Starting Oct. 16, 2013, Google Fiber TV customers can stream the WatchESPN and WATCH Disney apps to their smart phones and tablets for free. The deal isn't unusual or exclusive, as WatchESPN and WATCH Disney are available from most Internet service providers.

But the deal adds one more important ISP, and makes streaming direct to end users by a content provider more common. Eventually, the accumlated weight of such direct-to-consumer content offers is going to help create the foundation for widespread delivery of programming network content as well.

It will take a while, and Disney is more comfortable with such concepts than most other programming networks. But, little by little, the barriers to direct distribution over the Internet are being chipped away.

WatchESPN provides live access to eight networks, including live events and all of ESPN’s sports and studio shows (including ESPN, ESPN2, ESPNU, ESPN3, ESPN Deportes, ESPNEWS, ESPN Goal Line and ESPN Buzzer Beater).

WATCH Disney gives users live access to Disney Channel, Disney Junior and Disney XD networks. Just go to WatchDisneyChannels.com and log in using your Google Fiber username and password.

Wednesday, October 16, 2013

Google Fiber Adds ESPN, Disney Streaming for Smart Phones, Tablets

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

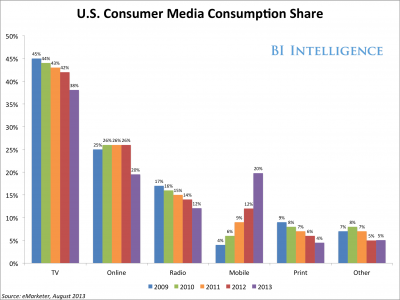

Mobile Is Reaching Parity with Online Content Consumption, Soon Will Trail Only Television

Mobile devices (smart phones and tablets) now account for about 20 percent of all U.S. consumer content consumption, exceeding the volume of print and radio consumption and rivaling online consumption.

Mobile devices (smart phones and tablets) now account for about 20 percent of all U.S. consumer content consumption, exceeding the volume of print and radio consumption and rivaling online consumption.

That is a big deal. Soon, mobile consumption will exceed online content consumption.

What it means is that the next target for mobile content consumption is television volumes.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Data Volume Mostly Carried on Fixed Networks

Mobile broadband might never be a completely satisfactory substitute for fixed broadband access. Many would argue it does not have to be a complete substitute, only a reasonable substitute in some cases.

Nor, given current trends related to smart phone use of Wi-Fi access, is it necessarily the case that most users ever will want to use mobile Internet access as a primary alternative to fixed access.

One might be tempted to argue the opposite position, that in fact fixed Internet access routinely handles as much as 80 percent of all smart phone data operations, in which case one might argue that mobile Internet access is, and always will be, supplemental to fixed network access.

That said, it appears likely that though the volume of data consumed will remain a fixed network function, mobile could represent the vast majority of instances of use. In other words, most of the data will flow over the fixed access network, but most of the sessions could be mobile.

Smart phone data consumption on Wi-Fi networks ranges from twice to 10 times the volume of data consumed by smart phones on the mobile network, one study has found.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

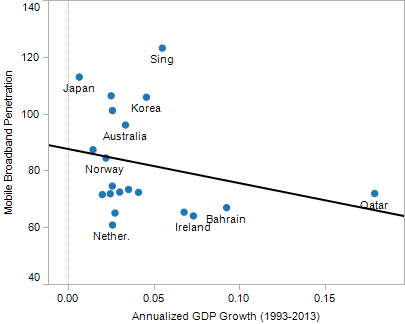

Does Mobile Broadband "Cause" Economic Growth?

Though correlation is not causation, it might also be said that, in terms of the relationship between mobile broadband adoption and gross domestic product, the correlation might be positive, neutral or negative.

That is not what people tend to believe, or want to believe. But neither does evidence necessarily support the notion that mobile broadband causes, or leads to, economic growth.

Consider that a United Nation’s Broadband Commission report includes the standard view that broadband deployment leads to economic growth.

That is not to argue against robust adoption of mobile broadband. The point is that it is not clear broadband adoption, in and of itself, actually leads in a direct way to economic growth.

That is not what one typically hears. Ericsson sponsored a study conducted by Arthur d. Little and Chalmers University of Technology to quantify the economic impact of broadband speed upgrades, at both the country and household levels.

