A survey of U.S. consumers has found what you might expect, namely that few U.S. residents understand network neutrality. The Hart Research Associates survey found only 25 percent of respondents claimed they knew what network neutrality is.

Perhaps not surprisingly, 73 percent said they wanted disclosure of what the rules actually are, when told that “just five members of an unelected Federal Communications Commission will decide the future of the Internet without providing an opportunity for the public to see and understand the regulations prior to a vote.”

The wording of the explanatory note, most might suggest, was not “neutral.” So it might not be surprising that 80 percent of respondents wanted full disclosure of the ruling before a vote is taken.

Just 32 percent of respondents thought regulating Internet access like telephone services would be helpful.

With the caveat that a business customer’s use of bandwidth differs from the pattern typical of a consumer customer, small business customers of Cogent Communications tend to use about 12 Mbps of the 100 Mbps services bought to replace T1 connections of about 3 Mbps, said BTIG researchers.

According to Cogent, only about 12 to 24, out of perhaps 17,400 customers ever have reached 50 percent utilization of the 100 MB pipe. Likewise, customers who buy gigabit connections have usage that does not likely differ materially from 100 MB customers, according to Cogent.

One might well argue that consumer consumption is growing faster than business customer usage, certainly. But Sandvine data suggests U.S. median household data consumption over a fixed network connection is about 20 Gb a month. Granted “Gbps” is a measure of speed, while “Gb” is a measure of consumption, but monthly consumption of 20 Gb does not suggest most households likely are taxing their access downlinks.

To be sure, households with faster connections tend to consume more data. But that might be because households consuming more data disproportionately buy the faster connections. As more locations are able to use connections operating from 40 Mbps up to 1 Gbps, we should get a better idea of how much a “typical” user consumes, when access speeds exceed the ability of far-end servers to respond.

A study by Ofcom, the U.K. communications regulator, suggests that beyond about 10 Mbps, local access speed is not the experience bottleneck.

The study found that “access speed” matters substantially at downstream speeds of 5 Mbps and lower. In other words, “speed matters” for user experience when overall access speed is low.

For downstream speeds of 5 Mbps to 10 Mbps, the downstream speed matters somewhat.

But at 10 Mbps or faster speeds, the actual downstream speed has negligible to no impact on

end user experience.

Since the average downstream speed in the United Kingdom now is about 23 Mbps, higher speeds--whatever the perceived marketing advantages--have scant impact on end user application experience. Some 85 percent of U.K. fixed network Internet access customers have service at 10 Mbps or faster.

Investing too much in high speed access is, as a business issue, as bad as investing too little, one might argue.

Average access speeds in the United States are 10 Mbps, according to Akamai. Average speeds are 32 Mbps, according to Ookla. Another study shows that average Internet access speeds in the United Kingdom and United States are equivalent, in fact.

The point is that, in terms of user experience, faster marketed speeds (gigabit, 100 Mbps) actually do not improve end user experience.

As someone who recently was able to upgrade from about 15 Mbps to 105 Mbps, I would confirm, as an end user, that the upgrade has made no apparent difference in my browsing experience.

For that reason, I will not be buying a gigabit access connection, which I could do. There being no apparent change in experience at 100 Mbps, I cannot see the advantage of upgrading further, to 1 Gbps.

