Dynamic embedded subscriber information modules--something Apple introduced in 2014 for its iPad devices--are among the possible enhancers of competition in mobile markets.

The Apple SIM made it possible for iPad owners in the United States and United Kingdom to pick and choose a mobile connectivity provider, directly from the device (assuming multiple providers were willing to support the feature).

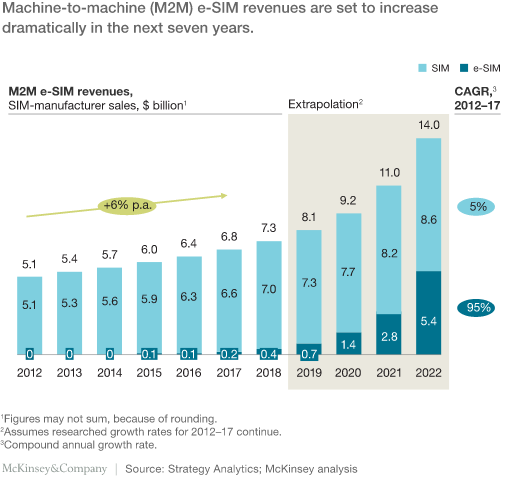

As Internet of Things devices and applications proliferate, the same basic concept--allowing an programmable electronic SIM to select from a number of potential mobile connections--could emerge on a wider scale, argue McKinsey and Company consultants Markus Meukel, Markus Schwarz, and Matthias Winter.

As you might imagine, mobile service providers were not keen on enabling that level of competition. But there is new thinking about IoT requirements, especially the ability to remotely activate IoT devices. And that requires use of an e-SIM.

So the difference in industry reception between the Apple SIM and e-SIMs is the role in supporting a big new revenue stream and business model. Where Apple SIM was a threat to existing business models, e-SIMs are a support for new and different business models.

The GSMA expects to finalize a technical architecture 2016.

In principle, widespread e-SIM capabilities could have marketing implications for wearables. Targeting new clients through promotional activities may be as easy as having them sign up by scanning the barcode of a print advertisement and activating the service immediately.

On the other hand, the ease of use and ease of operator switching has the potential to weaken the network operator’s position in the mobile value chain.

Customer touchpoints also could change. The e-SIM eliminates the need for customers to go to a store and acquire a SIM card when signing up for service. That might negatively affect the amount of upselling.

Churn and loyalty also could be affected, since customer may be able to switch operators and offers more easily. Churn could increase.

Prepaid versus contract markets. E-SIM’s impact may be greater in markets with more prepaid customers, as well.

There could be changes at the wholesale level. As Google’s Fi essentially has pioneered, wholesale service providers might buy capacity dynamically from multiple capacity and access providers. That could happen on price or quality or both dimensions.

High prices for global roaming might be just as important, allowing travelers to locally provision service when traveling internationally.

You can make your own estimates of possible advantages and disadvantages, for core mobile services sold to people and IoT devices.