent with approaches taken earlier by U.S. regulators that had to balance “investment” and “competition” incentives to encourage more investment in fiber to home facilities.

Among the key proposed changes is an increase in prices network owners can charge competitors who lease access circuits, network elements and infrastructure, as well as a suspension of mandatory wholesale price rules for the new fiber to home networks.

The rules would first raise revenue for the incumbents leasing capacity to rivals, and then allow setting of commercial rates for future access to the fiber to home facilities. Both moves would aim to bolster incumbent finances while creating clearer incentives for investing in fiber to home networks.

The plan illustrates once again how telecom regulators can directly affect competitor revenue and cost assumptions and business plans.

Under the new plan,, monthly rental access prices per customer would range between eight and 10 euros by the end of 2016. That would mean higher charges paid by competitive carriers in 10 EU countries including the Netherlands, Austria, Poland, Hungary and Estonia, which currently offer rates below eight euros.

On the other hand, Ireland, which currently has the highest monthly cost at 12.41 euros, Finland, Britain and Luxembourg would have to bring their prices down.

The EC has been looking at wholesale rates as part of a wider effort to create incentives for investment in faster fiber to home networks. The investment problem, up to this point, has been that incumbent carriers have seen little reason to invest heavily under circumstances where the fiber network rates are highly regulated.

Of particular concern are rules that set wholesale access rates too low, thereby reducing the revenue earned from selling competitors wholesale access to those new networks.

The very same argument occurred in the U.S.market, for precisely the same reasons, with essentially the same format adopted.

In the U.S. market, after a period of mandatory and significant wholesale discounts, wholesale access to copper and all fiber facilities was deregulated, allowing market rates to be set by contracts, rather than relying on mandatory price rules.

The issue in the U.S. market, as in the EC, was that incumbent carriers argued they could not upgrade to fiber facilities because the steep discounts did not allow them to earn a reasonable return on invested capital.

In North America and Europe, it increasingly seems as though regulators can have “more competition” or they can have “ more investment,” but not both, in the fixed network realm.

In order to reach the European Community’’s “Digital Agenda” goal of at least half of EC residents able to access broadband at 100Mbps or more by 2020, the EC has been looking at how the regulatory environment can support and stimulate investment in next-generation networks. The draft proposal is the result of that investigation.

Essentially, regulators have two fundamental choices: mandate aggressive wholesale rules to spur competition, or allow service providers to “keep” the potential revenue from investment in new facilities by relaxing wholesale obligations.

In the U.S. market, after an extensive experiment with mandatory wholesale access with hefty discounts, triggered by the Telecommunications Act of 1996, regulators had to make a choice.

The major facilities-based access providers essentially signaled that they were not going to make major investments in new optical infrastructure so long as mandatory access with hefty discounts remained policy, especially when a rival broadband network, already operated by a local cable operator, already was in business, without any mandatory access obligations at all.

Eventually, to the chagrin of competitors, the Federal Communications Commission reversed course, allowing incumbents to charge market-based rates, in return for heavier investment in new optical access.

Historically, European regulators, operating in markets where there had not been robust deployment of cable broadband, favored heavy use of wholesale access.

But in a significant “u turn,” European Community telecom commissioner Neelie Kroes backed off a plan to increase the discounts offered to third parties who buy wholesale access from incumbent European Union service providers.

Clearly, such a plan would have further reduced carrier incentives to invest in new fiber plant. For competitors, the new rules also would raise operating costs, making it harder to compete.

But that's the dilemma regulators face: encouraging competition by mandating lower wholesale rates also decreases incentives for facilities owners to invest in new optical plant.

Monday, December 3, 2012

EC Proposes Higher Wholesale Access Prices

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, December 2, 2012

Still Time to "Harvest" Video Revenues

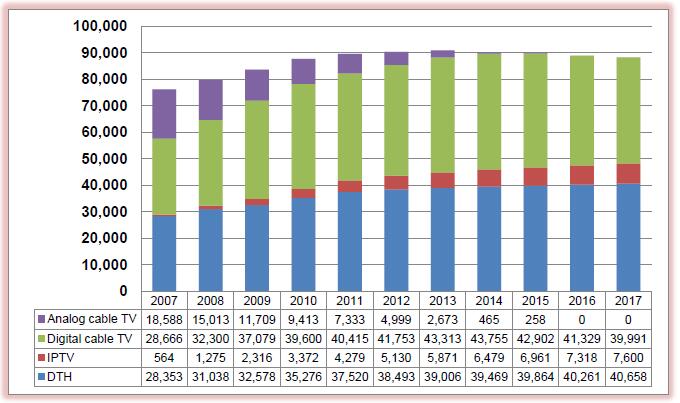

The number of U.S. telco video subscribers will rise from 8.8 million in 2011 to 18.6 million in 2017, according to Parks Associates now forecasts. That gain by telcos will come from share presently held by cable TV customers and satellite providers.