The main conclusion was that doubling the broadband speed for an economy can increase gross domestic product growth by 0.3 percent on average in Organization for Economic Cooperation and Development economies.

The average increase in household income for a broadband speed upgrade of 4 Mbps to 8 Mbps is US$120 per month in OECD countries.

Households in Brazil, Russia, India and China benefit most by upgrading from 0.5 Mbps to 4 Mbps, at US$46 per month.

For households in OECD countries, there is a threshold broadband access speed to increase in earnings, somewhere between 0.5 Mbps and 2 Mbps on average. The greatest expected increase in income is for the transition from being without broadband to gaining 4 mbps, the

difference being around US$2,100 per household per year (equivalent to US$182 per month).

In BRIC households, the threshold level seems to be 0.5 Mbps. Rround US$800 additional annual household income is expected to be gained by introducing 0.5 Mbps broadband

connection in BRI country households, equivalent to US$70 per month per household.

But other data suggests that, for the 20 countries with the highest mobile broadband penetration, there is actually a negative relationship between GDP growth and broadband penetration.

Some might facetiously argue that limiting mobile broadband use might promote economic growth. Nor is it completely clear that economic growth and fixed network broadband are causally related. People tend to assume that is the case, but it is tough to prove.

The point is that although the conventional wisdom is that broadband availability--fixed or mobile--”must” lead to economic growth, statistics do not uniformly support that conclusion.

There is no one obvious factor predicting mobile broadband penetration in these major countries, or the relationship to economic growth, one might well argue.

"There are just too many other factors that affect GDP growth for mobile broadband to have any significant and measurable effect,” said Yankee Group Research VP Declan Lonergan.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

U.S. Mobile Business Becoming a Price Game?

Is the U.S. mobile market heading further in the direction of becoming a price game, despite all efforts by service providers to avoid that scenario? Ask French mobile service providers, who have seen revenues and profit margin plummet after the market entry of Illiad’s Free Mobile.

That is not to discount the value of human agency. Talented and creative executives might be able to create value that run counter to the other trends. But that will occur against a backdrop of heightened retail pricing pressure.

In the U.S. market, contestants including Republic Wireless and FreedomPop are trying to disrupt mobile pricing. But many observers expect the real changes to come from the likes of T-Mobile US or Sprint, both anxious to gain market share, and both newly fortified by their German and Japanese financial backers.

The result is that the relatively stable U.S. mobile market, stable for a decade, is going to face attempts at disruption, and price is expected to be a huge part of the effort.

Unless the U.S. Department of Justice has an unexpected change of analytical framework, there is no chance a merger between T-Mobile US and Sprint would be allowed, a move that would fuel even more competition. That leaves organic growth as the only way to make a material difference in U.S. mobile market share.

Denied further opportunity to merge, and facing quite modest remaining acquisition opportunities, the four leading national carriers have no choice but to attempt organic growth in a saturated market.

Also, the two smaller national carriers have just made billions worth of new investment in their networks and businesses, and will be seeking a financial return by growing their market share.

If you knew nothing but the history of competition in saturated markets, you know what will happen. Price competition will reach new levels. Executives can deny any interest in doing so all they want. Rarely does new competition make serious inroads into any market without upsetting established pricing.

Also, there is the further issue of what happens to prices in a mature market. Some believe the U.S. mobile phone market is nearing saturation. What markets can you think of where saturated demand and abundant supply has failed to put pressure on prices?

Typically, a mature market is characterized by excess capacity, increased difficulty of maintaining product differentiation, increased intensity of competition, and growing pressures on costs and profits.

That is not to discount the value of human agency. Talented and creative executives might be able to create value that run counter to the other trends. But that will occur against a backdrop of heightened retail pricing pressure.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, October 15, 2013

How Much Video Piracy is Caused by Lack of Legal Streaming and Rental?

Movie and video content owners have a notably complex way of allowing people to view new content. And some might argue content owners would suffer less content piracy if those content owners were a bit more flexible about the ways people could view content.

A look at piracy rates for specific titles for a recent three week period shows that none of the most pirated titles were available for legal streaming and only 53 per cent were available to buy at all. About 20 percent of those titles were available to rent, according to researchers at the Mercatus Center.

A look at piracy rates for specific titles for a recent three week period shows that none of the most pirated titles were available for legal streaming and only 53 per cent were available to buy at all. About 20 percent of those titles were available to rent, according to researchers at the Mercatus Center.