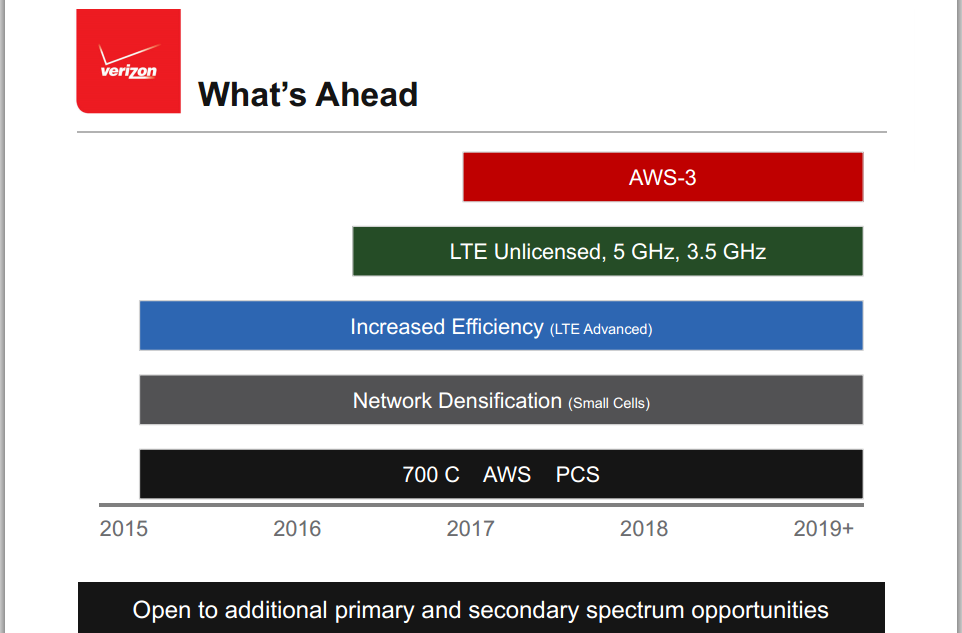

As important as licensed spectrum has been for development of mobile services, unlicensed spectrum is shaping up as a more-important access approach.

Verizon Communications has committed to introduce Long Term Evolution using unlicensed spectrum, even before the formal standard has been ratified.

LTE in unlicensed spectrum allows mobile service providers to bond capacity supplied by licensed and unlicensed spectrum.

The other important development is the Internet of Things, especially many machine-to-machine sensor apps that require extremely low-cost devices with long battery life, wide area communications range and low-cost network platforms as well.

So it is that the LoRa Alliance, including firms such as IBM, Cisco and Microchip Technology, as well as telecom operators Bouygues Telecom, KPN, SingTel, Proximus, Swisscom, and FastNet (Telkom South Africa), supports the use of LoRa spread-spectrum radio protocol for use in wide area networks and the Internet of Things.

LoRa (Long Range) is a low data rate, long-distance communication protocol used by Semtech Corp. to provide industrial, home and building automation networks. LoRa supports devices with a range of up to 50 kilometers. The long range means that large areas can be covered by relatively few base stations.

Just as significantly, LoRa devices are expected to operate for as long as 10 years without a battery swap.

That is part of the reason supporters believe LoRa has value for many IoT and M2M applications.

Separately, SigFox uses an ultra-narrow-band platform for machine-to-machine communications and IoT, also operating in unlicensed spectrum.

The base stations are said to operate over ranges of three to 10 kilometers in urban areas and up to 30 to 50 kilometers in rural areas.

To be sure, mobile service providers have numerous tools available to them to increase network capacity, ranging from exclusive spectrum resources to traffic offload to network architecture to improvements in air interface technology.

So despite the importance of licensed spectrum, other sources of leverage, including unlicensed spectrum and network elements, technology and architectures, are becoming equally important.