Satellite's share of the subscription video market will drop to 30 percent by 2017, while cable's share will fall to 52 percent, while telco IPTV share will rise to 18 percent.

Cable video subscribers will decline from 60.7 million in 2011 to 56.1 million in 2017.

Those figures show the difference between incumbent and attacking providers in a mature market. Under those conditions, “harvesting” is a typical business strategy for leading contestants in declining markets.

When executives believer there is no real opportunity to reverse a product slide into the declining side of its product life cycle, it makes sense to harvest cash, but not to invest too much to “save” the business, or turn it around, as the judgment simply is that the business is mature and inevitably will decline.

It does make sense to invest only enough to slow the rate of decline, of course. Attackers, on the other hand, can do nicely for a while simply by taking market share.

Video is largely becoming a harvesting exercise for cable operators, just as long distance calling and legacy voice are examples of “harvesting” by telcos.

As the attacker in voice and business services, cable operators still can grow revenue in the near term, as telcos can grow revenue in video. Over the longer term, though, even attackers can only achieve so much, in a maturing market.

For cable, consumer voice revenues have ceased to be much of a growth business, which explains the shift to business customers. Telcos and satellite video providers still have room to continue taking video share, though. Sooner or later, that might run into resistance, especially if over the top video, featuring the same content now part of video subscriptions, takes off.

A new ABI Research study suggests that nearly 20 percent of online video consumers consider online video as a replacement for entertainment video subscriptions. That obviously represents “significant risk” to the traditional video entertainment business.

ABI Research suggests the magnitude of potential revenue loss could range as high as $16.8 billion in the U.S. market, for example. Telcos won’t face those issues, as they are predicted by virtually every study to continue taking market share, as cable TV operators and satellite providers continue to lose market share over time.

But at least one analysis has satellite providers overtaking cable TV providers in revenue in 2017.

So the near term trends might not be “linear,” as some forecasters still project cable TV operator and satellite provider video revenues growing for a period, Digital TV Research forecasts.

But a change that shaves as much as $17 billion from U.S. providers would seem to be a longer-term danger, as ABI Research also suggests U.S. video entertainment penetration is dropping at a rate of about 0.5 percent per year through 2017.

That arguably is an optimistic scenario for cable TV providers. Ignoring changes of market share between the contestants, a loss of perhaps half a percent a year of subscribers won’t make a large dent in a revenue stream that collectively represents more than $90 billion in annual revenue.

If the number of subscribers were directly related to the amount of revenue, then a half percent a year decline would represent perhaps $450 million in lost revenue each year. At such rates, it would take decades before service providers lost $17 billion.

Whatever share shift one expects, the game now for video service providers is to “take or protect” market share.

North America pay TV revenues ($ mil.)

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Why Google, Facebook, Apple "Mobile Service Provider" Rumors Never Cease

From time to time there are new rumors that Facebook, Apple or Google "might" become mobile service providers, using a mobile virtual network operator model. Some think it doesn't make sense.

But the rationale for being a mobile service provider is a bit more complicated than it used to be. For starters, "voice" revenue is not the only reason for doing so. These days, Internet access makes almost as much sense.

Also, for application providers with other revenue models, becoming a service provider would allow creation of packages and plans that cold be much more differentiated than currently are available from the leading mobile service providers.

But the lure of revenue might still be important. In the global telecom business, there have been complaints for years from telecom executives that third party app providers build businesses on the back of telco-provided access services, but that the access providers do not share in the revenue created.

In a potentially new development, some application providers might be taking a similar view, sensing that they create huge value for telcos, but do not participate in the access revenue stream, for example.

Strand Consult now speculates on whether Facebook, for example, is willing to look beyond advertising as a source of revenue, and whether Facebook would become a mobile virtual network operator, as a way to create a new revenue stream, as well as recapture some of the value it believes it is creating in the ecosystem.

