Apple surprised some observers, it is safe to say, by not releasing a low-cost device aimed at China and other similar markets.

To be sure, Apple has been saying it would not do so, but many expected Apple would change its views, as it is changing its views about screen sizes for tablets (smaller) and smart phones (larger), when it earlier had insisted there was no need to change.

Right or wrong, that move suggests to some that Apple is committing a "colossal" error, choosing to maintain a "premium" niche instead of dominating the mass market.

The essence of the argument for trouble is that Apple is clinging to charging ultra-premium prices for products that are no longer ultra-premium, as well as maintaining prices that are so high Apple is priced out of the world's largest and fastest growing markets.

Some of you with long memories remember that Apple made the same decision in the 1980s, when it allowed Microsoft, with a vastly-different strategy based on ubiquity, relegated Apple to a small and niche role from which the firm never really emerged (in the PC market).

Some argue that Apple is in danger of making that same mistake again, by essentially adopting the same strategy again--a premium and small smart phone niche--rather than going for dominance globally.

Others think Apple still has a strategy that will work.

Saturday, September 14, 2013

Is Apple Making the Same Mistake, Again?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Auction Policies Should Work, Not Just "Sound Good"

There is a clear difference between policies that work, and policies that don't work, but make people feel as though "something was done."

A colloquial way of putting this is that it is important to be good, not simply to feel good, when "feeling good" does not actually fix a problem, or makes a problem worse.

Spectrum auction and other policies designed to increase competition and innovation sometimes can include clauses that apparently boost competition, but actually have no ultimate positive effect. In at least some cases, those policies to "increase competition" actually can delay the arrival of more effective competition. It's a paradox, but no less true for being so.

Auction policies sometimes contain preferential treatment clauses designed to increase competition. T-Mobile US and Sprint, for example, have argued that the larger Verizon Wireless and AT&T Wireless should not be allowed to bid on reallocated analog TV spectrum, or at least that the two smaller carriers should have some preferences in that auction, to “level the playing field” between the two smaller carriers and the two bigger carriers.

That is not an uncommon regulator approach. It often is believed that “set asides” for specific types of bidders (small businesses, disadvantaged classes of people) is good public policy.

It doesn't work, one study suggests. Restrictive or preferential bidding rules distorts prices and misallocates spectrum in ways that ultimately harm consumer welfare.

Larger carriers often have access to more capital and can build networks faster, for example. In other cases, they are able to operate any particular block of spectrum with greater efficiency, because of other spectrum holdings.

On the other hand, competition and consumer welfare tend to be boosted by reassignment of existing spectrum and the existence of a dynamic secondary market for spectrum.

For example, restrictive and preferential participation rules in place for the 1994 U.S. PCS spectrum auctions resulted in lost consumer welfare of as much as $70 billion, analysts argue.

Underfunded and unfunded business plans developed by new entrants acquiring set-aside licenses resulted in substantial amounts of spectrum sitting idle for many years.

The role of secondary markets also is instructive. Following the PCS auctions in the mid-1990s, all significant new entry into the US wireless market has been through spectrum re-purposing or the secondary market.

In the German 3G auctions in 2000, policies intended to encourage market entry were unsuccessful and resulted in a 10-year delay in the assignment of one-third of the 3G spectrum, delaying its development and the benefits consumers would have otherwise enjoyed.

In Canada and several European countries, restrictive and preferential policies intended to encourage market entry distorted the auction process and were unsuccessful in expanding the number of sustainable competitors in the marketplace.

Initial changes in the competitive landscape, attributable to restrictive auction rules, proved fleeting as market forces pushed the industry structure back to a pre-auction market structure with the same number of, or fewer, national competitors.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

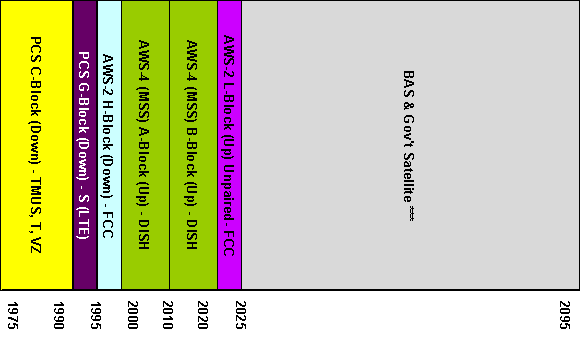

U.S. to Auction 10 MHz of Mobile Spectrum Now, 55 MHz More in Feb. 2014

The Federal Communications auction of 10 MHz of spectrum in the 1900 MHz band (1915-1920 MHz and 1995-2000). The move has been a bit controversial, as spectrum auctions frequently can be.

Dish and T-Mobile US had urged the FCC to delay the H Block auction, which is adjacent to spectrum Sprint already has in service.

The logic for a delay is that another planned auction of spectrum (AWS-3 M-Block) in February 2015 could be paired with the auction of the H Block spectrum (about 55 MHz worth of spectrum).

But the FCC has decided to move ahead, despite arguments that a delay might be preferable, and potentially more valuable, for T-Mobile US, Dish Network or other competing carriers.

As an old aphorism suggests, “for every public purposes there is a corresponding private interest.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, September 13, 2013

T-Mobile's LTE network now covers 180 million people in 154 markets

The T-Mobile US LTE network now covers 180 million people in 154 markets, which is perhaps notably impressive because T-Mobile US only began construction six months ago.

The carrier first launched its LTE in just seven markets back in March 2013. As network construction projects go, that's fast.

On the other hand, it arguably is deceptive to show coverage maps such as this, which is "not (my emphasis) representative of LTE coverage," according to T-Mobile US itself. True the disclaimer is at the bottom of the map, so the image is not legally deceptive. It just is an effort to persuade that unfortunately is untruthful.