So content owners might be able to slash piracy rates by simply making content easily and legally available, rather than trying legal and technological hacks to sustain its current release model, in other words.

The analysis of file-sharing news was based on TorrentFreak's weekly top-10 most-pirated media, cross-referenced with statistics on legitimate media buying and streaming, shown at Piracy Data.

Would legal alternatives halt all piracy? Probably not all piracy, one might guess, but nearly all of it.

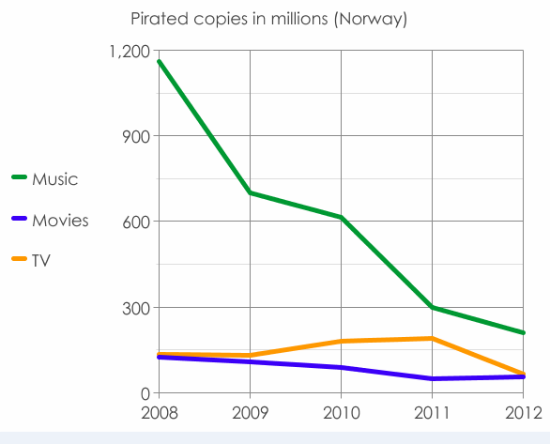

In Norway, where tough anti-piracy measures were put into place in June 2013, music piracy rates have been dropping dramatically, while TV and movie pirarcy also has dropped since 2008.

Many would say that is because legal alternatives are more compelling.

A look at piracy rates for specific titles for a recent three week period shows that none of the most pirated titles were available for legal streaming and only 53 per cent were available to buy at all. About 20 percent of those titles were available to rent, according to researchers at the Mercatus Center.

A look at piracy rates for specific titles for a recent three week period shows that none of the most pirated titles were available for legal streaming and only 53 per cent were available to buy at all. About 20 percent of those titles were available to rent, according to researchers at the Mercatus Center. So content owners might be able to slash piracy rates by simply making content easily and legally available, rather than trying legal and technological hacks to sustain its current release model, in other words.

The analysis of file-sharing news was based on TorrentFreak's weekly top-10 most-pirated media, cross-referenced with statistics on legitimate media buying and streaming, shown at Piracy Data.

Would legal alternatives halt all piracy? Probably not all piracy, one might guess, but nearly all of it.

In Norway, where tough anti-piracy measures were put into place in June 2013, music piracy rates have been dropping dramatically, while TV and movie pirarcy also has dropped since 2008.

Many would say that is because legal alternatives are more compelling.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Amazon Working on Smart Phone with HTC

Though Amazon continues to deny it is developing one or more smart phones, another report suggests Amazon is working with HTC to develop a range of smart phones. But some think the recent Amazon denial of any device "in 2013," could well be developing one or more devices for 2014 introduction.

Though Amazon continues to deny it is developing one or more smart phones, another report suggests Amazon is working with HTC to develop a range of smart phones. But some think the recent Amazon denial of any device "in 2013," could well be developing one or more devices for 2014 introduction. Some will question the wisdom or need for such devices, but to the extent Amazon wants to retain relevance and sales in the content business, a branded device, optimized for Amazon's own content store, would be similar in intent to Amazon's Kindle line of devices.

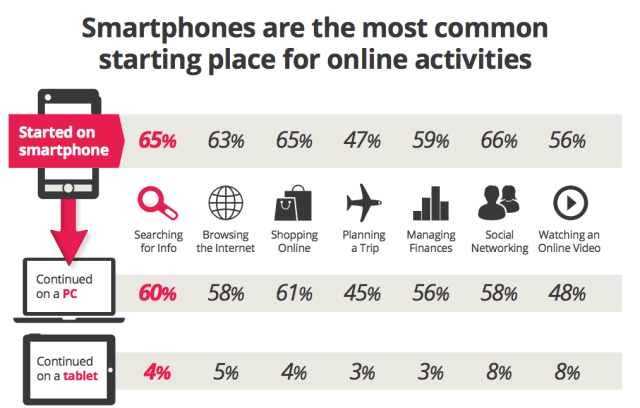

The point is that what people do on tablets, they do on smart phones. And many online activities start on smart phones, and are finished on other devices such as tablets and PCs.

Amazon might not want to miss that part of the transaction value chain.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...