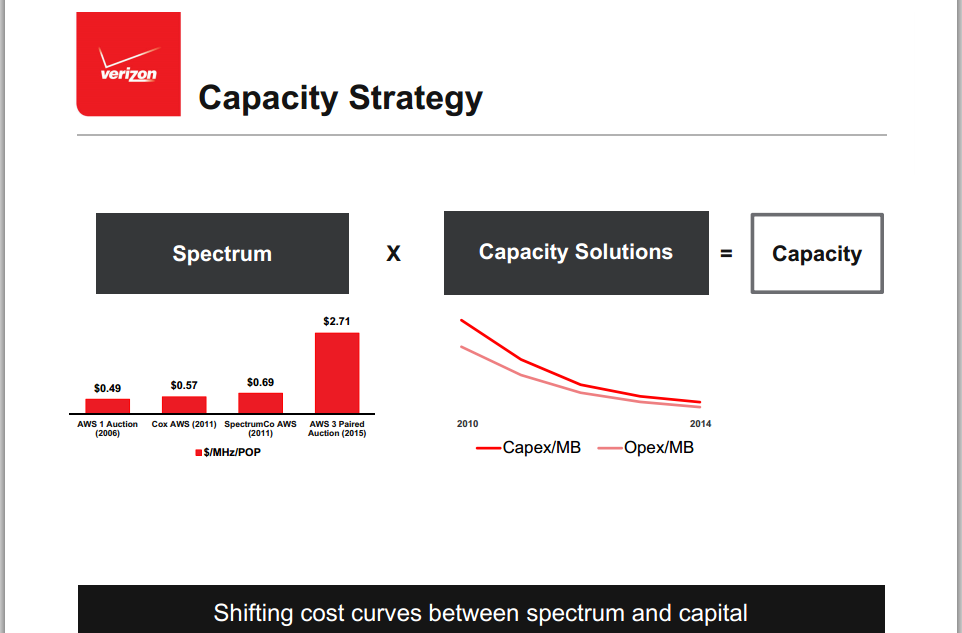

And at least as Verizon Communications positions the matter, the cost of acquiring new spectrum is growing, while the cost of network enhancements is dropping.

Without question, mobile service providers prefer to supply capacity by gaining the use of new spectrum, largely because that has been “an extremely cost effective means of adding capacity,” according to Tony Melone, Verizon Communications CTO.

But Moore’s Law and manufacturing volume matter. So the cost of relying on a technology-driven solution (smaller cells, better radios, antennas and modulation protocols) are going down every year, Melone also said.

That probably does not mean capacity gains are equivalent, using either “new spectrum” or “network technology” approaches. It likely remains the case that additional spectrum remains a cheaper way to gain new capacity.

But Long Term Evolution, eventually 5G, antenna technologies and interference management techniques are playing a crucial role.

“All of these technology solutions will drive improvements in bits per hertz and cost per bit,” Melone said.

The latest technique is use of LTE protocols over unlicensed spectrum. “With our key suppliers we are active in the standards process and will likely deploy a pre-standard version in the not too distant future,” said Melone.

Unlicensed spectrum might play a key role supporting Internet of Things networks especially focused on industrial, agricultural, utility and environmental sensor applications.

Such applications typically require low power platforms of low cost, but able to transmit messages at reasonable distances.

SigFox claims to have a network providing 80 percent coverage of France and has signed up operators in the Netherlands, Spain, UK and Russia, and is working on satellite connections as well.

The point is that, if one assumes the next big leap in mobile and untethered communications will be to support machines, not people, then unlicensed spectrum is likely to play a bigger role.

T-Mobile US might, by the end of 2014, caught Sprint in terms of total number of subscribers. Possibly early in 2015 T-Mobile US could pass Sprint, with T-Mobile US becoming the third largest mobile service provider. Market share shifts of that type, at the top of the market, do not happen very often.

It isn’t yet clear what Apple might be up to in terms of connected car activities. Some think Apple will build an automobile, while others think Apple only wants to unify as much of the in-vehicle communications and applications experience as possible.

Whatever the reason, Apple has us all talking about the possibilities, which might be a signal sent about future huge product categories beyond the watch. Whatever the long term thinking, that possibility will help Apple attract and retain key employees attracted by the opportunity.

Despite the apparent fact that consumers do not really seem to understand what a connected car is, analysts are forecasting huge sales for connected car products and systems.

Transparency Market Research predicts the connected car market will reach $132 billion by 2019.

Even if one believes streaming services are about to begin taking more market share in the subscription TV and video business from linear providers, that does not mean every provider is losing customers, market share, or revenue.

In its most recent quarter, DirecTV grew Latin America full year revenues three percent, to $7.1 billion, largely by adding 903,000 net new subscribers.

Full year U.S. revenue grew five percent to $26 billion, driven by average revenue per user growth of 4.7 percent and annual subscriber growth of 99,000 accounts.

Full year 2014 earnings per share Increased 12 percent, while free cash flow grew 21 percent to $3.1 billion.

What AT&T, in the process of acquiring DirecTV, cares about is the free cash flow, even more than the incremental revenue and the ability to sell entertainment video, plus its other mobile services, nationwide.

As a long term matter, it has seemed logical that tier one telcos globally would begin to shift revenue focus from the consumer to the business segment, especially where competition in the fixed network segment was particularly robust.