As some have speculated about the value of Facebook creating its own branded smart phone, Strand Consult now speculates about the value of Facebook becoming a service provider.

Becoming an “MVNO is a logical step for Facebook the world’s largest communication platform,” Strand Consult analysts argue.

One billion users already consider Facebook as their de facto telephone book for friends and family and use the platform for communicating by SMS, text, image and video, the firm argues.

Aside from its huge user base, Facebook has credit card credentials on file already for millions of its users, many of whom purchase premium games, driving one sixth of Facebook’s revenue.

How much could Facebook earn as an MVNO? Facebook currently earns annual revenue per user of $4. An MNVO can earn between $10 a month and $50 a month per customer with an operating margin between 20 percent and 25 percent.

Facebook arguably is in no mood to consider such diversions. But Google or Apple, both with key application and gadget businesses, might have more motivation to do so.

But the rationale for being a mobile service provider is a bit more complicated than it used to be. For starters, "voice" revenue is not the only reason for doing so. These days, Internet access makes almost as much sense.

Also, for application providers with other revenue models, becoming a service provider would allow creation of packages and plans that cold be much more differentiated than currently are available from the leading mobile service providers.

But the lure of revenue might still be important. In the global telecom business, there have been complaints for years from telecom executives that third party app providers build businesses on the back of telco-provided access services, but that the access providers do not share in the revenue created.

In a potentially new development, some application providers might be taking a similar view, sensing that they create huge value for telcos, but do not participate in the access revenue stream, for example.

Strand Consult now speculates on whether Facebook, for example, is willing to look beyond advertising as a source of revenue, and whether Facebook would become a mobile virtual network operator, as a way to create a new revenue stream, as well as recapture some of the value it believes it is creating in the ecosystem.

As some have speculated about the value of Facebook creating its own branded smart phone, Strand Consult now speculates about the value of Facebook becoming a service provider.

Becoming an “MVNO is a logical step for Facebook the world’s largest communication platform,” Strand Consult analysts argue.

One billion users already consider Facebook as their de facto telephone book for friends and family and use the platform for communicating by SMS, text, image and video, the firm argues.

Aside from its huge user base, Facebook has credit card credentials on file already for millions of its users, many of whom purchase premium games, driving one sixth of Facebook’s revenue.

How much could Facebook earn as an MVNO? Facebook currently earns annual revenue per user of $4. An MNVO can earn between $10 a month and $50 a month per customer with an operating margin between 20 percent and 25 percent.

Facebook arguably is in no mood to consider such diversions. But Google or Apple, both with key application and gadget businesses, might have more motivation to do so.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Smart Phones and Tablets Converging?

In 2011, the majority of all mobile phone owners consumed mobile media on their smart phones and tablet devices, marking an important milestone in the evolution of mobile from being a communication device to a content consumption tool.

Smart phones also have subsumed the MP3 player, to a great extent. Smart phones likewise have generally replaced cameras, alarm clocks and GPS units.

You might also wonder if the other trend could materialize, namely the tablet becoming a replacement for a smart phone. That seems generally unlikely for the 10-inch version of the tablet.

But with tablets now available in seven-inch screen form factors, with some smart phones pushing up to five inches screen size, there is greater potential for a tablet to become a replacement for a smart phone. After all, the form factor difference is between five inches and seven inches.

More important is the relative importance of “voice” and “content consumption” as computing appliance functions. Virtually all computing appliances now are becoming ways people interact with, and consume, all sorts of media and content, even if the smart phone also does duty as the “voice” appliance.

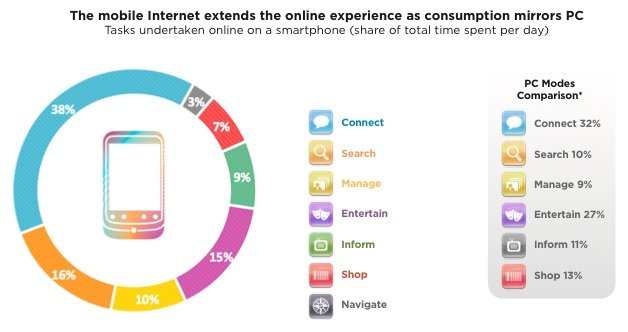

In fact, smart phone and PC user behavior really is converging. In October 2012 about 55 percent of U.S. mobile subscribers used downloaded apps, while 53 percent used a browser. About 39 percent used social networking apps, 34 percent played games and 29 percent listened to music, according to comScore. That isn’t so different from what most people do on PCs, to say nothing of tablets.

