Will the French mobile market or the U.K. market provide a precursor of developments in the U.S. mobile business?

The U.S. and French mobile markets are unstable, both presently have four leading national contestants, while a major transaction with change of control has occurred in France, while a possible bid to do the same in the U.S. market could be launched within months to two years.

The U.K. market, on the other hand, features more than four national providers, with BT a new entrant. In addition to three firms with more than 15 percent share, there are three additional providers with at least seven percent market share.

Some might argue France resembles the current U.S. mobile market structure, though the U.K. could be more germane if both Dish Network and a cable TV operator operation launch as independent entities, and the legacy mobile carriers do not consolidate.

That could mean as many as six national providers in the market, though most think five or four is a more-likely outcome, even after the entry of Dish Network and a cable operator operation as well.

Illiad’s Free Mobile has disrupted the French mobile market by attacking prices, basing that assault on use of a “Wi-Fi-first” access model that U.S. cable operators also plan to use to anchor a future untethered or mobile access business.

The chief difference at the moment is that the French government now has concluded that ruinous levels of competition exist, and that stable competition, long term, will be served if the mobile market consolidates to three dominant national providers.

In the U.S. market, at least so far, regulators and antitrust authorities have signaled a belief that maintaining four national competitors is necessary. In the French market, government officials now believe competition has reached ruinous levels.

To end a destructive price war, Economy Minister Arnaud Montebourg has argued that the number of mobile operators needed to be reduced. That consolidation further would allow the surviving operators to invest more aggressively in next generation networks.

Matters are more fluid in the U.S. market, though. No matter what view U.S. regulators hold, two additional contestants will enter the market: Dish Network, which must build a network and begin offering service or lose its mobile spectrum licenses, and the asset value the spectrum represents.

Also, the cable industry will enter the market, using a strategy pioneered by Free Mobile.

So while the French government now pushes for consolidation in the country's mobile market--from four providers to three--the U.S. market could potentially see as many as five to six national providers in the near future.

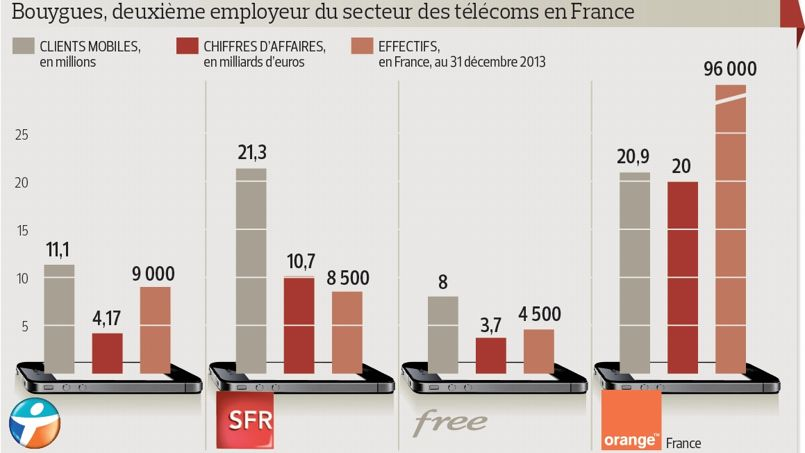

Note that in France, it was Numericable--France’s largest cable TV operator--that has acquired SFR, creating France’s second-biggest communications provider, behind Orange.

"There are two smaller operators that remain, and we can wonder what their future will be unless they merge, which doesn't seem to be on the agenda right now," Montebourg has said.

Consolidation "will happen," Montebourg says. "We will make three operators capable of investing, which will stop destroying jobs and killing each other.”

Many observers would argue that the logical combination would be a combination of Illiad’s Free Mobile and Bouygues. Illiad owns fixed network assets as well as mobile assets.

At the same time, Free Mobile, which is building its mobile network, then would have access to the Bouygues access network, while Bouygues mobile customers would have access to Illiad’s fixed network for mobile data offload.

Since April 2014, the French government has said it will actively encourage mobile market consolidation, a bit of a switch from some earlier thinking that four service providers in the market was preferable to just three in the market.

But there is a difference between the French and U.S. markets. France had just three dominant providers prior to Free Mobile’s market entry in 2012. So a return to three providers would merely restore former market structure.

In the U.S. market, the recent pattern has featured four national providers, even if two more entrants are expected.

Systemic risk to Orange, however, clearly is an issue for some French government authorities, who believe the danger to jobs is greater than the risk of reduced consumer benefits from competition.

So in one sense, the French market seems headed for fewer providers, while the U.S. market seems headed for more providers, even if Sprint were allowed to merge with T-Mobile US, or if some subsequent deal allowed Dish Network to buy T-Mobile US.

After the expected entry of a cable operation, there still would be at least four national providers, and potentially five. tru