That trend seems to be emerging clearly for AT&T.

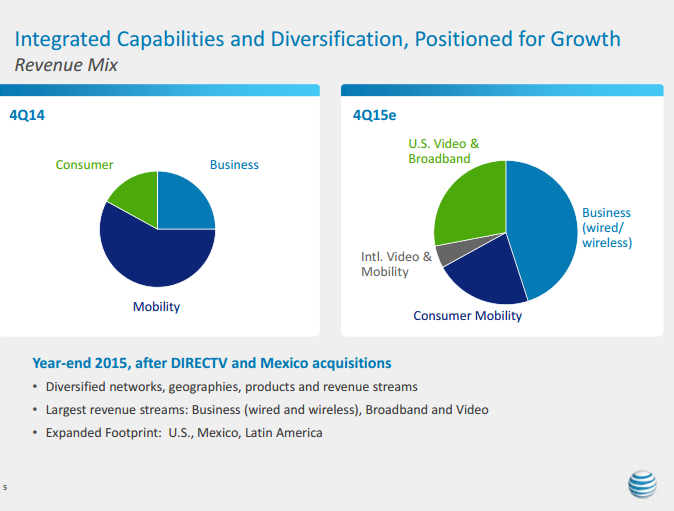

Our transactions with DIRECTV and Mexican wireless companies Iusacell and Nextel Mexico will make us a very different company, said AT&T CEO, Randall Stephenson. “After we close DIRECTV, our largest revenue stream will come from business-related accounts , followed by U.S. TV and broadband, U.S. consumer mobility and then international mobility and TV.”

Consider the magnitude of the changes. In 2014, AT&T reported earning nearly 60 percent of total revenue from mobile services. AT&T meanwhile earned about a quarter of its revenue from business customers.

Consumer landline revenue was less than 20 percent of total.

Assuming AT&T’s acquisitions of Iusacell, Nextel Mexico and DirecTV are approved, AT&T will earn about 45 percent of total revenue from business customers and about 20 percent from consumer mobility services.

About 30 percent of revenue would be earned from U.S. consumer high speed access and video entertainment.

For perhaps the first time, AT&T revenue would be driven by business accounts, not consumer services.

For the first time, AT&T would emerge as a leader in the subscription video market.

Contributions from the mobility segment would not wane, but AT&T would be far less exposed to competition in the consumer mobile segment.

All of that has key implications. AT&T will reduce reliance on U.S. market revenues and consumer “communications” revenues, to a significant extent, with a bigger reliance on video entertainment.

One might argue that diversification lessens the threat AT&T faces from cable TV, T-Mobile US and Sprint, CLECs, Google Fiber and other emerging independent ISPs.

One obvious question is what Verizon might do. So far, it has made a different bet, banking heavily on the U.S. mobile market for growth. Whether that will remain the case over the next decade is the issue. Some might argue the fundamental strategy will have to change.

The extent to which the pattern emerges elsewhere around the globe is the larger issue. Some might argue the pressure to focus on business accounts is less, since “cable TV” tends not to be a rival industry but a platform owned by tier one telcos, where it is a factor in the markets.

Also, few markets have the degree of facilities-based competition on the U.S. model.

Still, there are any number of reasons why tier one service providers ultimately might want to shift attention to business accounts. Larger revenue per account is one good reason.

Also, higher profit margins are another advantage. That is one reason why U.S. competitive local exchange carriers generally focus on business accounts only when they move out of market and compete with other telcos.

Also, to some extent, there is less competition in the business segment, compared to the consumer segment. Few competitors can compete with tier one telcos, other than other tier one telcos, in the international communications segment, or even in national large enterprise account markets.

There arguably is more competition in the mid-market segment, but growing competition in the small business (mass markets) end of the market, especially as both cable TV companies and CLECs compete in the small business market.

In consumer markets, there is fierce competition from satellite and cable TV providers. In fact, in the U.S. market, it increasingly looks as though cable TV companies are emerging as the leading providers of fixed network triple play services, not telcos.

Even in the mobile services segment, long dominated by telcos, heightened competition is occurring, putting pressure on gross revenue and profit margins. And more competition is expected,