In December 2011, 8.2 percent of all web page views occurred on devices other than PCs, for example, with mobile devices accounting for 5.2 percent of traffic, tablets driving 2.5 percent, according to the latest Nielsen Cross-Platform Report.

In 2011, the majority of all mobile phone owners consumed mobile media on their smart phones and tablet devices, marking an important milestone in the evolution of mobile from primarily a

communication device to a content consumption tool.

Of course, the application convergence also goes the other way: smart phones increasingly are used as a primary content consumption screen.

A study by Orange shows a stark contrast in mobile media habits between teenagers and adults in the U.K. market, for example.

For teenagers, the mobile phone is the primary screen, for the first time, not the TV or PC.

Also, adults are using multiple screens more interchangeably than ever before, choosing the most suitable screen for any particular situation, Orange says.

In the United Kingdom, 83 percent of teenagers have a smart phone and 95 percent have one in Spain. In addition, 92 percent of teenagers in the United Kingdom say mobile is a “way to always have a media device at hand” and 55 per cent of teenagers in the UK say that they prefer their mobile over other screens.

Consumers also are increasingly using their mobile or tablet to replicate the same experience on their PC, about 62 percent of consumers in the United Kingdom agree. Consumers also are multitasking. Some 90 percent of consumers access the internet at the same time as watching TV, in the United Kingdom.

At the same time as interchangeable usage is occurring, larger screens on smart phones are making accessing multimedia easier, and “smaller” sized tablets are increasing their portability. In Spain, 16 percent of tablet owners also own the more portable Samsung Galaxy Tab, for example.

The percentage of people primarily accessing mobile media ‘out and about’ on both their mobile and tablet has significantly increased across all markets.

In the United Kingdom 58 percent of respondents say they use their devices to access content and media while out and about.

Tablet use to access content and media “out and about” has grown from 11 percent of users in 2011 to 21 percent in 2012 in the United Kingdom.

And though some would say tablets are not a substitute for a PC, about 75 percent of tablet media users want to “find the same things on their tablet as on their PC,” the study also found. That doesn’t mean people believe they can “work” on a tablet in the same way as on a PC.

But where it comes to content and information, they do expect they will be able to consume all the same content they would expect to get on a PC.

One of Google’s studies of tablet use over a two-week period, which had users recording every occasion that they used their tablet, shows that tablets really are not PCs, any more than smart phones are used in the same way that PCs are used.

Most consumers use their tablets for fun, entertainment and relaxation while they use their desktop computer or laptop for work, Google User Experience Researchers Jenny Gove and John Webb say. About 91 percent of the time that people spend on their tablet devices is for personal rather than work related activities.

And, as it turns out, when a consumer gets a tablet, they quickly migrate many of their entertainment activities from laptops and smart phones to this new device.

The most frequent tablet activities are checking email, playing games and social networking. The study also found that people are doing more activities in shorter bursts on weekdays (social networking, email) while engaging in longer usage sessions on weekends (watching videos/TV/movies).

Tablets are multi-tasking devices with at least 42 percent of activities occurring while doing another task or engaging with another entertainment medium. Tablets aren’t PCs

As it turns out, lots of things people can do on PCs don’t “need” to be done on PCs. Content consumption, email and other communications actually represent most of what many business users really “have to do” on a PC.

Also, tablets are more accurately described as “untethered” devices than “mobile” devices, to the extent that tablets primarily are used at home. Unlike smart phones that go everywhere and laptops that travel between work and home, few consumers take their tablets with them when they leave the house.

That shipments of tablets are expected to grow from 72.7 million units in 2011 to 383.3 million units by 2017, according to NPD, would not surprise many observers.

Growth in emerging markets, expected to account for up to 46 percent of worldwide shipments by 2017, an increase from the 36 percent share in 2011, might be more surprising.

The tablet forecast also illustrates an important change in connected appliance trends. In the past, “PCs” have been one category of appliances, while MP-3 players, phones and digital organizers, game devices, cameras and e-reading devices have been distinctly different categories.

These days, many of those devices have overlapping functions. Taken as a whole, the changes suggest the crucial role “content consumption” now plays as a lead application for most devices. Though PCs, cameras and organizers still largely have “work or business” use cases, virtually all the other devices are oriented around content consumption.