On the other hand, it arguably is deceptive to show coverage maps such as this, which is "not (my emphasis) representative of LTE coverage," according to T-Mobile US itself. True the disclaimer is at the bottom of the map, so the image is not legally deceptive. It just is an effort to persuade that unfortunately is untruthful.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Verizon Wants to Sell FiOS TV Nationwide

Verizon is having conversations with major programmers about how to bring its FiOS programming service to a national audience, delivered "over the top" of any broadband connection.

Aside from the obvious implications for the future of online video entertainment, such a move would further decouple service providers from some traditional geographical limitations. In the past, mobile or fixed service providers could operate only in geographies where they owned spectrum, networks or franchises or licenses.

The advent of the era of Internet Protocol and Internet-based communications breaks the link between network infrastructure and applications. So far, that mostly has manifested itself in over the top app growth.

But, in principle, streaming video can be sold over the top as well, as Netflix has so amply demonstrated.

Such a move "out of territory" would allow Verizon to sell video entertainment to potential customers across the United States, and not only to the five million or so video accounts

Verizon presently services on its landline network.

Going over the top and out of territory would allow Verizon to sell to perhaps 130 million households.

Aside from the obvious implications for the future of online video entertainment, such a move would further decouple service providers from some traditional geographical limitations. In the past, mobile or fixed service providers could operate only in geographies where they owned spectrum, networks or franchises or licenses.

The advent of the era of Internet Protocol and Internet-based communications breaks the link between network infrastructure and applications. So far, that mostly has manifested itself in over the top app growth.

But, in principle, streaming video can be sold over the top as well, as Netflix has so amply demonstrated.

Such a move "out of territory" would allow Verizon to sell video entertainment to potential customers across the United States, and not only to the five million or so video accounts

Verizon presently services on its landline network.

Going over the top and out of territory would allow Verizon to sell to perhaps 130 million households.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Kabel Deutschland Shareholders Vote to Sell to Vodafone

Kabel Deutschland shareholders have voted in favour of selling the company to Vodafone.

The €7.7 billion deal is part of Vodafone's strategy to counter declining mobile revenues by selling quadruple play services.

Vodafone is the largest mobile network in Germany with 32 million subscribers. Kabel Deutschland has 7.6 million cable subscribers.

Vodafone said that the required minimum of 75 percent of Kabel shareholders had voted to accept its €87 per share offer, which includes a €2.50 dividend payment.

The deal still has to be approved by regulators.

The acquisition illustrates the maturation of the mobile business as a driver of industry growth in Europe, and one of the strategies leading service providers will employ to maintain revenue growth. When organic growth is not possible, service providers turn to acquisitions.

The €7.7 billion deal is part of Vodafone's strategy to counter declining mobile revenues by selling quadruple play services.

Vodafone is the largest mobile network in Germany with 32 million subscribers. Kabel Deutschland has 7.6 million cable subscribers.

Vodafone said that the required minimum of 75 percent of Kabel shareholders had voted to accept its €87 per share offer, which includes a €2.50 dividend payment.

The deal still has to be approved by regulators.

The acquisition illustrates the maturation of the mobile business as a driver of industry growth in Europe, and one of the strategies leading service providers will employ to maintain revenue growth. When organic growth is not possible, service providers turn to acquisitions.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

How Big a Deal is the Right to Sell iPhones?

How big a deal is access to the Apple iPhone? According to one study, about 66 percent of NTT Docomo customers who signed up with another service provider did so at least in part because they wanted to use the iPhone.

That probably is a mixed blessing for mobile service providers. The potential good news is that the iPhone, and smart phones in general, might be the most tangible physical expression of the value of Internet access and mobile service more broadly.

The problem all sellers of intangible products (health care, legal advice, tax and financial consulting or communications service) encounter is that it is hard to show the value of something that is a process.

The buyer has no idea how good the experience will be until after the purchase is made. In such cases, a seller has to rely on proxies for value. Those proxies might include displayed certifications and licenses, degrees, awards, furniture, office addresses or professional attire.

Communications service providers have the same problem: there is no tangible product to evaluate in advance. How many people have you ever met who have a brand preference for one supplier’s “dial tone” over another supplier’s dial tone?

One might well argue, with some justification, that Internet access allows for much more differentiation. Speed or usage policies, as well as the specific configuration of retail offers, allow for more distinctive positioning than was possible with dial tone.

Those proxies are ways an intangible product is made “tangible.”

How does one cultivate brand preference for an intangible product? One way is to emphasize the more-tangible “wrap-around,” such as customer service experience, brand and image.

But that’s inherently hard, compared to the brand preferences people develop for personal products ranging from cars to perfumes and clothing brands and styles. One might argue the iPhone is the first tangible expression of personal affinity for a product whose value hinges on a communications service.

That helps service providers when they can sell the device. People are more likely to be “loyal to an iPhone” than to a service provider. Service providers do the best when the right to sell an iPhone is exclusive, but arguably are helped very little when every major service provider in a market has rights to sell the device.

The larger problem, though, is that “value” and “loyalty” as well as brand preference largely are transferred to the device supplier.

In many ways, that illustrates the “commodity supplier of access” problem all service providers face. Though it is not impossible, it is difficult to create a consumer mental image of “access” that is differentiated and preferred.

Google Fiber might be the first access service in quite some time that has a chance to transcend the “commodity access” problem, in part because its offer is so unique. A symmetrical one gigabit service, sold for $70 a month, is unusual. And it is Google acting as an ISP. That’s unusual as well.

Most service providers offering an access service are not so lucky.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...