Smart phones also have subsumed the MP3 player, to a great extent. Smart phones likewise have generally replaced cameras, alarm clocks and GPS units.

You might also wonder if the other trend could materialize, namely the tablet becoming a replacement for a smart phone. That seems generally unlikely for the 10-inch version of the tablet.

But with tablets now available in seven-inch screen form factors, with some smart phones pushing up to five inches screen size, there is greater potential for a tablet to become a replacement for a smart phone. After all, the form factor difference is between five inches and seven inches.

More important is the relative importance of “voice” and “content consumption” as computing appliance functions. Virtually all computing appliances now are becoming ways people interact with, and consume, all sorts of media and content, even if the smart phone also does duty as the “voice” appliance.

In fact, smart phone and PC user behavior really is converging. In October 2012 about 55 percent of U.S. mobile subscribers used downloaded apps, while 53 percent used a browser. About 39 percent used social networking apps, 34 percent played games and 29 percent listened to music, according to comScore. That isn’t so different from what most people do on PCs, to say nothing of tablets.

In December 2011, 8.2 percent of all web page views occurred on devices other than PCs, for example, with mobile devices accounting for 5.2 percent of traffic, tablets driving 2.5 percent, according to the latest Nielsen Cross-Platform Report.

In 2011, the majority of all mobile phone owners consumed mobile media on their smart phones and tablet devices, marking an important milestone in the evolution of mobile from primarily a

communication device to a content consumption tool.

| Mobile Content Usage 3 Month Avg. Ending Oct. 2012 vs. 3 Month Avg. Ending Jul. 2012 Total U.S. Mobile Subscribers (Smartphone & Non-Smartphone) Ages 13+ | |||

| Share (%) of Mobile Subscribers | |||

| Jul-12 | Oct-12 | Point Change | |

| Total Mobile Subscribers | 100.0% | 100.0% | N/A |

| Sent text message to another phone | 75.6% | 75.9% | 0.3 |

| Used downloaded apps | 52.6% | 54.5% | 1.9 |

| Used browser | 51.2% | 52.7% | 1.5 |

| Accessed social networking site or blog | 37.9% | 39.4% | 1.5 |

| Played Games | 33.8% | 34.1% | 0.3 |

| Listened to music on mobile phone | 28.3% | 28.7% | 0.4 |

Of course, the application convergence also goes the other way: smart phones increasingly are used as a primary content consumption screen.

A study by Orange shows a stark contrast in mobile media habits between teenagers and adults in the U.K. market, for example.

For teenagers, the mobile phone is the primary screen, for the first time, not the TV or PC.

Also, adults are using multiple screens more interchangeably than ever before, choosing the most suitable screen for any particular situation, Orange says.

In the United Kingdom, 83 percent of teenagers have a smart phone and 95 percent have one in Spain. In addition, 92 percent of teenagers in the United Kingdom say mobile is a “way to always have a media device at hand” and 55 per cent of teenagers in the UK say that they prefer their mobile over other screens.

Consumers also are increasingly using their mobile or tablet to replicate the same experience on their PC, about 62 percent of consumers in the United Kingdom agree. Consumers also are multitasking. Some 90 percent of consumers access the internet at the same time as watching TV, in the United Kingdom.

At the same time as interchangeable usage is occurring, larger screens on smart phones are making accessing multimedia easier, and “smaller” sized tablets are increasing their portability. In Spain, 16 percent of tablet owners also own the more portable Samsung Galaxy Tab, for example.

The percentage of people primarily accessing mobile media ‘out and about’ on both their mobile and tablet has significantly increased across all markets.

In the United Kingdom 58 percent of respondents say they use their devices to access content and media while out and about.

Tablet use to access content and media “out and about” has grown from 11 percent of users in 2011 to 21 percent in 2012 in the United Kingdom.

And though some would say tablets are not a substitute for a PC, about 75 percent of tablet media users want to “find the same things on their tablet as on their PC,” the study also found. That doesn’t mean people believe they can “work” on a tablet in the same way as on a PC.

But where it comes to content and information, they do expect they will be able to consume all the same content they would expect to get on a PC.

One of Google’s studies of tablet use over a two-week period, which had users recording every occasion that they used their tablet, shows that tablets really are not PCs, any more than smart phones are used in the same way that PCs are used.

Most consumers use their tablets for fun, entertainment and relaxation while they use their desktop computer or laptop for work, Google User Experience Researchers Jenny Gove and John Webb say. About 91 percent of the time that people spend on their tablet devices is for personal rather than work related activities.

And, as it turns out, when a consumer gets a tablet, they quickly migrate many of their entertainment activities from laptops and smart phones to this new device.

The most frequent tablet activities are checking email, playing games and social networking. The study also found that people are doing more activities in shorter bursts on weekdays (social networking, email) while engaging in longer usage sessions on weekends (watching videos/TV/movies).

Tablets are multi-tasking devices with at least 42 percent of activities occurring while doing another task or engaging with another entertainment medium. Tablets aren’t PCs

As it turns out, lots of things people can do on PCs don’t “need” to be done on PCs. Content consumption, email and other communications actually represent most of what many business users really “have to do” on a PC.

Also, tablets are more accurately described as “untethered” devices than “mobile” devices, to the extent that tablets primarily are used at home. Unlike smart phones that go everywhere and laptops that travel between work and home, few consumers take their tablets with them when they leave the house.

That shipments of tablets are expected to grow from 72.7 million units in 2011 to 383.3 million units by 2017, according to NPD, would not surprise many observers.

Growth in emerging markets, expected to account for up to 46 percent of worldwide shipments by 2017, an increase from the 36 percent share in 2011, might be more surprising.

The tablet forecast also illustrates an important change in connected appliance trends. In the past, “PCs” have been one category of appliances, while MP-3 players, phones and digital organizers, game devices, cameras and e-reading devices have been distinctly different categories.

These days, many of those devices have overlapping functions. Taken as a whole, the changes suggest the crucial role “content consumption” now plays as a lead application for most devices. Though PCs, cameras and organizers still largely have “work or business” use cases, virtually all the other devices are oriented around content consumption.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

It's Really Hard to Stand Out in a Market

A study of the customer experience of mobile apps and websites of 17 major financial services companies shows little differentiation, Foresee Results says. That shouldn't really be too surprising. It is hard, in any market, to truly create exceptional, unusual, unique products and experiences.

Only credit unions, measured in aggregate, meet the threshold for excellence with a score 80 on the 100-point scale of the ForeSee Mobile Satisfaction Index. Of course, in fairness, it is arguably fairly hard to differentiate a banking app.

ForeSee’s research shows that apps provide a superior experience to mobile websites and may be the key to competitive differentiation and growth. However, all companies measured have a ways to go to provide a compelling mobile experience: traditional websites (as experienced on personal computers) still provide the best customer experience for financial services companies.

Thus far, there is little differentiation between competitors, since satisfaction with all measured companies’ mobile experiences range between 73 and 79. A full set of scores is below:

Only credit unions, measured in aggregate, meet the threshold for excellence with a score 80 on the 100-point scale of the ForeSee Mobile Satisfaction Index. Of course, in fairness, it is arguably fairly hard to differentiate a banking app.

ForeSee’s research shows that apps provide a superior experience to mobile websites and may be the key to competitive differentiation and growth. However, all companies measured have a ways to go to provide a compelling mobile experience: traditional websites (as experienced on personal computers) still provide the best customer experience for financial services companies.

Thus far, there is little differentiation between competitors, since satisfaction with all measured companies’ mobile experiences range between 73 and 79. A full set of scores is below:

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Cable's "Mobile" Strategy is Mostly "Untethered"

Time Warner Cable is a partner with Comcast, Cablevision, Cox Communications and Bright House Networks in a public hotspot network of about 50,000 locations, and now is adding WeFi service as well. Time Warner invested in WeFi early in 2012.

Though cable operators have not been able to really figure out how to create a big mobile communications business, the current effort aims to extend use of fixed connections inside and outside the Time Warner network footprint.

Untethered communications, inside or outside the network footprint, is part of the strategy. In fact, in many cases a mobile phone uses a Wi-Fi connection more than the mobile network.

Though cable operators have not been able to really figure out how to create a big mobile communications business, the current effort aims to extend use of fixed connections inside and outside the Time Warner network footprint.

Untethered communications, inside or outside the network footprint, is part of the strategy. In fact, in many cases a mobile phone uses a Wi-Fi connection more than the mobile network.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Big Data Should be About "People"

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...